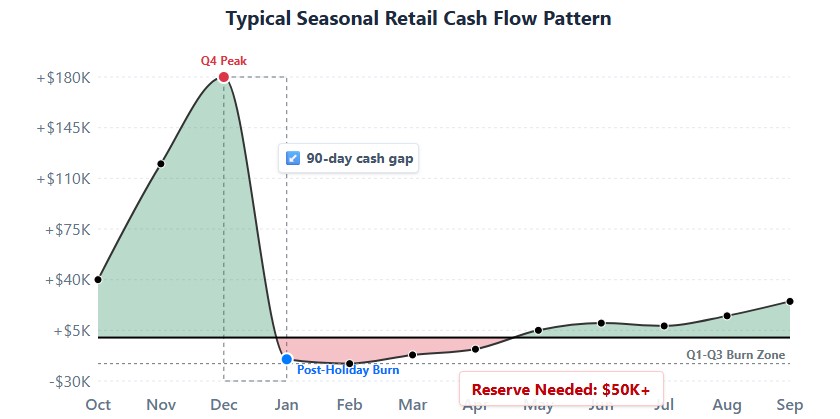

Most seasonal retailers treat the holiday season like a gold rush and the first quarter like a vacation. That mindset is exactly why 41% of seasonal businesses face cash flow gaps exceeding 90 days post-holiday. When 40% of your annual revenue hits in November and December, a flawed break-even model doesn’t just hurt your Q4 profits—it bankrupts your Q1 operations.

The real challenge isn’t just hitting a revenue number in December. It’s calculating your break-even point while accounting for post-holiday markdowns, the fully loaded cost of temporary staff, and the IRS compliance traps that turn your Q4 cash pile into a tax liability. Here is how to build a seasonal break-even model that actually keeps the lights on in February.

The Core Seasonal Break-Even Formulas

These are the three equations that determine whether your seasonal business survives or fails. Keep them visible.

Q4 Peak Season Break-Even

Break-Even Revenue = Total Q4 Fixed Costs ÷ Blended Realized Margin %

Where Blended Margin accounts for both full-price holiday sales AND post-holiday markdowns

Q1-Q3 Off-Season Bridge

Monthly Cash Burn = Off-Season Fixed Costs – Minimum Off-Season Revenue

Reserve Requirement = Monthly Cash Burn × Months Until Next Peak Season

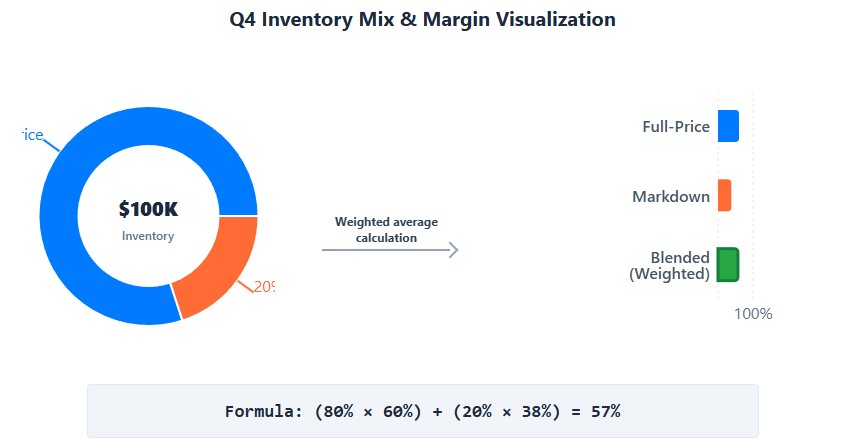

Blended Realized Margin

Blended Margin = (Full-Price % × Full-Price Margin) + (Markdown % × Markdown Margin)

Example: (80% × 60%) + (20% × 38%) = 55.6% blended margin

The One-Page Seasonal Break-Even Blueprint

Before diving into the tax code and inventory math, here is the exact step-by-step framework to align your peak season profitability with your off-season survival.

