For most US e-commerce brands, Q4 isn’t just another quarter. It’s 40% to 70% of your entire year’s revenue, packed into 60 days.

But here is the brutal reality that kills otherwise successful brands: Revenue is vanity. Cash is sanity.

You can have a record-breaking Black Friday, but if your payment processor places a 15% rolling reserve on your funds, your inventory supplier demands Net-15 terms, and your Q4 ad spend spikes, you will face a January cash crunch. Add in the IRS’s aggressive cross-referencing of the new $600 1099-K threshold against state sales tax filings, and a simple forecasting error can turn into an audit or a liquidity crisis.

This guide cuts through the accounting jargon. It provides a step-by-step, actionable framework to forecast your Q4 cash flow, secure the right financing, and avoid the hidden traps that drain e-commerce bank accounts during the holidays.

The Q4 Cash Flow Trap: Why Profit Doesn’t Equal Cash

Under GAAP accounting (ASC 606), you recognize revenue when the product ships. But your bank account doesn’t care about GAAP. It cares about when the cash actually settles.

During Q4, three massive forces widen the gap between your reported profit and your actual cash:

- Processor Rolling Reserves: Stripe, PayPal, and Shopify Payments monitor chargeback rates closely. If your dispute rate creeps above 0.9% during the holiday rush, they will automatically hold 10% to 20% of your daily volume for up to 90 days. That is cash you cannot use to buy January inventory.

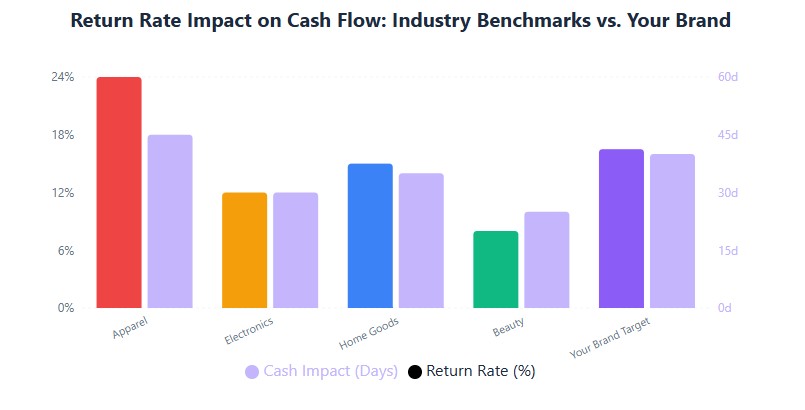

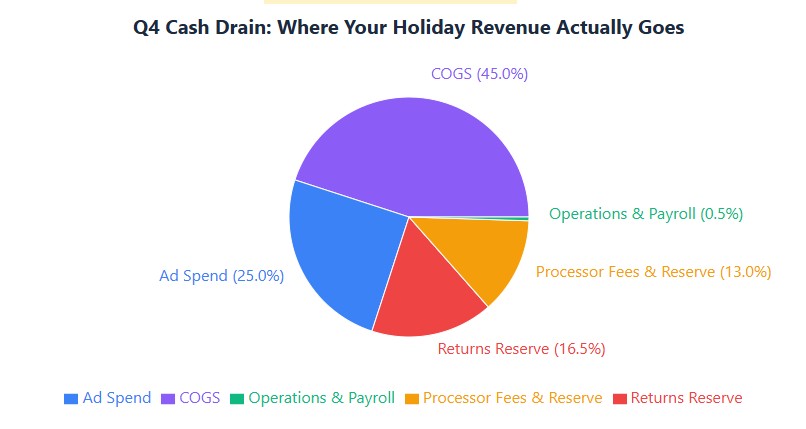

- The Return Lag: The National Retail Federation (NRF) reports an average post-holiday return rate of 16.5%. You pay for the outbound shipping, the COGS, and the ad spend in November. The refund hits your account in January, but the cash is already gone.

- Peak Season Surcharges: UPS and FedEx implement peak season surcharges (up 6.9% year-over-year for 2026). If your free-shipping threshold isn’t adjusted, these fees will eat directly into your working capital.

