In 2026, with commercial interest rates still elevated (prime rate above 8%) and credit standards tightening, banks are more conservative than ever. They’ve been burned by businesses that looked great on tax returns but ran out of cash six months later. So they’ve shifted their focus from “How much profit did you make?” to “Can you prove you have the cash to repay us?”

This guide explains exactly how lenders evaluate cash flow, what they’re looking for, and how to position your business for approval—even if your net income looks weak on paper.

The Fundamental Difference: Profit vs. Cash Flow

Before we dive into lender requirements, let’s clarify what we’re talking about. These two metrics tell very different stories about your business.

Net Profit (What Your Tax Return Shows)

Net profit is what’s left after you subtract all expenses from revenue. It’s calculated using accrual accounting (for most businesses), which means:

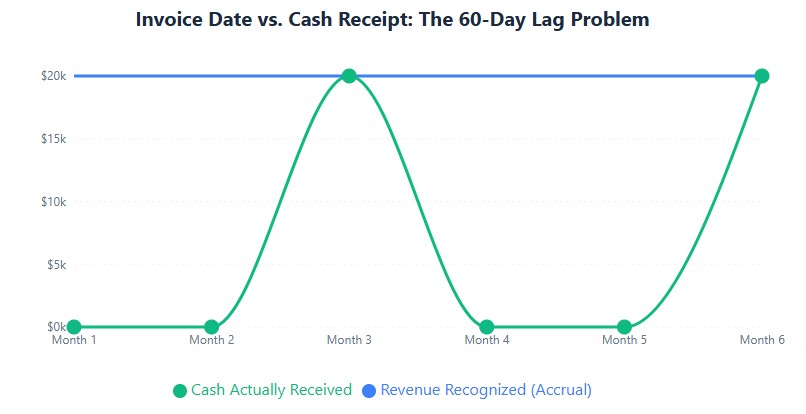

- Revenue is recorded when earned, not when you get paid. If you invoice a client $10,000 in December but they pay in February, that $10K shows up in your December profit.

- Expenses are recorded when incurred, not when you pay them. If you buy $5,000 in supplies in March but pay the bill in April, that $5K expense hits your March P&L.

- Non-cash items reduce profit. Depreciation on equipment, amortization of intangible assets—these reduce your taxable income but don’t actually cost you cash this year.

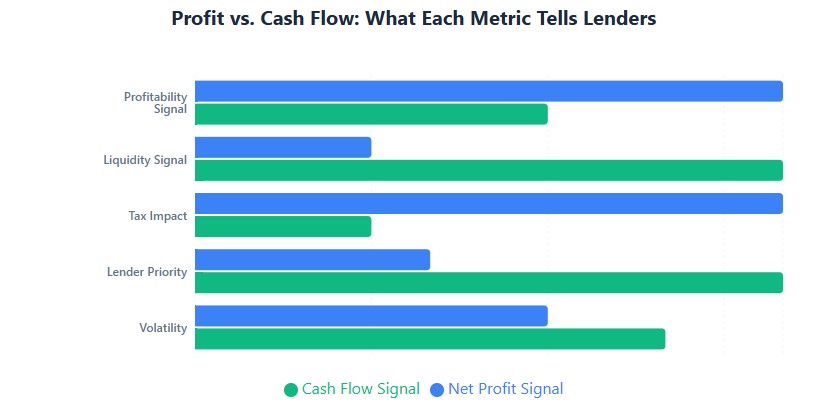

The problem: Net profit tells you if your business model works. It doesn’t tell you if you can pay your bills next month.

Operating Cash Flow (What Lenders Actually Care About)

Operating cash flow is the actual cash moving in and out of your bank account. It answers: “After paying suppliers, employees, rent, and taxes, how much cash is left?”

