If you freelance in the US, you already know the joke: “Net-30” actually means “Net-60, if you’re lucky.”

Forecasting cash inflows when your clients pay irregularly isn’t just about budgeting—it’s about survival. The IRS doesn’t care that your biggest client is 40 days late on a $15,000 invoice. Your quarterly estimated taxes are still due on the 15th. When cash inflows are lumpy but outflows (rent, software, taxes) are fixed, a single delayed payment can trigger penalties or force you into high-interest debt.

Most advice on this topic tells you to “just build a 6-month emergency fund” or “switch to accrual accounting.” That’s useless for a solo freelancer. What you actually need is a systematic way to predict when the money will actually hit your bank account, and how to align that reality with your tax obligations.

Here is the exact, step-by-step framework to forecast irregular cash inflows, built for US freelancers operating on a cash basis.

The Core Problem: Invoice Date vs. Cash-in-Bank Date

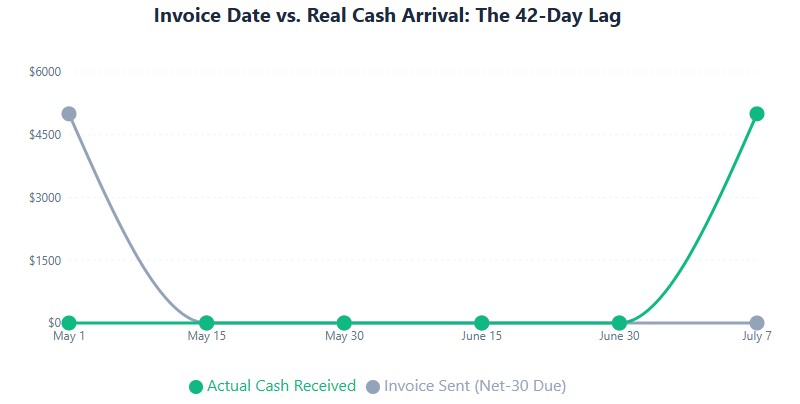

The biggest mistake freelancers make when building a cash flow forecast is using the invoice due date as the expected payment date.

If you send an invoice on May 1st with Net-30 terms, you might put $5,000 in your “June Inflows” column. But if your client’s accounts payable department only runs checks on the 15th and 30th of the month, and they always take an extra week to process, that cash doesn’t arrive until July 7th.

Your forecast just lied to you. You planned to pay your quarterly taxes in June with that $5,000, but the money isn’t there. Now you’re dipping into your reserve or paying IRS penalties.

To fix this, we have to stop forecasting based on when we bill, and start forecasting based on when we get paid.

Step 1: Calculate Your “Real” DSO (Days Sales Outstanding)

DSO measures the average number of days it takes a client to pay you. But you don’t want the theoretical DSO (30 days); you want the Real DSO.

Pull your payment history for the last 6 to 12 months. For every invoice, calculate:

Payment Date - Invoice Date = Actual Days to Pay

Do this for each major client. You will quickly see patterns:

- Client A (Corporate): Invoices are consistently paid in 42 days.

- Client B (Agency): Invoices are consistently paid in 18 days.

- Client C (Direct Small Business): Invoices are paid in 65 days, or they require a follow-up email.

Once you know the Real DSO for each client, you shift your forecast. If you invoice Client A on May 15th, you don’t put the cash in June. You put it in the week of June 26th (42 days later).

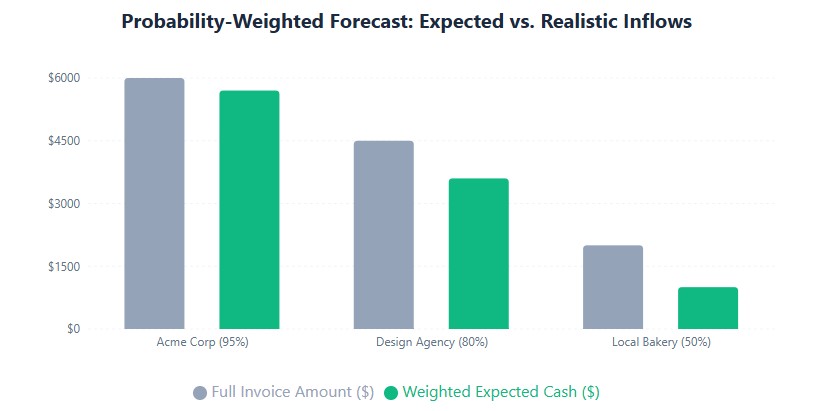

Step 2: Build a Probability-Weighted Cash Forecast

Even with Real DSO, clients sometimes ghost you or go bankrupt. A static forecast assumes 100% collection. A professional forecast applies probability weights based on the client’s payment history and your relationship.

Assign a collection probability to each outstanding invoice:

- 95% Probability: Long-term retainer client, auto-pay enabled, flawless history.

- 80% Probability: Good client, pays consistently but occasionally takes an extra week.

- 50% Probability: New client, no payment history yet, or a client who frequently negotiates invoices down.

- 0% Probability: Client is in bankruptcy or has explicitly refused to pay.