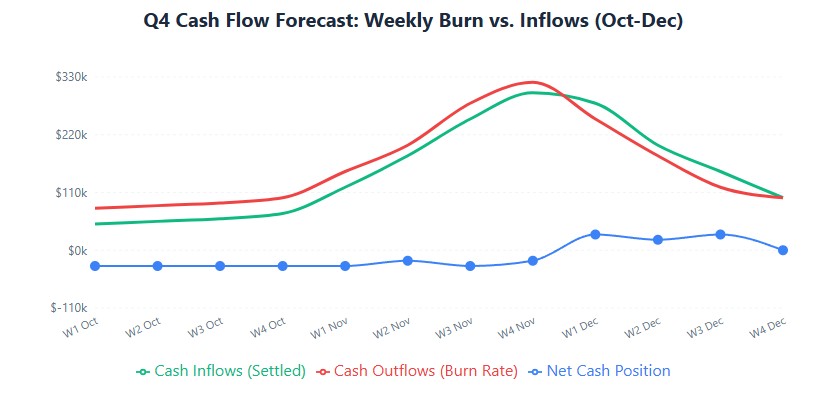

Step-by-Step: Building a Bulletproof Q4 Cash Flow Forecast

Do not rely on a static annual budget. You need a rolling, weekly cash flow model for October, November, and December. Here is how to build it.

Step 1: Forecast “Settled” Net Sales (Not Gross)

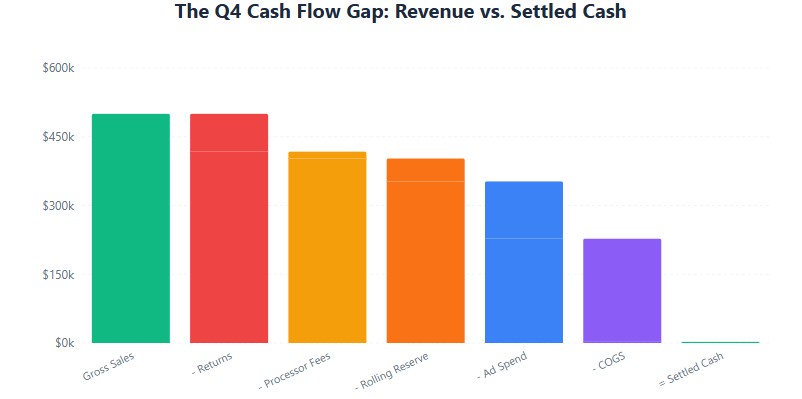

Start with your historical Q4 revenue by category. Apply a conservative seasonal lift (e.g., 2.5x to 3x for November). Then, immediately subtract your return reserve.

Formula: Gross Sales – (Gross Sales × 16.5% Return Rate) = Net Sales

Pro Tip: Do not forecast 100% of Net Sales as cash-in-hand. Assume a 5-to-7-day settlement lag from your payment gateway, and factor in a 10% buffer for potential processor holds.

Step 2: Map Inventory Outlays to Vendor Terms

Under IRS rules (IRC §263A), inventory is a capitalized asset, not an immediate expense. Buying $200,000 in stock in September drains your cash, even if it doesn’t hit your P&L as COGS until it sells.

Map your purchase orders against your vendor terms. If you have Net-30 terms, an order placed on August 15 is due September 14. Ensure your cash balance on September 14 can cover it without tapping a high-interest credit line.

Step 3: Model Ad Spend Against ROAS Thresholds

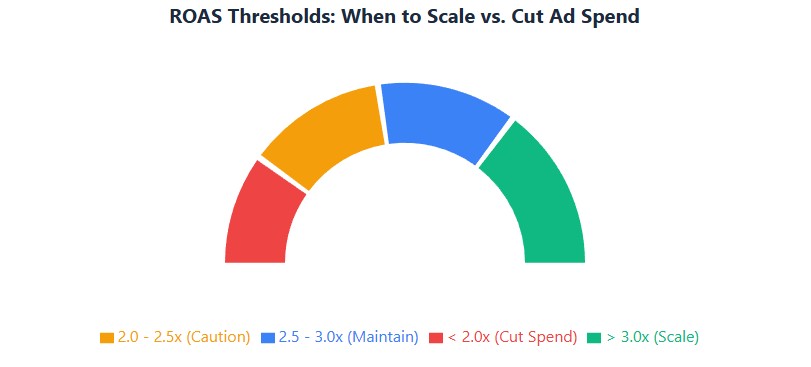

Ad spend is your most flexible, yet most dangerous, cash outflow. Base your Q4 budget on historical Return on Ad Spend (ROAS).

- Beauty/Apparel: Target 3.0x+ ROAS

- Electronics/Home Goods: Target 2.5x+ ROAS

Rule of thumb: If your blended ROAS drops below 2.0x for two consecutive weeks in November, cap the spend immediately. Do not “hope” it turns around in December. Protect the cash.

Step 4: Calculate Your True Cash Runway

Use this weekly formula to ensure you never dip below your minimum operating balance:

Ending Cash = Starting Cash + Settled Revenue - (COGS + Ad Spend + Payroll + Processor Holds + Tax Reserves)

If your “Ending Cash” projection drops below 30 days of fixed operating expenses in any week, you have a funding gap that must be addressed now.