Here’s the key difference:

| Scenario | Impact on Net Profit | Impact on Cash Flow |

|---|---|---|

| You invoice a client $20,000 in March (payment due in 60 days) | + $20,000 revenue in March | $0 cash in March (money hasn’t arrived yet) |

| You buy $15,000 in inventory on Net-30 terms | $0 expense in March (you haven’t paid yet) | $0 cash out in March (bill not due) |

| You depreciate a $50,000 piece of equipment over 7 years | – $7,143 expense per year (non-cash) | $0 cash out (you already paid for it) |

| A client pays a $10,000 invoice 90 days late | $0 impact (revenue was recorded when invoiced) | + $10,000 cash in (finally arrived) |

The takeaway: A business can be profitable but cash-poor (if clients pay late or inventory piles up). Or it can show a loss but generate strong cash flow (if depreciation is high but operations are lean).

Lenders know this. That’s why they look beyond your tax return.

How Lenders Actually Evaluate Your Cash Flow

When you apply for a business loan, the underwriter doesn’t just glance at your net income and make a decision. They reconstruct your cash flow using a specific methodology. Here’s exactly what they do.

Step 1: Start with Your Tax Return Net Income

They pull your last 2-3 years of tax returns (Form 1120 for C-corps, 1120-S for S-corps, 1065 for partnerships, or Schedule C for sole proprietors). This is your starting point.

Step 2: Add Back Non-Cash Expenses

These reduce your taxable income but don’t actually cost you cash:

- Depreciation: The gradual write-off of equipment, vehicles, furniture. Found on Form 4562.

- Amortization: Similar to depreciation, but for intangible assets (patents, trademarks, startup costs).

- Depletion: For natural resource businesses (mining, oil, timber).

Example: Your HVAC company shows a $50,000 net loss. But you have $130,000 in equipment depreciation. Lenders add that back: -$50K + $130K = $80,000 in “adjusted” cash flow.

Step 3: Add Back Discretionary or One-Time Expenses

Lenders understand that business owners sometimes run personal expenses through the business, or have one-time costs that won’t repeat. They’ll add these back if you can document them:

- Excess owner compensation: If you pay yourself $150,000 but a market-rate salary for your role is $90,000, lenders may add back the $60,000 excess. (You’ll need to justify this with industry salary data.)

- Personal expenses: Personal vehicle lease, family travel, club memberships—anything clearly not business-related.

- One-time losses: Lawsuit settlement, equipment theft, storm damage. Must be documented and non-recurring.

- Interest expense: Since DSCR measures your ability to service new debt, lenders add back interest on existing debt.

Warning: Don’t get creative here. Lenders will ask for receipts, contracts, or third-party verification. If you claim a $30,000 “consulting expense” add-back but have no invoice or contract, that’s a red flag.

Step 4: Subtract Non-Recurring Revenue

Just like they add back one-time expenses, they’ll subtract one-time revenue. If you sold a piece of equipment for $40,000, that’s not recurring operating cash flow. It gets removed.

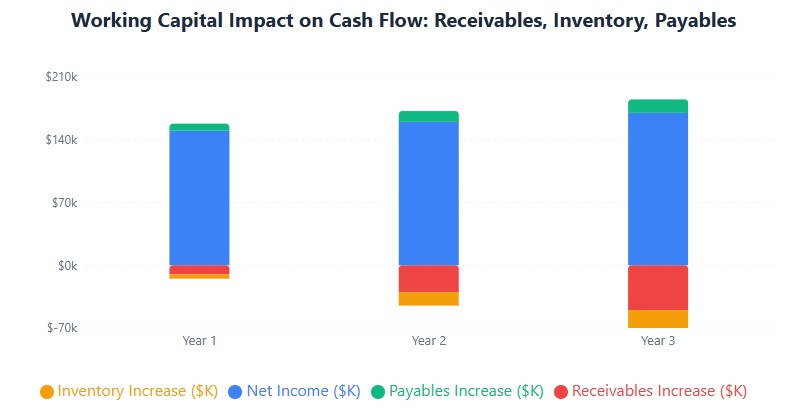

Step 5: Adjust for Working Capital Changes

This is where it gets technical, but it’s critical. Lenders look at how your receivables, inventory, and payables are trending:

- Receivables increasing? That means clients are paying slower. Cash is tied up in unpaid invoices. Lenders may reduce your cash flow by the increase in receivables.