- Calculate the Blended Realized Margin: Stop using full-price margins. Factor in the 15-20% of inventory that will inevitably go to post-holiday clearance.

- Determine the Q4 Fixed Cost Spike: Isolate temporary fixed costs—pop-up leases, seasonal insurance riders, and holiday marketing.

- Compute the “Fully Loaded” Seasonal Labor Cost: Add FUTA, SUTA, and the “ramp-up” productivity loss to your temporary payroll.

- Establish the Q1-Q3 “Bridge” Break-Even: Calculate the exact monthly revenue needed to cover off-season fixed costs without touching your Q4 cash reserves.

- Secure the Liquidity Bridge: Align your SBA CAPLines or inventory financing to cover the gap between Q4 tax payments and Q2 cash flow.

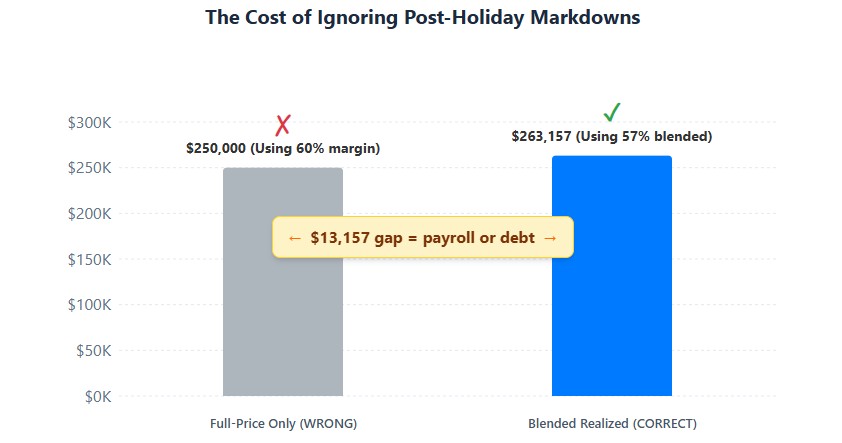

The Hidden Q4 Trap: Calculating Break-Even with Post-Holiday Markdowns

Most retail break-even formulas assume every unit sells at full price. In reality, if you don’t sell it by December 26th, you’re selling it at a discount. If your model ignores post-holiday markdowns, you will hit your break-even point on paper but still run out of cash.

You must calculate the Blended Realized Margin. This accounts for the fact that a portion of your Q4 inventory will only generate revenue in Q1 at a steep discount, while still incurring Q4 carrying costs.

| Metric | Full-Price Holiday Sales | Post-Holiday Markdowns | Blended Total |

|---|---|---|---|

| % of Total Inventory | 80% | 20% | 100% |

| Average Selling Price | $100.00 | $65.00 | $93.00 |

| Unit COGS | $40.00 | $40.00 | $40.00 |

| Contribution Margin | $60.00 (60%) | $25.00 (38%) | $53.00 (57%) |

If your Q4 fixed costs are $150,000, using the full-price margin (60%) tells you to break even at $250,000. But using the Blended Realized Margin (57%) reveals you actually need $263,157. That $13,000 gap is often the difference between making payroll in January and taking on high-interest merchant cash advance debt.

The Off-Season “Bridge” Break-Even: Funding the Q1-Q3 Desert

Q4 generates the cash, but Q1-Q3 burns it. Your off-season break-even isn’t about growth; it’s about minimizing the burn rate. The goal is to cover your baseline fixed costs (rent, core payroll, insurance, loan debt service) with the lowest possible revenue threshold.

- Calculate the Bare-Bones Burn Rate: Strip out all discretionary spending. For a mid-sized apparel retailer, this might be $18,000/month.

- Factor in Inventory Carrying Costs: Dead Q4 stock sitting in a warehouse costs roughly 2-3% of its value per month in storage, insurance, and opportunity cost. If you have $100,000 in unsold holiday inventory, that’s $2,500/month bleeding into your Q1 reserves.