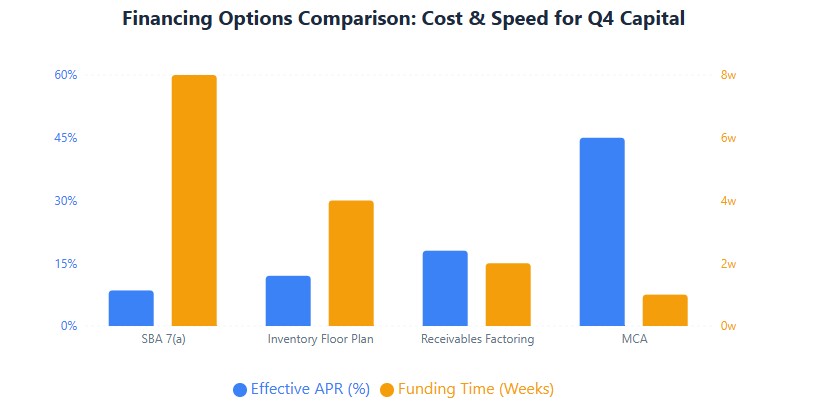

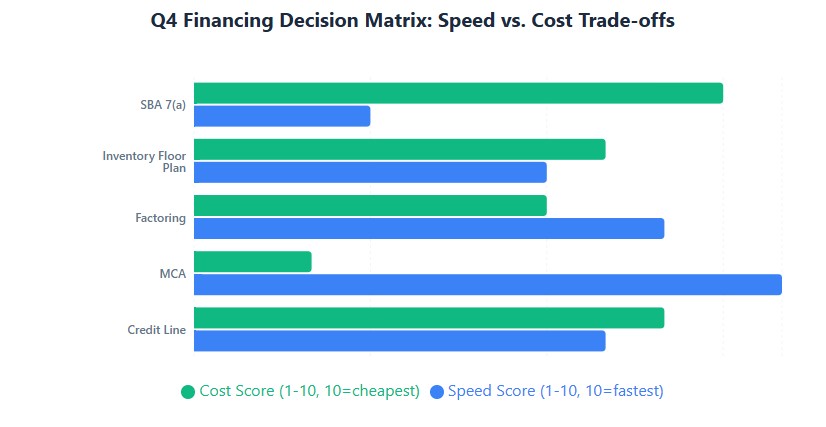

Financing the Q4 Gap: Choosing the Right Tool

If your forecast shows a cash shortfall, you need working capital. But not all capital is created equal. Choosing the wrong instrument can destroy your Q4 margins.

| Financing Option | Best For | Cost & Terms | The Catch |

|---|---|---|---|

| SBA 7(a) Working Capital | Brands with 2+ years history, 680+ credit, and strong cash flow. | Prime + 2-3%. 6–10 week funding time. | Too slow for last-minute October emergencies. Requires extensive documentation. |

| Inventory Floor Planning | High-ticket items (electronics, furniture) with audited inventory. | Interest only on drawn funds. Pay as units sell. | Requires strict UCC-1 filings and often a personal guarantee. |

| Receivables Factoring | B2B e-commerce or brands with wholesale accounts waiting on Net-60 payments. | 1.5% – 3% fee per 30 days. | Recourse factoring leaves you liable if the buyer doesn’t pay. |

| Merchant Cash Advance (MCA) | Desperate, last-resort funding for brands with high card volume but poor credit. | 10% – 15% effective APR. Daily ACH pulls. | Daily withdrawals will strangle your cash flow during the exact weeks you need it most. |

The Verdict: If you have the financials, secure an SBA line of credit or term loan by September 30. If you are asset-heavy, look into inventory financing. Avoid MCAs unless your brand’s survival is literally on the line.

Compliance & Audit Triggers: Don’t Let the IRS Ruin Q4

High-volume months attract scrutiny. State Departments of Revenue and the IRS use automated systems to flag discrepancies. Protect your brand by watching these specific triggers:

1. The 1099-K vs. Sales Tax Mismatch

With the 1099-K reporting threshold at $600, the IRS sees almost all your platform revenue. States like California, New York, and Illinois actively cross-reference your 1099-K gross volume against your filed sales tax returns. If your 1099-K shows $500,000 but you only reported $300,000 in taxable sales, expect a CP2000 notice or a state audit. Solution: Reconcile your platform payouts with your sales tax filings monthly, not annually.

2. Temporary Seasonal Staffing Rules

Hiring holiday help? In California, you must register new employees with the EDD within 20 days, and State Disability Insurance (SDI) withholding begins on day one. Failure to do so triggers immediate penalties.