- Inventory increasing? You’re buying more stock than you’re selling. Cash is sitting on shelves. Lenders may reduce cash flow.

- Payables increasing? You’re taking longer to pay suppliers. That’s actually good for cash flow (you’re holding onto cash longer). Lenders may add this back.

Example: Your adjusted cash flow is $200,000. But your accounts receivable increased by $50,000 last year (clients paying slower). Lenders subtract that: $200K – $50K = $150,000 in “normalized” cash flow.

Step 6: Calculate Debt Service Coverage Ratio (DSCR)

This is the magic number. DSCR measures how many times your cash flow covers your debt payments.

Formula:

DSCR = Cash Flow Available for Debt Service ÷ Total Annual Debt Payments

Example:

- Your normalized cash flow: $180,000

- Your existing loan payments: $40,000/year

- New loan payment you’re applying for: $60,000/year

- Total debt service: $100,000

- DSCR = $180K ÷ $100K = 1.80x

What does 1.80x mean? It means your cash flow covers your debt payments 1.8 times. You have an 80% cushion. If your revenue drops 40%, you can still make your loan payments.

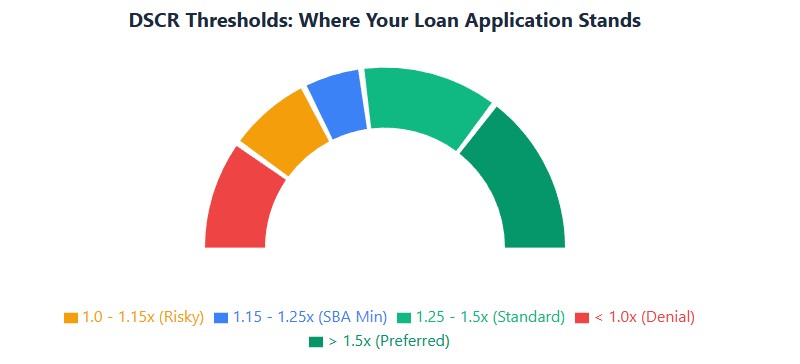

What’s a good DSCR?

| DSCR | What It Means | Lender Reaction |

|---|---|---|

| Below 1.0x | You don’t generate enough cash to cover debt payments | Automatic denial. You’re losing money on this loan. |

| 1.0x – 1.15x | Barely covering debt. No room for error. | High risk. Most traditional lenders will decline. Online lenders might approve at high interest rates. |

| 1.15x – 1.25x | Adequate coverage, but tight. | SBA 7(a) minimum threshold. May require strong collateral or personal guarantees. |

| 1.25x – 1.50x | Good coverage. Comfortable cushion. | Standard approval range for most SBA and bank loans. |

| Above 1.50x | Strong coverage. Very low risk. | Preferred borrower. May qualify for best rates and terms. |

