Most startup loan repayment models are broken. They treat debt as a static line item, ignore the interaction with SaaS metrics like CAC payback and burn multiple, and fail to automate with real bank feeds. When your variable rate resets or a covenant gets breached, you’re scrambling in Excel instead of having automated alerts.

This guide gives you the CFO-level framework used by growth-stage startups to model debt service alongside SaaS metrics, integrate with Stripe/QuickBooks APIs, and negotiate with lenders from a position of data-driven strength.

Part 1: Advanced Debt Structures Most Founders Ignore

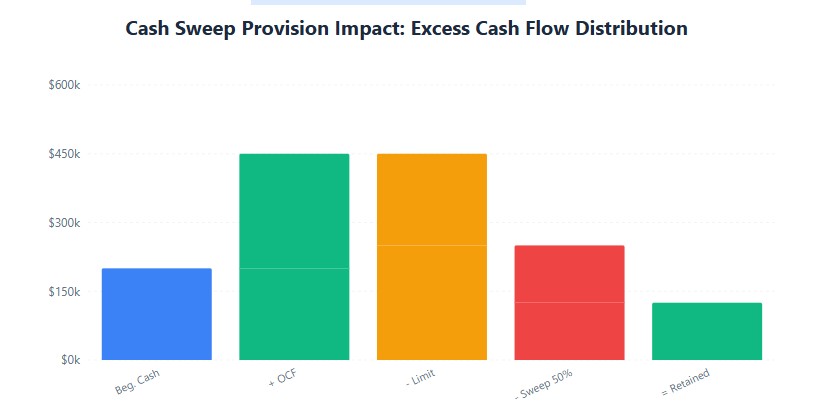

1. Cash Sweep Provisions: The Hidden Liquidity Trap

If your loan has a cash sweep clause, excess cash above a threshold gets automatically applied to principal. This sounds good (faster payoff) but destroys your cash flow flexibility.

Example: Your loan agreement says “50% of Excess Cash Flow above $200K must be applied to principal.”

| Quarter | Cash Balance | Excess Cash | Sweep Amount (50%) | Remaining Cash |

|---|---|---|---|---|

| Q1 | $450,000 | $250,000 | $125,000 | $325,000 |

| Q2 | $380,000 | $180,000 | $90,000 | $290,000 |

CFO Insight: Banks use cash sweeps to de-risk their exposure. You lose the ability to deploy that cash for growth initiatives (hiring, marketing, R&D). Always negotiate the threshold higher and the sweep percentage lower (target: 25% sweep above $500K).

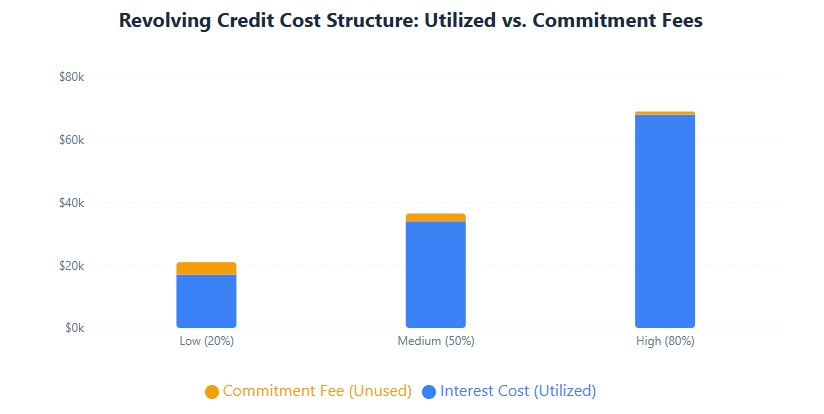

2. Revolving Credit Lines vs. Term Loans: Modeling the Difference

Term loans are predictable. Revolvers are not. You need to model peak utilization and commitment fees.