Multiply the invoice amount by the probability percentage. This gives you your Weighted Expected Cash Inflow. It keeps your forecast conservative and realistic.

Example: Probability-Weighted Pipeline

| Client | Invoice Amount | Invoice Date | Real DSO | Expected Cash Date | Probability | Weighted Inflow |

|---|---|---|---|---|---|---|

| Acme Corp (Retainer) | $6,000 | May 1 | 42 days | June 12 | 95% | $5,700 |

| Design Agency | $4,500 | May 10 | 18 days | May 28 | 80% | $3,600 |

| Local Bakery (New) | $2,000 | May 15 | 30 days (est.) | June 14 | 50% | $1,000 |

| TOTAL EXPECTED CASH FOR JUNE | $10,300 | |||||

Notice the difference? If you just added up the invoices, you’d expect $12,500. But by weighting for reality, your forecast tells you to plan for $10,300. That $2,200 difference is the buffer that keeps you from overspending.

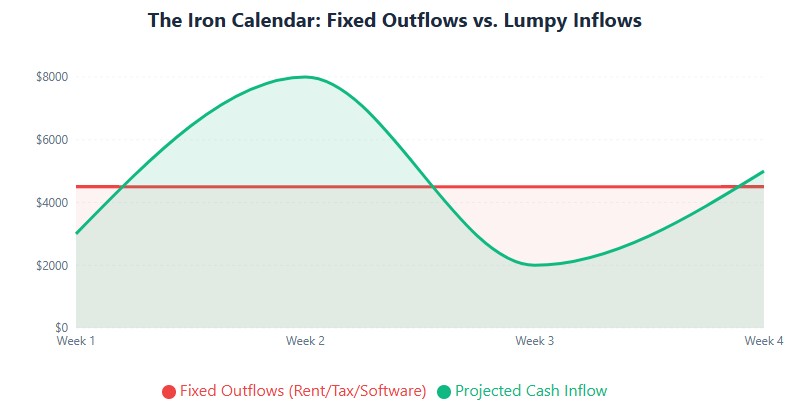

Step 3: Align Inflows with the “Iron Calendar”

Your cash inflows are flexible; your tax and fixed cost deadlines are not. Once you have your weighted inflows mapped by week, overlay your “Iron Calendar”:

- Quarterly Estimated Taxes: April 15, June 15, September 15, January 15.

- Fixed SaaS/Software: Usually hits on the 1st or 15th of the month.

- Health Insurance: Due on the 1st.

- Retirement Contributions: SEP-IRA or Solo 401(k) deadlines.

If your weighted cash inflow for the first two weeks of June is only $3,000, but your Q2 estimated tax payment is $4,500, you have a visible cash shortfall before it happens. You can now take action: delay a non-essential software upgrade, ask a client for an upfront deposit, or draw from your reserve.

The Freelancer’s Secret Weapon: Annualized Income Installments

Here is a piece of tax strategy that almost no freelance blogs talk about, but it is a lifesaver for irregular income.

The IRS generally expects you to pay your estimated taxes evenly across four quarters (25% each). But what if you make $0 in Q1, and $120,000 in Q4 because a massive project finally paid out?

If you pay equal quarterly installments, you’ll massively overpay in Q1 and Q2, and owe a fortune in Q4. Worse, if you try to pay nothing in Q1 because you have no cash, the IRS will hit you with an underpayment penalty for Q1 and Q2.

The Solution: Form 2210, Schedule AI (Annualized Income Installment Method).

This IRS form allows you to annualize your income quarter-by-quarter. It tells the IRS: “I didn’t make any money in Q1, so my required estimated payment for Q1 should be $0.”

If your income is highly seasonal or project-based (e.g., you only get paid when a book publishes, or you work on 6-month contract cycles), using Schedule AI legally eliminates underpayment penalties during your slow months. You just need to file Form 2210 with your tax return to prove it. Note: You must actually calculate and pay the correct amount for the quarter you do make the money.

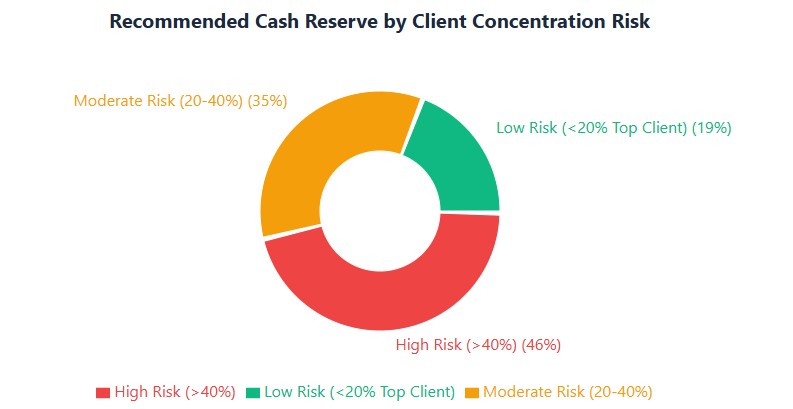

How to Size Your Cash Reserve (Based on Client Concentration)

Everyone says “save 3 to 6 months of expenses.” But that’s a generic rule of thumb. Your actual reserve size should be dictated by your client concentration risk.

