In 2026, the “growth at all costs” era is dead. With the Federal Funds Rate holding steady and venture capital tightening, startup founders can no longer afford to price products based on optimistic projections. If your go-to-market (GTM) pricing strategy does not clear your break-even point after accounting for hidden fees, state taxes, and customer acquisition costs, you are not building a business—you are burning runway.

A break-even pricing strategy is not just an accounting exercise. It is your absolute price floor. It tells you the minimum viable price required to cover your fixed and variable costs at a specific unit volume. Getting this math wrong leads to cash flow collapse, while getting it right gives you the leverage to negotiate with investors, suppliers, and early customers.

The Core Break-Even Pricing Formulas

Before building a complex financial model, you need to master these three foundational equations. Keep them visible to your entire leadership team.

1. Contribution Margin per Unit

Contribution Margin = Selling Price – Total Variable Cost per Unit

(This is the actual cash each sale contributes to paying off your fixed costs.)

2. Break-Even Point (in Units)

Break-Even Units = Total Monthly Fixed Costs ÷ Contribution Margin per Unit

(This is the exact number of units you must sell every month to reach $0 net profit/loss.)

3. Minimum Viable Price (MVP) with CAC Allocation

Minimum Price = (Monthly Fixed Costs ÷ Target Monthly Volume) + Variable Cost per Unit + (CAC ÷ Expected Lifetime Units per Customer)

(This is the true price floor when you factor in customer acquisition. Most founders forget CAC in their break-even math, which is why they run out of cash even when hitting unit break-even.)

For example, if your CAC is $150 and the average customer buys 5 units over their lifetime, you must allocate $30 of CAC to every unit sold. That $30 is a hidden variable cost that must be covered by your price.

The 4-Step GTM Pricing Framework for US Startups

Building a defensible pricing model requires bridging financial discipline with market reality. Follow this four-step framework to ensure your pricing is both profitable and compliant.

Step 1: Isolate True Fixed and Variable Costs (The IRS Reality)

Founders often inflate their monthly break-even point by including one-time startup costs. Under IRS rules (IRC §195), pre-launch expenses like R&D and initial marketing must be amortized over 180 months, not deducted fully upfront. For the statutory language on startup expenditures and 180-month amortization, see: https://www.law.cornell.edu/uscode/text/26/195

For a practitioner overview of how startup and expansion costs are deducted and amortized, see: https://www.thetaxadviser.com/issues/2017/sep/deducting-startup-expansion-costs/

For your break-even model, only include recurring operational fixed costs: office rent, core SaaS subscriptions, base salaries, and insurance. For variable costs, go beyond just Cost of Goods Sold (COGS). You must include shipping, payment processing fees, and direct labor.

Step 2: Factor in the “Hidden” Variable Costs

Most startup pricing models fail because they ignore the microscopic costs that bleed margins dry. If you are selling a physical product or a digital service, your variable cost per unit must include:

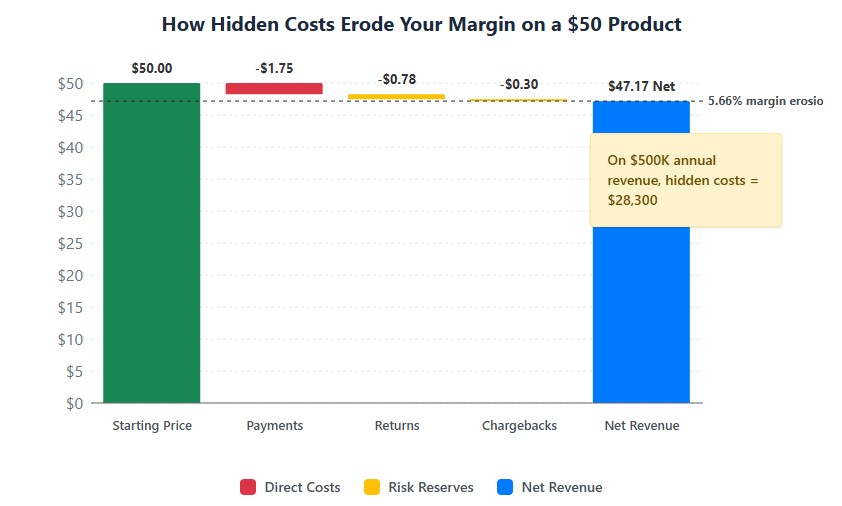

- Payment Processing: Standard rates are typically 2.9% + $0.30 per transaction. Typical online credit card processing fees fall in the 1.5%–3.5% range, with many providers charging around 2.9% + $0.30 for card-not-present transactions: https://www.nerdwallet.com/business/software/learn/credit-card-processing-fees On a $50 item, that is roughly $1.75 gone immediately.

- Return Logistics: For DTC e-commerce, average return rates hover around 12% (industry benchmark range: 10–20% depending on category). You must amortize the cost of reverse logistics (roughly $6.50 per return on average) and restocking labor across all units sold.

- Economic Nexus Sales Tax: Many states now use economic nexus thresholds (often around $100,000 in sales, sometimes with transaction-count tests), but rules vary by jurisdiction. Always confirm using an up-to-date nexus chart: https://taxcloud.com/blog/sales-tax-nexus-by-state/ If your pricing is tax-inclusive (rare in the US, but common in B2B contracts), this can instantly erase 4% to 10% of your margin.

- Chargebacks and Fraud: Budget at least 0.6% of gross revenue for payment disputes (range: 0.3%–1.5% depending on vertical), especially in high-risk categories like supplements or digital goods.

Step 3: Stress-Test Against Willingness to Pay

Once you have your break-even price, you must validate it against the market. If your math says you must charge $85 to break even, but customer discovery (via Van Westendorp pricing surveys) shows a maximum willingness to pay of $60, your business model is broken. You cannot fix a unit economics problem with marketing.

In this scenario, you have only two levers: drastically reduce your fixed/variable costs, or pivot to a higher-value customer segment that justifies the $85 price point.

Step 4: Align with SBA and Investor Metrics

If you plan to seek debt financing (like an SBA 7(a) loan) or venture capital, your pricing must support broader financial health metrics. For SaaS startups, lenders look for an LTV:CAC (Lifetime Value to Customer Acquisition Cost) ratio of 3:1 or higher. For physical products, they want to see a gross margin of at least 40-50% to absorb supply chain shocks.

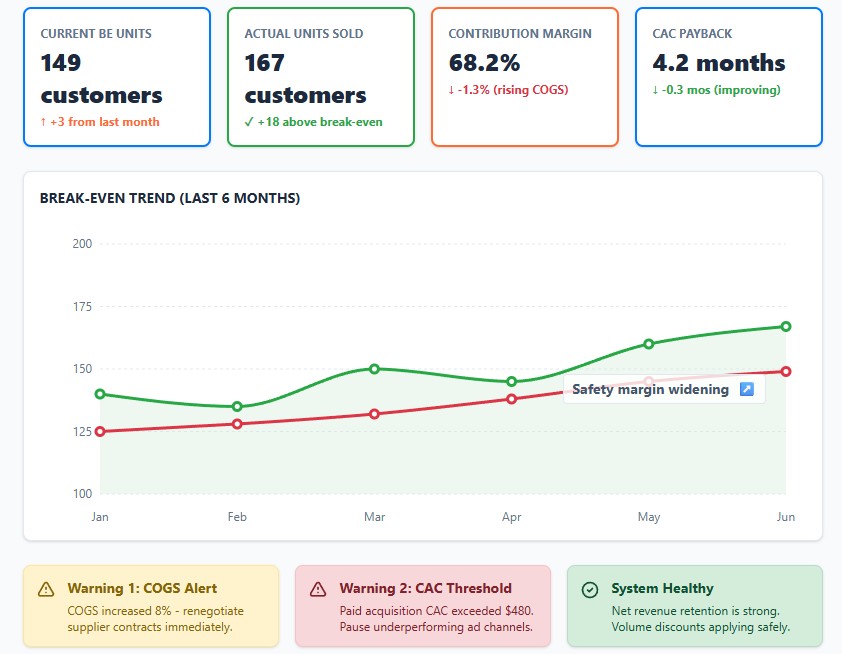

Real-World Case Study: B2B SaaS Break-Even in Texas

Let’s look at a practical example of a B2B SaaS startup launching a field-service management tool in Texas.