Formula for Revolver Costs:

Total Cost = (Utilized Amount × Interest Rate) + (Unused Commitment × Commitment Fee)

Example: $1M Revolver at SOFR + 3.5% with 0.5% Commitment Fee

| Scenario | Utilized | Unused | Interest Cost (8.5%) | Commitment Fee (0.5%) | Total Annual Cost |

|---|---|---|---|---|---|

| Low Utilization | $200K | $800K | $17,000 | $4,000 | $21,000 |

| High Utilization | $800K | $200K | $68,000 | $1,000 | $69,000 |

Key Insight: Commitment fees are “dead money” — you pay them whether you use the line or not. Factor this into your runway calculations.

3. Multi-Tranche Debt: Venture Debt & Mezzanine Financing

Growth-stage startups often layer debt: senior secured term loan + mezzanine debt with warrants.

Modeling Warrant Dilution:

If your mezzanine lender gets warrants for 5% of equity at a $20M valuation, that’s $1M of equity value. Over 5 years, that’s $200K/year in implicit cost.

Effective Cost Formula:

Total Cost = Cash Interest + Warrant Value / Term Years

Example: $2M Mezzanine at 12% + 5% Warrants

- Cash Interest: $240K/year

- Warrant Value: $1M / 5 years = $200K/year

- Total Cost: $440K/year = 22% effective rate

CFO Insight: Warrants are expensive. Negotiate them down or cap the valuation at which they’re priced.

Part 2: Integrating SaaS Metrics into Debt Modeling

The SaaS Debt Triangle: CAC Payback, Burn Multiple, Runway

Debt doesn’t exist in a vacuum. It interacts with your core SaaS metrics. Here’s how:

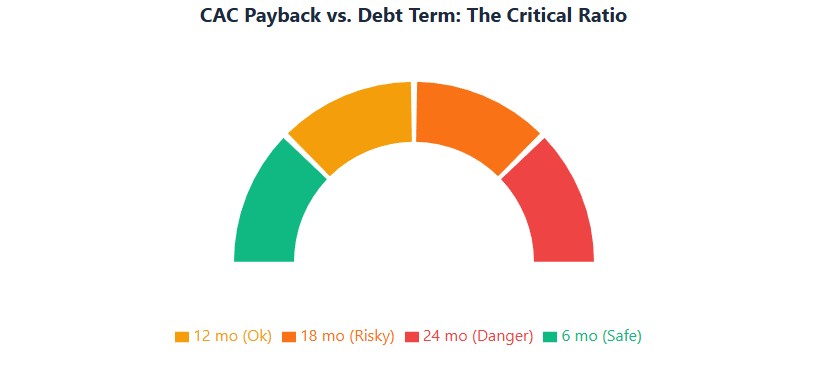

1. CAC Payback Period Impact

If you use debt to fund customer acquisition, your CAC payback period must be shorter than your debt term.

Formula:

CAC Payback = CAC / (Gross Margin % × Monthly Recurring Revenue per Customer)

Example:

- CAC: $3,000

- ARPU: $500/month

- Gross Margin: 80%

- Monthly Contribution: $400

- CAC Payback: $3,000 / $400 = 7.5 months

Decision Rule: If CAC payback is 7.5 months, you can safely use a 12-month revolver to fund acquisition. If payback is 18 months, you need longer-term debt or equity.

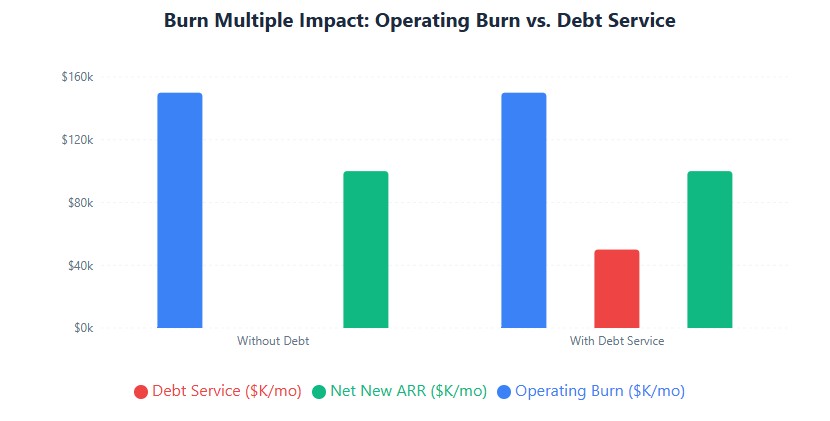

2. Burn Multiple & Debt Service

Your burn multiple (Net Burn / Net New ARR) tells you how efficiently you’re growing. Adding debt service increases your burn.