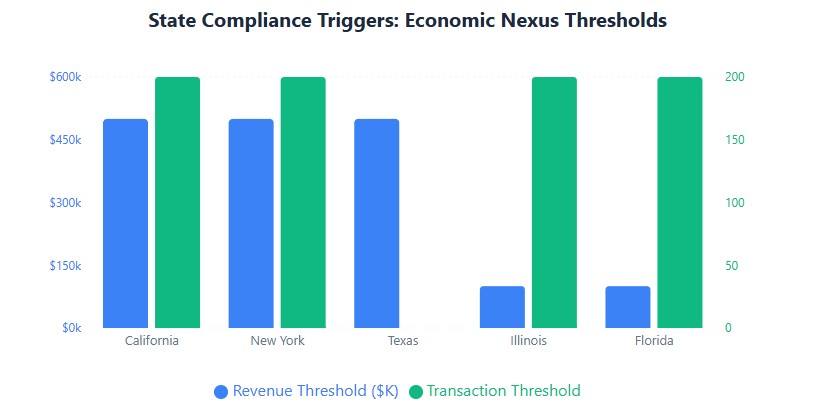

3. Economic Nexus Triggers

In Texas, exceeding $500,000 in affiliate-driven or marketplace sales creates an economic nexus, requiring you to register for a sales tax permit and start collecting/remitting tax. Do not wait until January to figure this out.

4. Return Reserve Accounting (ASC 606)

If you seek outside investment or an audit, you must record a “refund liability” for expected returns at the time of sale, alongside a “return asset” for the inventory you expect to get back. Failing to do this materially misstates your gross margin.

The 90-Day Q4 Cash Flow Countdown Checklist

Print this out. Execution is everything.

September (90 Days Out)

- [ ] Finalize Inventory Orders: Place all Q4 purchase orders to align with vendor Net-30/Net-60 terms and avoid Q3 freight rate hikes.

- [ ] Secure Financing: Submit applications for SBA 7(a) or inventory financing. Do not wait until October.

- [ ] Q3 Tax Check: Make your Q3 estimated tax payment (Form 1040-ES) by September 15 to maintain IRS safe harbor protection.

October (60 Days Out)

- [ ] Stress-Test Your Forecast: Run a “downside scenario” (25% returns, 1.8x ROAS). If cash drops below 30 days of runway, cut planned ad spend or secure a backup credit line.

- [ ] Audit Processor Terms: Log into Stripe/Shopify/PayPal. Confirm your current reserve terms. If your chargeback rate is under 0.5%, proactively email them to request a reserve reduction for Q4.

- [ ] Hire Seasonal Staff: Ensure all W-4s, I-9s, and state new-hire reports are filed to avoid EDD/DOR penalties.

November (30 Days Out)

- [ ] Adjust Free Shipping Thresholds: Raise your free shipping minimum by 15-20% to offset peak carrier surcharges.

- [ ] Monitor ROAS Daily: Implement a hard rule: if blended ROAS dips below target for 3 days, pause underperforming campaigns immediately.

December & January (Post-Peak)

- [ ] Reconcile 1099-K Data: By January 15, begin matching your platform 1099-Ks to your internal ledger to prepare for tax season.

- [ ] Process Returns Aggressively: Get returned inventory back into sellable condition quickly to recapture cash and minimize the refund liability drag on your balance sheet.

Frequently Asked Questions

Are return shipping costs tax-deductible?

Yes. Under IRC §162, return shipping is generally treated as an ordinary and necessary business expense (often categorized as a sales allowance or marketing expense). Do not bury it in COGS unless you directly own the carrier contract and it’s a direct cost of the sale.

What if my payment processor places a surprise reserve on my funds?

This is why the “Settled Revenue” step in the forecast is critical. If it happens, contact your account manager immediately. Provide them with tracking numbers for fulfilled orders and a low chargeback history to negotiate a partial or full release of the hold.

Can I use a Home Equity Line of Credit (HELOC) for Q4 inventory?

Proceed with extreme caution. Under IRS Notice 2018-02, HELOC interest is only deductible if the funds are used to “buy, build, or substantially improve” the home that secures the loan. Using it for business inventory makes the interest non-deductible, and you are putting your personal residence at risk for business volatility.

Final Thought

Q4 will test your operations, your marketing, and your financial discipline. The brands that win aren’t necessarily the ones with the highest gross sales. They are the ones that accurately forecast their cash needs, secure affordable capital in September, and protect their margins from hidden fees and returns. Build your forecast today, so you can actually enjoy the holidays you’re working so hard to fund.