- Monthly Fixed Costs: $15,000 (Includes cloud hosting, 2 core developers, basic software stack, and general liability insurance).

- Selling Price: $150 per month per customer.

- Variable Costs per Unit: $30 (Includes $15 for incremental server usage, $10 for customer support allocation, and $5 for payment gateway fees and taxes).

- CAC: $450 per customer, with an average customer lifetime of 24 months.

The Math:

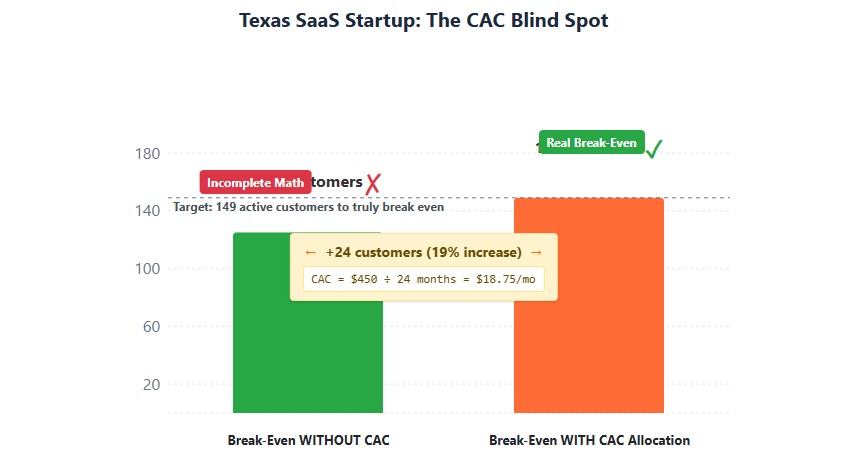

Contribution Margin = $150 – $30 = $120

Break-Even Units = $15,000 ÷ $120 = 125 active customers.

But wait—CAC allocation:

CAC per month = $450 ÷ 24 months = $18.75 per customer per month

True Break-Even Units = $15,000 ÷ ($120 – $18.75) = 149 active customers.

That 19% difference between 125 and 149 customers is the gap that kills startups who forget to allocate CAC into their break-even math.

The State Tax Nuance:

Texas imposes a franchise tax of 0.75% on margin for entities with revenue over a certain threshold. See Texas Tax Code §171.002 for the standard 0.75% franchise tax rate on taxable margin: https://www.jdsupra.com/legalnews/how-to-compute-the-texas-franchise-tax-1432811/ While this might seem small, as the startup scales past $1 million in Annual Recurring Revenue (ARR), that 0.75% effectively increases the variable cost per unit, pushing the true break-even point from 149 customers to roughly 152 customers. Modeling this early prevents nasty surprises during annual tax filings.

Numeric Case Study: When Break-Even Price Exceeds Willingness to Pay

Here is a real-world DTC e-commerce scenario where the math forced a pivot. A startup selling premium organic skincare products faced the following unit economics:

- Monthly Fixed Costs: $22,000 (warehouse lease, 3 FTE staff, Shopify Plus, marketing tools)

- COGS per unit: $18 (product + packaging)

- Shipping: $7.50 (average across zones)

- Payment processing: $2.10 (2.9% + $0.30 on $62 average order)

- Return reserve: $1.80 (12% return rate × $15 avg reverse logistics cost)