Adjusted Burn Multiple Formula:

Adjusted Burn = (Operating Burn + Debt Service) / Net New ARR

Example:

| Metric | Without Debt | With $50K/month Debt Service |

|---|---|---|

| Operating Burn | $150K/month | $150K/month |

| Debt Service | $0 | $50K/month |

| Total Burn | $150K/month | $200K/month |

| Net New ARR | $100K/month | $100K/month |

| Burn Multiple | 1.5x | 2.0x |

Red Flag: If debt service pushes your burn multiple above 2.0x, you’re in the “danger zone” for venture-backed startups.

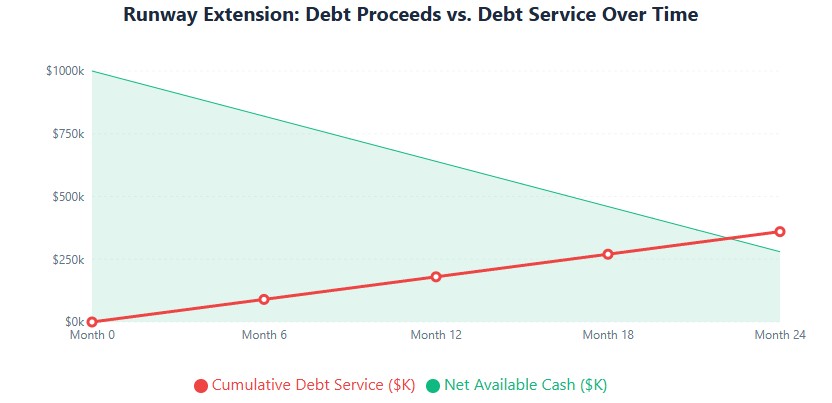

3. Runway vs. ARR Growth

Debt can extend runway, but only if used for growth, not operations.

Runway Extension Formula:

Extended Runway = (Debt Proceeds - Debt Service over Period) / Monthly Burn

Example:

- Current Runway: 12 months

- Debt Proceeds: $1M

- Monthly Debt Service: $15K

- Monthly Burn: $100K

- Extended Runway: ($1M – $180K) / $100K = 8.2 additional months

- Total Runway: 12 + 8.2 = 20.2 months

CFO Insight: If you’re using debt just to extend runway without growing ARR, you’re kicking the can. Lenders will see this in your DSCR and pull credit.

Part 3: Automation & Real-Time Monitoring (2026 Stack)

1. Bank Feed Integration: QuickBooks + Stripe + Plaid

Stop manually updating amortization schedules. Connect your systems:

Setup:

- QuickBooks Online → Connect bank feeds via Plaid

- Stripe → Enable auto-sync to QBO

- Lender Portal → Export API key for payment data

Automation Workflow:

- Daily: Bank feeds update cash balance

- Weekly: Stripe revenue syncs to QBO

- Monthly: Lender API pulls payment data → auto-updates amortization schedule

- Real-time: DSCR dashboard recalculates

2. AI-Powered Forecasting Tools

Use AI to predict covenant breaches before they happen:

| Tool | Use Case | Integration |

|---|---|---|

| Puzzle | Cash flow forecasting with ML | QuickBooks, Xero, Stripe |

| Agicap | Debt service tracking & scenario modeling | Bank feeds, Excel export |

| Finmark (by Bill.com) | Startup financial modeling with debt | QuickBooks, Stripe, Shopify |