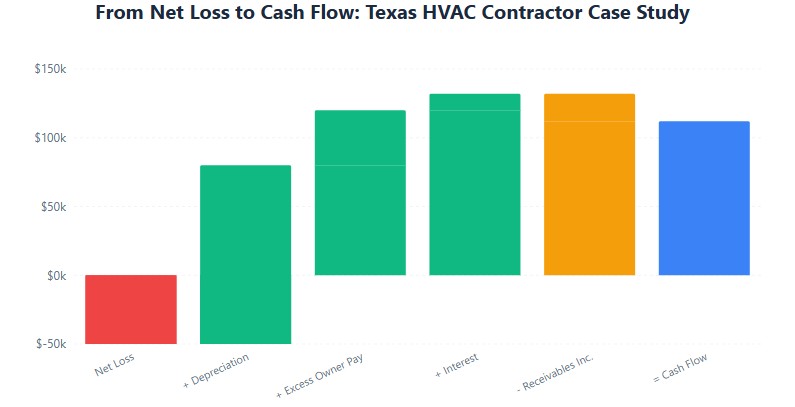

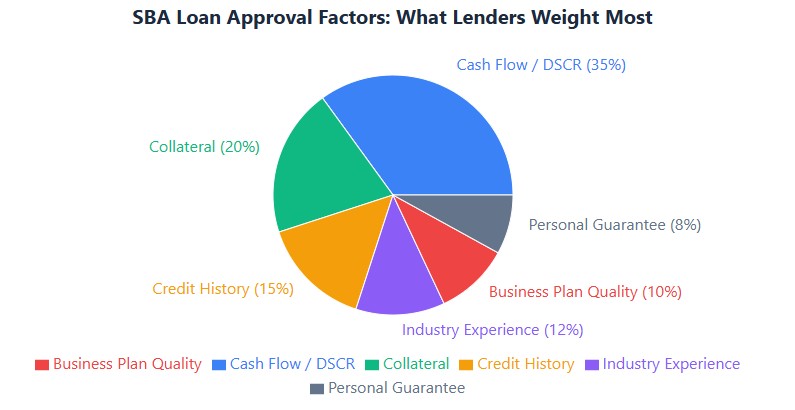

Real Case Study: How a “Loss-Making” Business Got a $300K SBA Loan

Let’s walk through a real example to show how this works in practice.

Business: Texas HVAC contractor, 8 years in business

Revenue: $850,000

Net Profit (on tax return): -$50,000 loss

Loan Request: $300,000 SBA 7(a) for equipment and working capital

On paper, this business looks like a bad bet. It’s losing money. Why would a lender approve a $300K loan?

Here’s what the lender saw when they reconstructed the cash flow:

| Line Item | Amount | Why |

|---|---|---|

| Net Loss (from tax return) | -$50,000 | Starting point |

| + Depreciation (equipment, vehicles) | +$130,000 | Non-cash expense. Equipment was paid for in prior years. |

| + Excess owner compensation | +$40,000 | Owner paid himself $140K, but market rate for HVAC owner is $100K. Added back $40K excess. |

| + Interest on existing debt | +$12,000 | Existing loan interest. New DSCR will include this payment. |

| – Increase in receivables | -$20,000 | Clients paid 15 days slower this year. Cash tied up. |

| Cash Flow Available for Debt Service | $112,000 |

Debt Service Calculation:

- Existing loan payment: $40,000/year

- Proposed new loan payment ($300K, 10 years, 8%): $74,000/year

- Total annual debt service: $114,000

DSCR: $112,000 ÷ $114,000 = 0.98x

Wait—that’s below 1.0x. That should be a denial, right?

Not necessarily. Here’s what saved this application:

- Strong collateral: The business owned $200,000 in equipment (free and clear) that could be pledged.

- Personal guarantees: The owner had a personal net worth of $400,000 (home equity, retirement accounts).

- Improving trend: Receivables had been increasing for two years, but the owner implemented stricter collection policies. The lender projected receivables would stabilize, adding back $20K to cash flow.

- Adjusted DSCR: $132,000 ÷ $114,000 = 1.16x (meets SBA minimum).

Outcome: Loan approved. The lender was confident that the business generated enough cash to service the debt, even though the tax return showed a loss.

The lesson: Net profit is just the starting point. Lenders care about cash flow, collateral, and your ability to repay.