- Total variable cost per unit: $29.40

- CAC: $38 per customer, with 1.4 purchases per customer on average

- CAC per unit: $38 ÷ 1.4 = $27.14

Break-Even Calculation at Target Volume (1,500 units/month):

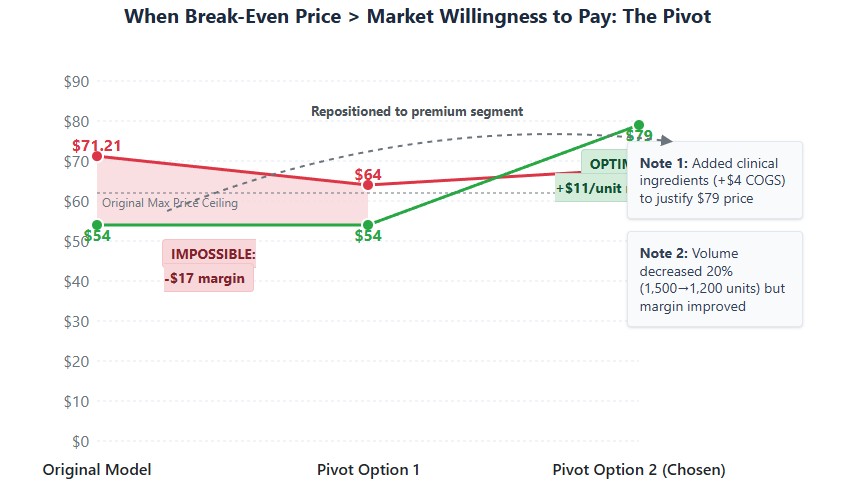

Minimum Price = ($22,000 ÷ 1,500) + $29.40 + $27.14 = $14.67 + $29.40 + $27.14 = $71.21

The Market Reality:

Van Westendorp surveys showed the optimal price point was $54, with a maximum acceptable price of $62. The break-even price of $71.21 exceeded the market’s ceiling by $9.

The Pivot:

The founders had three options: (1) raise prices to $72 and accept slow growth, (2) cut costs, or (3) reposition the product. They chose option 3—reformulated the product to justify a $79 price point by adding clinically-proven active ingredients, which increased COGS by $4 but moved the product into a premium segment where $79 was within the willingness-to-pay range. The new break-even at 1,200 units/month dropped to $68, safely below the new $79 price.

This is the kind of hard math that separates startups that survive from those that burn through their seed round and die.

Risk & Compliance: Pricing Guardrails to Avoid Audit Triggers

Your pricing strategy must also survive regulatory scrutiny. The IRS and state authorities monitor specific pricing behaviors that can trigger audits or penalties.

- Transfer Pricing (IRC §482): If your US startup has a foreign subsidiary and you license IP or sell services to them at artificially low prices to shift profits offshore, the IRS will reallocate your income and penalize you. Maintain benchmark studies to prove your intercompany pricing reflects “arm’s length” market rates.

- Deceptive Discounting: The FTC Act Section 5 and state consumer protection laws (like NY General Business Law §349) strictly enforce rules against fake “was/now” pricing. If you claim a product is “$199, now $99,” but it never actually sold at $199, you face fines and enforcement actions. The FTC requires that the “original” price be a genuine, recent price at which the product was openly sold.

- Worker Misclassification: If you use gig workers for fulfillment or sales and classify them as 1099 contractors to keep variable costs low, you risk severe penalties under laws like California’s AB 5. For an overview of how AB5 applies the “ABC test” to determine employee vs. independent contractor status, see: https://www.lock-law.com/information-on-california-ab5-law/ If reclassified as W-2, your variable labor costs will instantly spike by 20-30%, destroying your break-even model.