Calculate what percentage of your annual revenue comes from your top client, and your top three clients.

| Top Client Revenue Share | Recommended Cash Reserve | Why? |

|---|---|---|

| Under 20% | 2 – 3 months of fixed expenses | Low concentration risk. If one leaves, it’s a bump, not a cliff. |

| 20% – 40% | 4 – 5 months of fixed expenses | Moderate risk. Losing them requires a 2-month scramble to replace revenue. |

| Over 40% | 6+ months of fixed expenses | High risk. You are essentially a captive employee. If they delay payment by 60 days, you will default on your own bills without a massive buffer. |

Keep this reserve in a separate, high-yield business savings account. Do not touch it for “opportunities” or equipment upgrades. It is strictly for cash flow timing gaps and client loss.

Handling Retainers and Upfront Deposits

Retainers are great for cash flow, but they create a forecasting and tax illusion.

If a client pays you $12,000 upfront in January for a 6-month project, your bank account looks amazing. But you cannot spend that $12,000 in January. You have to deliver the work over 6 months.

For Cash Flow Forecasting: Record the full $12,000 as a cash inflow in January. But create a separate “Locked Reserve” category in your budget. Only allow yourself to draw down $2,000 per month for operating expenses. This prevents you from blowing the cash in Month 1 and starving in Month 4.

For Taxes: If you are a cash-basis taxpayer (which 99% of solo freelancers are), that entire $12,000 is taxable income in the year you received it, regardless of when you do the work. Do not make the mistake of thinking you can defer it to next year just because the work crosses December 31st. Set aside your estimated tax percentage from that deposit immediately.

FAQ: Real-World Freelance Cash Scenarios

What if a client completely ghosts and never pays?

If you are on the cash basis (like most freelancers), you never recorded the income in the first place, so there is no tax deduction to take. You just eat the loss. This is exactly why we use probability weighting in our forecast—to mentally write off slow payers before they happen.

Should I charge late fees to improve cash flow?

Yes, but understand the psychology. A late fee doesn’t actually speed up payment from a massive corporation with a rigid AP department; it just creates a dispute that delays payment further. Late fees work brilliantly on small business clients and direct consumers. If you do charge them, remember they are taxable income.

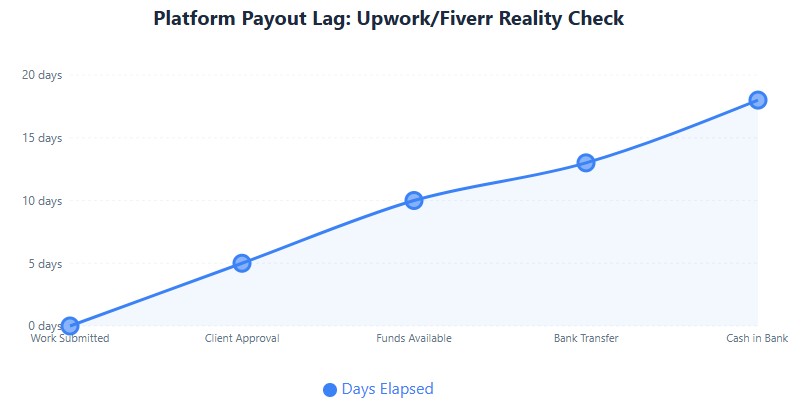

How do I handle payments from platforms like Upwork or Fiverr?

Platform payouts have their own lag. Upwork might release the funds to your “available” balance 5 days after the client approves the work, and then another 3-5 days to transfer to your US bank. Add a hardcoded 10-day lag to all platform invoices in your forecast. Never forecast platform cash based on the day you submit the work.

Can I use a business credit card to bridge cash flow gaps?

Yes, but only as a tactical bridge, not a structural crutch. If you know a $10,000 invoice is arriving in 14 days (based on your Real DSO), putting $3,000 of software and contractor costs on a 0% intro APR card is smart. If you are using a 24% APR card to pay rent because your forecast was wrong, you have a pricing or client problem, not a cash flow problem.

Next Steps: Build Your Forecast Today

- Export your data: Pull your last 6 months of invoices and payments from your accounting software (QuickBooks, Wave, HoneyBook) or a simple spreadsheet.

- Calculate Real DSO: Find the actual average days it takes your top 5 clients to pay you.

- Build the 90-day view: Create a spreadsheet with columns for the next 12 weeks. Map your outstanding invoices into the week they will actually arrive, applying probability weights.

- Overlay the Iron Calendar: Mark your next estimated tax payment and fixed software renewals. Identify any weeks where projected cash drops below your minimum operating balance.

- Adjust: If you see a shortfall, pause discretionary spending, request a 50% upfront deposit on your next new project, or draw from your reserve.

Forecasting irregular income isn’t about predicting the future perfectly. It’s about removing the surprises. When you know exactly when the cash is coming—and more importantly, when it isn’t—you stop reacting to emergencies and start running your freelance business like a real company.