- The Liquidation vs. Storage Decision: If your off-season break-even requires selling 500 units a month just to cover rent, but you’re only moving 200, you must liquidate the rest to pallet liquidators. Taking 15 cents on the dollar frees up warehouse space and stops the carrying cost bleed, effectively lowering your off-season break-even point.

Seasonal Staffing: The “Fully Loaded” Margin Killer

Retailers often plug seasonal wages directly into their variable cost model. This is a fatal error. The true cost of a seasonal hire includes payroll taxes, workers’ compensation, and the “ramp-up” period where the employee is learning the POS system and slowing down your checkout lines.

Under US tax law, you pay FICA (7.65%), FUTA (0.6% on the first $7,000 of wages), and state SUTA (which varies, but averages around 1.5% for new seasonal accounts).

- The Ramp-Up Tax: A seasonal worker making $18/hour might only generate $14/hour in net margin during their first two weeks due to training time and transaction errors.

- The Fix: Build a “fully loaded” labor cost into your Q4 break-even model. Add 12% to the base hourly wage to cover payroll taxes and workers’ comp, and allocate the first 20 hours of each hire’s schedule as a fixed training cost, not a variable sales cost. This prevents your Q4 labor expenses from silently blowing past your break-even threshold.

IRS and GAAP Traps: Layaways, LIFO, and Nexus

Your break-even model is useless if the IRS reclassifies your revenue or disallows your deductions. Seasonal retail is a minefield of compliance issues that can wipe out your Q4 profits in April.

The Layaway Trap (ASC 606)

If you take a $50 deposit for a layaway item in November, that is cash in your pocket, but it is not revenue. Under GAAP (ASC 606), it is a deferred liability until the customer takes possession of the goods. If you book it as Q4 revenue to hit your break-even target, you will fail your CPA’s review and potentially face audit flags for inflated income.

Inventory Write-Downs (IRS Pub 538)

If you are stuck with obsolete Q4 inventory, the IRS allows you to write it down to its Net Realizable Value (NRV) and deduct the loss. However, you must document the market value decline. You cannot just guess a 30% write-down; you need evidence of the actual post-holiday market price to defend the deduction during an audit.

Economic Nexus on Pop-Ups

If you run a holiday pop-up shop in a state where you don’t have a physical presence, you likely just triggered economic nexus. Selling $100,000 in a temporary Chicago warehouse means you owe Illinois sales tax. If you didn’t register beforehand, that tax comes directly out of your Q4 profit margin, instantly pushing you below your break-even point.

Actionable Next Steps for Retail Owners

Stop guessing your holiday profitability. Take these steps before Q4 inventory hits the floor.

- Run the Blended Margin Scenario: Adjust your Q4 break-even model to assume 20% of your inventory sells at a 35% discount in January. See if you still hit your target profit.

- Audit Your Seasonal Labor Costs: Add the FUTA/SUTA and ramp-up time to your temporary staffing budget. If the margin on seasonal sales drops below 15%, cap your hiring.

- Secure the Q1 Bridge Now: Do not wait until January to apply for an SBA CAPLine or seasonal line of credit. Lenders require 60-90 days to underwrite. Apply in September based on your Q4 projections.

- Separate Cash from Revenue: Set up a separate bank account for layaway deposits and gift card sales. Do not spend this cash on Q4 inventory; it belongs to Q1 fulfillment.

- Plan the Post-Holiday Liquidation: Decide in August which SKUs will be marked down and which will be sent to liquidators. Pre-negotiate pallet buyer contracts so you aren’t paying Q1 storage fees on dead Q4 stock.

Seasonal retail is a game of cash flow timing, not just holiday volume. By modeling your break-even point around the blended reality of markdowns, fully loaded labor, and off-season burn rates, you transform Q4 from a stressful gamble into a predictable funding engine for the rest of the year.