| LivePlan | Traditional forecasting with loan modules | QuickBooks, Xero |

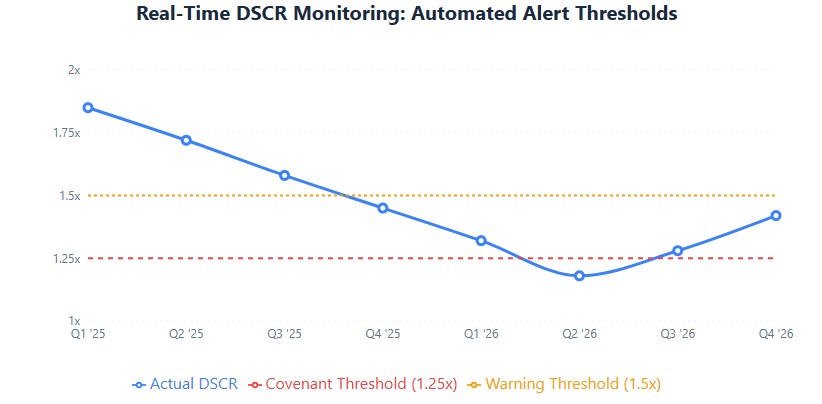

3. Real-Time DSCR Dashboard

Build a dashboard that updates automatically:

Metrics to Track:

- Current DSCR vs. Covenant Threshold

- Projected DSCR (next 3 quarters)

- Debt-to-ARR Ratio

- Months of Cash Runway

- Variable Rate Exposure (% of debt at variable rates)

Alert Triggers:

- DSCR falls below 1.5x → Email CFO

- DSCR falls below 1.25x → Email CEO + Board

- Cash runway < 6 months → Emergency board meeting

Part 4: CFO-Level Insights: How Banks Actually Calculate DSCR

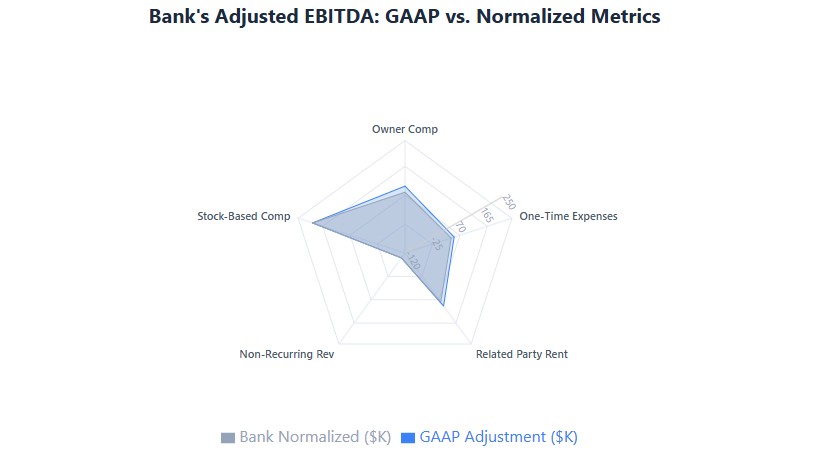

The “Adjusted EBITDA” Game

Banks don’t use your GAAP EBITDA. They use Adjusted EBITDA with add-backs and normalizations.

Common Bank Adjustments:

| Adjustment Type | Example | Bank Treatment |

|---|---|---|

| Owner Compensation | Founder pays self $250K, market rate is $150K | Add back $100K to EBITDA |

| One-Time Expenses | $50K legal fee for patent litigation | Add back to EBITDA (if documented) |

| Related Party Rent | Paying founder’s LLC $20K/month for office (market is $12K) | Add back $8K/month to EBITDA |

| Non-Recurring Revenue | $100K one-time consulting project | Subtract from EBITDA |

| Stock-Based Compensation | $200K in equity grants | Add back (non-cash expense) |

CFO Strategy: Document every add-back with third-party proof (salary surveys, market rent comps, legal invoices). Banks will disallow undocumented adjustments.

How Banks “Normalize” Your Metrics

Banks don’t trust your monthly volatility. They use trailing 12-month (TTM) averages and seasonality adjustments.

Example:

- Your Q4 revenue: $500K (holiday spike)

- Your Q1 revenue: $200K (post-holiday slump)

- Bank’s view: TTM average = $300K/quarter

Implication: Don’t take on debt in Q4 thinking you can service it year-round. Banks will normalize your revenue down.