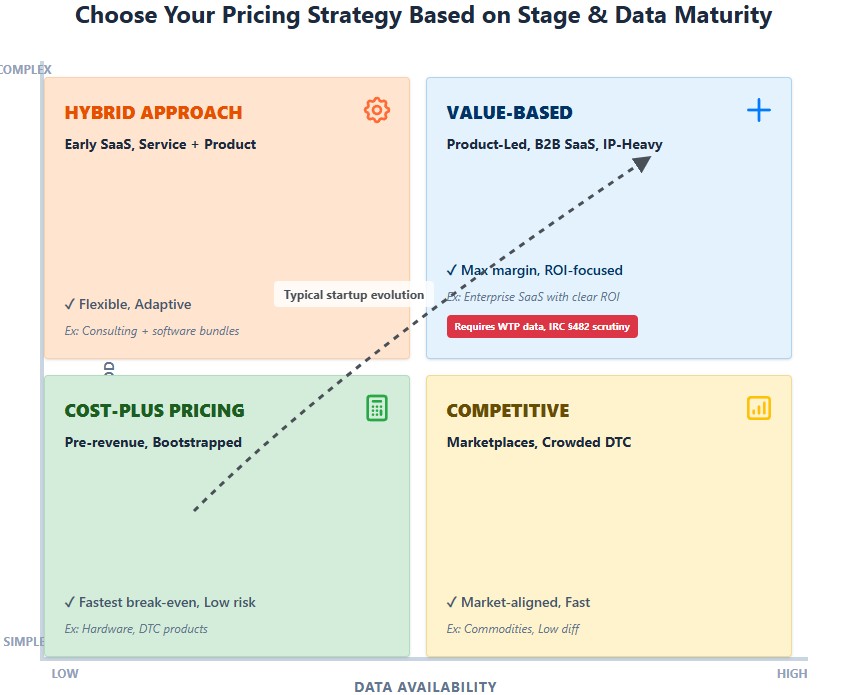

Choosing the Right Pricing Strategy for Your Stage

Not every startup should use the same pricing model. Match your approach to your current stage and data maturity.

| Pricing Model | Best For | Break-Even Speed | Primary Risk |

|---|---|---|---|

| Cost-Plus Pricing | Pre-revenue, bootstrapped, or high-COGS hardware/DTC startups. | Fastest (guarantees margin) | Leaves money on the table; ignores customer value. |

| Value-Based Pricing | Product-led, B2B SaaS, or IP-heavy models with clear ROI for the buyer. | Variable (requires deep market validation) | High scrutiny on intercompany transactions; requires robust data. |

| Competitive Pricing | Marketplaces, crowded DTC spaces, or low-differentiation commodities. | Fast, but highly margin-sensitive | Price wars; vulnerable to supply chain cost spikes. |

Practical Next Steps for Founders

Do not wait until you are out of cash to fix your pricing. Take these actions this quarter:

- Audit Your Variable Costs: Pull your last three months of bank statements. Add up every single fee tied to a sale (processing, shipping, returns, support) to find your true variable cost per unit.

- Calculate Your Floor with CAC: Run the Minimum Viable Price formula using your current fixed costs and CAC allocation. This is your absolute price floor. Do not run promotions that dip below this number without a documented, time-bound customer acquisition strategy.

- Stress-Test for Nexus: If you sell digitally or ship nationally, map out which states you are close to crossing the economic nexus threshold, and factor that future tax burden into your margin today.

- Validate with the Market: Before writing more code or ordering more inventory, use SBA customer discovery templates or tools like Prisync to confirm that buyers will actually pay your break-even price.

- Run the WTP vs. Break-Even Test: If your break-even price exceeds your customer’s maximum willingness to pay, you have a business model problem—not a marketing problem. Pivot or cut costs before you launch.

Pricing is not a set-it-and-forget-it decision. As your startup scales, your fixed costs will grow, and your variable costs should shrink through economies of scale. Revisit your break-even model monthly to ensure your GTM strategy remains grounded in financial reality.

Disclaimer: This article provides general business and financial information. Tax laws and regulations vary by jurisdiction and change frequently. Consult with a qualified CPA or tax advisor before making pricing, tax, or compliance decisions for your business.