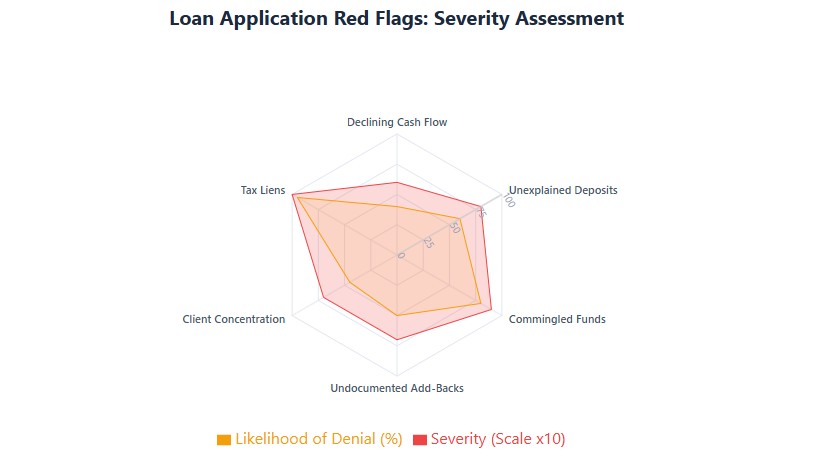

Red Flags That Kill Loan Applications

You can have great cash flow and still get denied if your application raises red flags. Here’s what makes lenders nervous:

1. Inconsistent or Declining Cash Flow

If your cash flow was $200K in 2024, $150K in 2025, and $100K in 2026, lenders see a business in decline. Even if your current DSCR is 1.30x, they’ll worry it’ll drop below 1.0x next year.

Fix: If your cash flow is declining, explain why (one-time event, market downturn) and show how you’re fixing it. Provide projections that demonstrate recovery.

2. Unexplained Bank Deposits

Lenders will request 12-24 months of business bank statements. If they see $15,000 deposits with no corresponding invoices or explanations, they’ll assume you’re underreporting income or mixing personal and business funds.

Fix: Keep clean books. Every deposit should match an invoice, contract, or documented source. If you have unusual deposits (loan proceeds, equipment sales), document them.

3. Commingling Personal and Business Funds

If you pay your mortgage from your business checking account, or deposit client checks into your personal account, lenders see this as financial indiscipline. It also makes it impossible to verify your true business cash flow.

Fix: Open separate business and personal accounts. Pay yourself a regular “owner’s draw” or salary, then use personal funds for personal expenses. Do this for at least 12 months before applying.

4. Aggressive or Undocumented Add-Backs

If you claim a $50,000 “personal expense” add-back but can’t provide receipts or a clear explanation, lenders will reject it. Worse, they’ll question your credibility.

Fix: Only add back expenses you can document. Work with your CPA to identify legitimate add-backs and gather supporting documentation (receipts, contracts, industry salary surveys).

5. High Customer Concentration

If 60% of your revenue comes from one client, lenders see massive risk. If that client leaves or pays late, your cash flow collapses.

Fix: Diversify your client base. If you’re concentrated, show a pipeline of new clients or contracts that reduce dependency. Some lenders may require a “key client” letter confirming ongoing business.

6. Recent Tax Liens or Judgments

Unpaid IRS payroll taxes or civil judgments signal financial distress. Most lenders will decline your application outright.

Fix: Resolve liens or set up payment plans before applying. Provide documentation showing you’re current. Some SBA lenders may consider applications if you have a payment plan in place, but it’s an uphill battle.

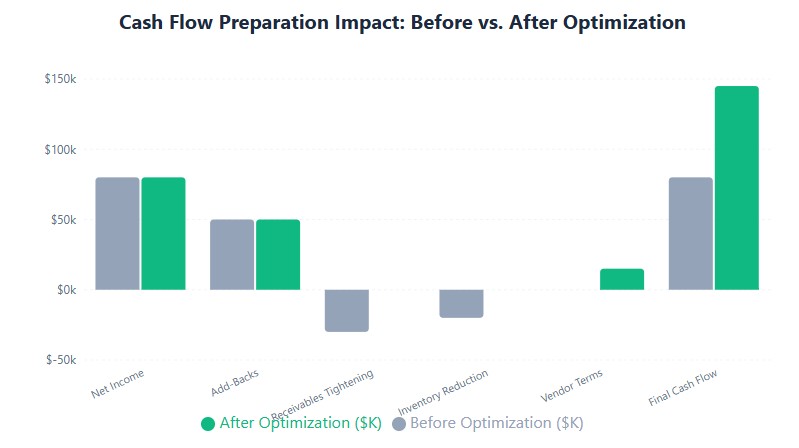

How to Prepare Your Cash Flow for Loan Approval

If you’re planning to apply for a business loan in the next 6-12 months, start preparing now. Here’s your action plan:

6-12 Months Before Applying

- Separate personal and business finances. Open a dedicated business checking account. Stop paying personal expenses from business accounts. Pay yourself a regular draw.