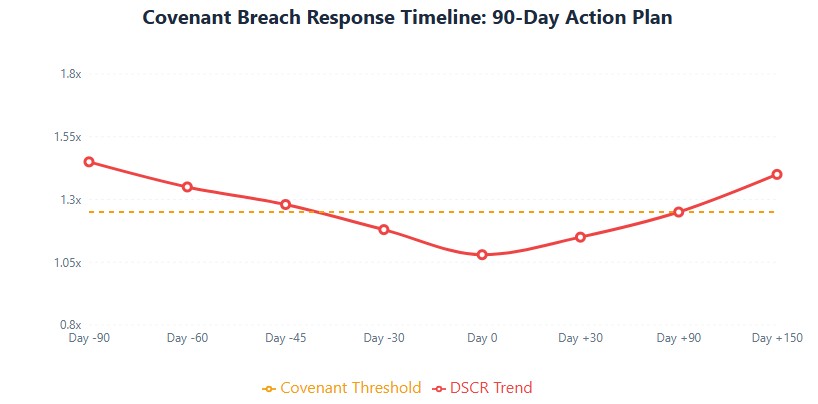

Part 5: Negotiating with Lenders During Covenant Breach

The 3-Step Breach Response Framework

Step 1: Early Detection (90 Days Before Breach)

Your DSCR dashboard shows 1.3x (covenant is 1.25x). You have 90 days.

Actions:

- Model scenarios: What if revenue drops 10%? What if rates rise 1%?

- Identify levers: Can you delay capex? Can you accelerate collections?

- Prepare narrative: “We’re investing in growth, here’s the ROI timeline”

Step 2: Proactive Outreach (60 Days Before Breach)

Contact your relationship manager before you breach.

Script:

“We’re projecting a temporary DSCR dip to 1.15x in Q3 due to [specific reason: seasonal slowdown, strategic investment]. We have a plan to recover to 1.3x by Q4 through [specific actions: cost reduction, revenue acceleration]. Can we discuss a temporary covenant waiver or amendment?”

Why This Works: Lenders prefer proactive borrowers. Surprises trigger default clauses.

Step 3: Negotiation Levers

When you’re in breach (or about to be), you have leverage points:

| Lever | How to Use It | Lender Response |

|---|---|---|

| Prepayment | “We can prepay $100K if you grant a 6-month waiver” | Lender gets cash now, you get breathing room |

| Additional Collateral | “We’ll pledge our AR as additional security” | Reduces lender risk, may get covenant relief |

| Personal Guarantee | “Founder will provide limited PG for 12 months” | Shows commitment, lender may defer action |

| Equity Injection | “We’re raising $500K equity, will use $200K to pay down debt” | Improves DSCR, lender may restructure |

Real Negotiation Example

Situation: SaaS startup, DSCR fell to 1.08x (covenant 1.25x) due to customer churn.

Negotiation:

- CEO contacted lender 45 days before reporting date

- Provided 13-week cash flow forecast showing recovery to 1.3x

- Offered to prepay $50K from recent equity raise

- Requested: 6-month covenant waiver + quarterly reporting

Outcome: Lender granted waiver, increased reporting frequency, no default. Startup recovered DSCR to 1.4x in 5 months.

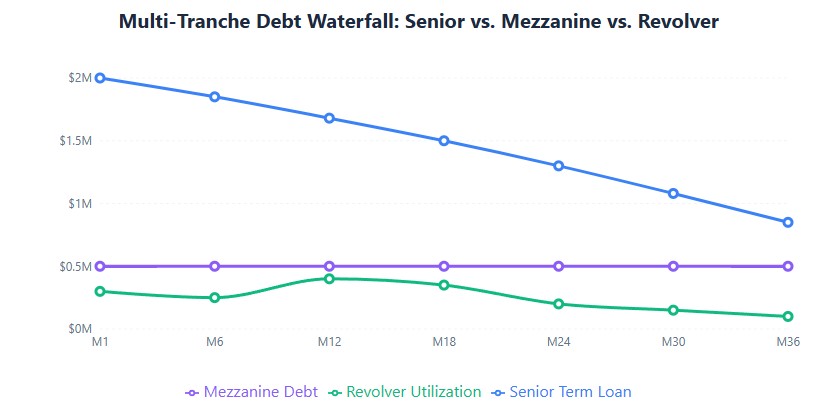

Part 6: Advanced Modeling Templates & Formulas

1. Multi-Tranche Debt Waterfall

When you have senior debt + mezzanine + revolver, model the payment waterfall:

| Tranche | Amount | Rate | Priority | Monthly Payment |

|---|---|---|---|---|

| Senior Term Loan | $2M | 7.5% | 1st | $23,840 |

| Mezzanine Debt | $500K | 12% | 2nd | $5,000 |

| Revolver (utilized) | $300K | SOFR+3.5% | 1st (same as senior) | $2,125 |

| Total | $2.8M | Blended: 8.9% | — | $30,965 |

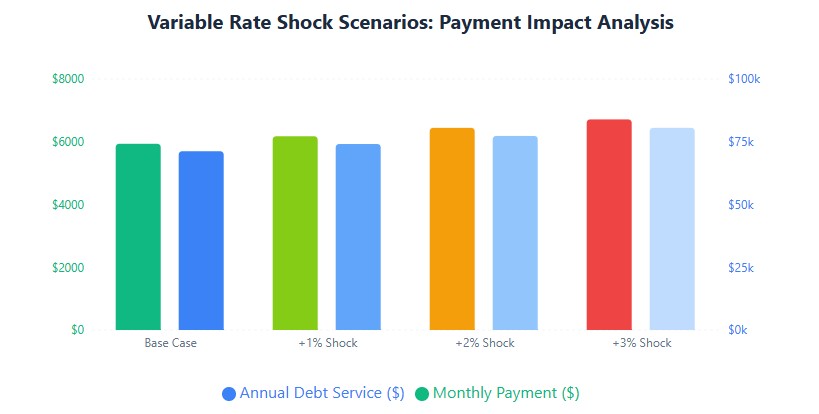

2. Dynamic Amortization with Rate Resets

For variable-rate loans, build a toggle for rate scenarios:

Excel Formula:

=PMT((SOFR_Cell + Spread_Cell)/12, Remaining_Term, -Remaining_Balance)

Scenario Table:

| Scenario | SOFR | Spread | Effective Rate | Monthly Payment | Annual Impact |

|---|---|---|---|---|---|

| Base Case | 4.5% | 3.5% | 8.0% | $5,935 | $71,220 |

| Rate Shock +2% | 6.5% | 3.5% | 10.0% | $6,443 | $77,316 |

| Rate Shock +3% | 7.5% | 3.5% | 11.0% | $6,712 | $80,544 |

3. Covenant Compliance Calculator

Build a dashboard that auto-calculates:

Inputs:

- TTM EBITDA (from QBO)

- Capex (from cash flow statement)

- Taxes paid (from tax returns)

- Total debt service (from amortization schedule)

Formula:

DSCR = (TTM EBITDA - Capex - Taxes) / Total Debt Service

Alert Logic:

- IF DSCR < 1.25x → "WARNING: Covenant breach risk"

- IF DSCR < 1.15x → "CRITICAL: Immediate action required"

- IF DSCR > 1.5x → “HEALTHY: Consider refinancing or prepayment”

Part 7: The 2026 Tech Stack for Loan Modeling

Essential Tools

| Category | Tool | Cost | Key Feature |

|---|---|---|---|

| Accounting | QuickBooks Online Advanced | $180/month | Custom reporting, API access |

| Bank Feeds | Plaid | $0.60/connection | Real-time bank data sync |

| Forecasting | Puzzle | $299/month | ML-powered cash flow predictions |

| Debt Tracking | Agicap | $199/month | Automated DSCR calculation |

| Scenario Modeling | Finmark | $149/month | SaaS metrics + debt integration |

Integration Workflow

Step-by-Step Setup:

- Connect QuickBooks to Plaid: Enable real-time bank feeds

- Link Stripe to QBO: Auto-sync revenue data

- Export lender API credentials: Pull payment data automatically

- Set up Puzzle/Agicap: Connect to QBO for forecasting

- Build DSCR dashboard: Pull data from all sources

- Configure alerts: Email/SMS when DSCR < 1.5x

Time to Set Up: 4-6 hours

Ongoing Maintenance: 30 minutes/month

Part 8: Common Mistakes & How to Avoid Them

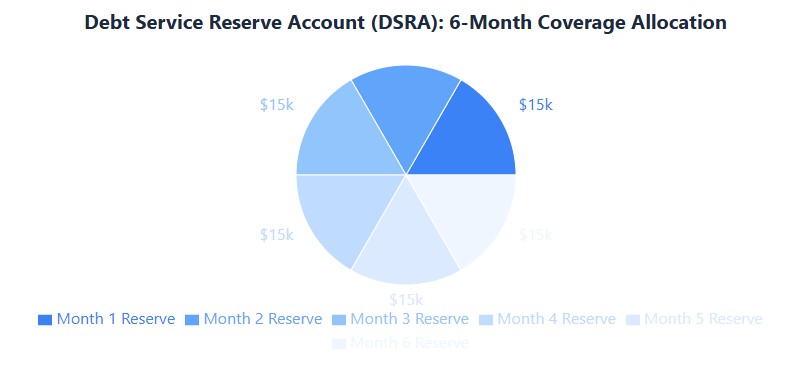

Mistake 1: Ignoring the “Debt Service Reserve”

Problem: You model debt service but don’t set aside cash for it.

Solution: Maintain a Debt Service Reserve Account (DSRA) with 3-6 months of payments.

Example:

- Monthly debt service: $15K

- DSRA target: $15K × 6 = $90K

- Keep this in a separate, non-operating account

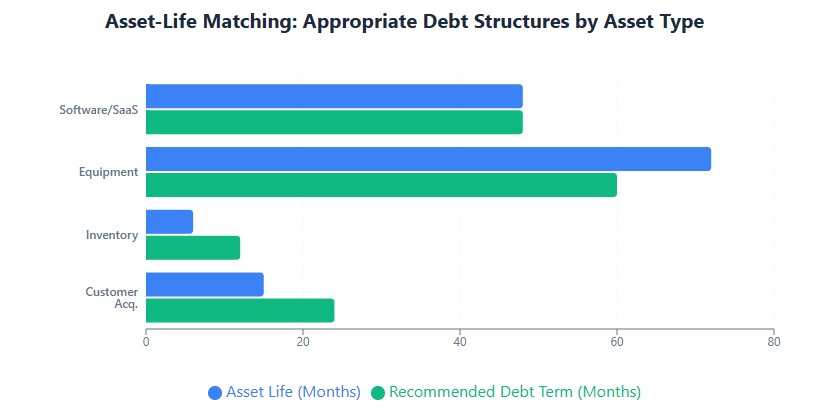

Mistake 2: Using Short-Term Debt for Long-Term Assets

Problem: You use a 12-month revolver to fund equipment that lasts 5 years.

Solution: Match asset life to debt term.

| Asset Type | Useful Life | Appropriate Debt |

|---|---|---|

| Software/SaaS | 3-5 years | 3-5 year term loan |

| Equipment | 5-7 years | 5-7 year equipment loan |

| Inventory | 3-6 months | Revolver or 12-month term |

| Customer Acquisition | 12-18 months (CAC payback) | 18-24 month term loan |

Mistake 3: Not Modeling Prepayment Scenarios

Problem: You get a cash windfall but don’t know if prepaying debt makes sense.

Solution: Build a prepayment calculator.

Formula:

Prepayment Benefit = (Remaining Interest - Prepayment Penalty) / Prepayment Amount

Decision Rule:

- If benefit > your cost of capital → Prepay

- If benefit < cost of capital → Invest elsewhere

Next Steps: Build Your Advanced Model Today

- Audit your current debt: Pull all promissory notes, list tranches, rates, covenants

- Build the multi-tranche waterfall: Model senior, mezzanine, revolver separately

- Integrate SaaS metrics: Calculate CAC payback, burn multiple, runway with debt service

- Set up automation: Connect QuickBooks, Plaid, Stripe for real-time data

- Build DSCR dashboard: Auto-calculate with alerts at 1.5x and 1.25x

- Stress-test: Model +2% and +3% rate shocks, 20% revenue decline

- Prepare negotiation playbook: Document your levers (prepayment, collateral, PG) before you need them

Debt is a tool, not a trap. But only if you model it with the sophistication it demands. Build this framework, and you’ll negotiate with lenders from strength, not desperation.