- Tighten your receivables. If clients are paying in 60 days, push for Net-30 terms. Offer 2% discounts for early payment. Send invoices immediately (don’t batch them at month-end). Follow up on overdue invoices weekly.

- Reduce inventory bloat. If you’re holding $100K in inventory but only turning it over twice a year, you’re tying up cash. Run clearance sales on slow-moving items. Switch to just-in-time ordering where possible.

- Negotiate longer vendor terms. If you’re paying suppliers Net-15, ask for Net-30 or Net-45. This keeps cash in your account longer.

- Build a cash reserve. Aim for 3-6 months of operating expenses in a business savings account. This shows lenders you can handle temporary cash flow dips.

3-6 Months Before Applying

- Reconstruct your financials the way a lender would. Work with your CPA to create a “lender-ready” P&L that adds back depreciation, amortization, and excess owner compensation. Calculate your DSCR.

- Order your tax transcripts. Use IRS Form 4506-T to get official transcripts for the last 2-3 years. Lenders will request these anyway—get them early to verify accuracy.

- Organize your bank statements. Download 24 months of business bank statements. Categorize all deposits and withdrawals. Be ready to explain any unusual transactions.

- Get your business credit report. Pull reports from Dun & Bradstreet, Experian Business, and Equifax Small Business. Dispute any errors. Pay down high balances.

- Prepare a cash flow projection. Create a 12-month projection showing expected cash inflows, outflows, and debt service. Show how you’ll maintain a DSCR above 1.25x.

1-3 Months Before Applying

- Pre-qualify with a lender. Before formally applying, schedule a call with a commercial loan officer or SBA lender. Share your financials and ask: “Based on this, would I qualify? What gaps do you see?” This saves you time and gives you a roadmap.

- Compile your loan package. Gather:

- 2-3 years of business tax returns (with all schedules)

- 2-3 years of personal tax returns (for owners with 20%+ stake)

- 24 months of business bank statements

- Year-to-date P&L and balance sheet

- Business debt schedule (all existing loans, balances, payments)

- Accounts receivable aging report

- 12-month cash flow projection

- Business plan (for SBA loans)

- Write a cash flow narrative. Don’t just submit numbers—explain them. If your cash flow dipped in 2025, explain why (e.g., “We invested $80K in new equipment, which increased depreciation but will boost capacity in 2026”). If you have large receivables, explain your collection process.

- Review add-backs with your CPA. Make sure every add-back is defensible and documented. Prepare a one-page summary listing each add-back, the amount, and the supporting documentation.

Which Loan Product Fits Your Cash Flow Profile?

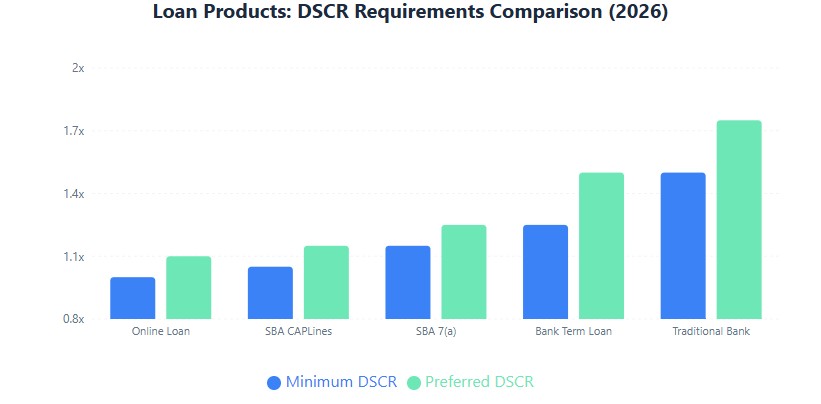

Not all business loans are created equal. Different products have different cash flow requirements. Here’s how to match your situation to the right financing:

| Loan Type | DSCR Requirement | Cash Flow History Needed | Best For | Typical Rates (2026) |

|---|---|---|---|---|

| SBA 7(a) Loan | 1.15x – 1.25x minimum | 2+ years of consistent cash flow | Long-term growth, real estate, equipment, acquisition | Prime + 2-3% (8.5-11%) |

| SBA 504 Loan | 1.15x – 1.25x | 2+ years, strong collateral | Commercial real estate, major equipment | Fixed rate, 5-6% |

| Traditional Bank Term Loan | 1.25x – 1.50x | 3+ years, strong financials | Established businesses with excellent credit | Prime + 1.5-3% (8-10%) |

| SBA CAPLines | 1.0x – 1.15x | Seasonal or project-based cash flow | Working capital, seasonal inventory, contract performance | Prime + 2-3% |

| Business Line of Credit | 1.0x – 1.15x | 1-2 years, can be less formal | Cash flow smoothing, emergency funds, short-term needs | Prime + 3-5% (variable) |

| Online Term Loan | 1.0x or less | 6-12 months, bank statements only | Fast funding, businesses that don’t qualify for bank loans | 10-30% APR |

| Invoice Factoring | Not based on DSCR | Strong receivables, B2B clients | Cash flow tied up in slow-paying invoices | 1-5% of invoice value per month |

Key takeaway: If your DSCR is below 1.15x, traditional bank loans and SBA 7(a) loans will be tough. Consider SBA CAPLines, a line of credit, or invoice factoring. If your DSCR is above 1.50x, you’re in a strong position—shop around for the best rates.

Frequently Asked Questions

What if my business is profitable but has negative cash flow?

This usually means your cash is tied up in receivables or inventory. For example, you might have $500K in sales but $400K in unpaid invoices. Solutions: tighten collection policies, offer early-payment discounts, apply for invoice factoring, or get a line of credit to bridge the gap.

Can I use personal income to boost my DSCR?

Sometimes. If you have a side job or rental income, some lenders will consider it if it’s documented and likely to continue. But most SBA lenders focus on business cash flow. Personal income is more relevant for sole proprietors or if you’re providing a personal guarantee.

How do lenders verify my cash flow?

They cross-check everything. Tax returns are compared to bank statements. If your tax return shows $300K in revenue but your bank deposits total $400K, they’ll ask why (maybe you’re underreporting, or maybe you have non-revenue deposits like loan proceeds). Be ready to explain every discrepancy.

What if I’m a startup with no cash flow history?

Traditional lenders won’t touch you. Your options: SBA microloans (up to $50K, more flexible on history), online lenders (will approve based on personal credit and projected cash flow), or bootstrapping. You’ll need a strong business plan and personal collateral.

Do lenders look at my personal credit score?

Yes. For small businesses (especially those under $5M in revenue), lenders almost always require a personal guarantee. They’ll pull your personal credit report. A score below 680 makes approval harder. Below 640, most traditional lenders will decline.

How long does the loan approval process take?

SBA 7(a) loans: 60-90 days (sometimes longer). Traditional bank loans: 30-60 days. Online lenders: 1-7 days. Start early and have your documents ready to avoid delays.

Final Thoughts

Lenders don’t care about your profit. They care about your cash flow. That’s the reality of business lending in 2026.

But here’s the good news: you can have a weak-looking tax return and still get approved if you can demonstrate strong, consistent cash flow. The key is understanding how lenders think, preparing your financials the way they want to see them, and addressing red flags before you apply.

Start preparing now. Separate your finances. Tighten your receivables. Build a cash reserve. Work with your CPA to reconstruct your financials. And when you’re ready, pre-qualify with a lender before formally applying.

Get this right, and you’ll stop getting denied. You’ll start getting funded.