Why Cash Flow Forecasting Actually Matters for Solopreneurs

Profit isn’t cash. You can be “profitable” on paper and still miss a tax payment because client money hasn’t hit your account yet. For solopreneurs—who often deal with irregular income but fixed monthly outflows—this gap is dangerous.

Three realities in 2026:

- Payments are slower: Many clients now pay Net 30 or Net 45. If you invoice on the 1st but get paid on the 30th, your forecast must reflect that delay.

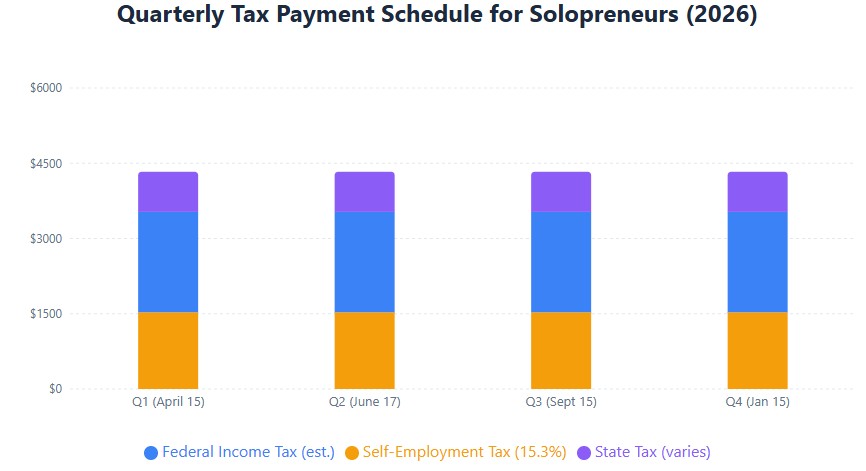

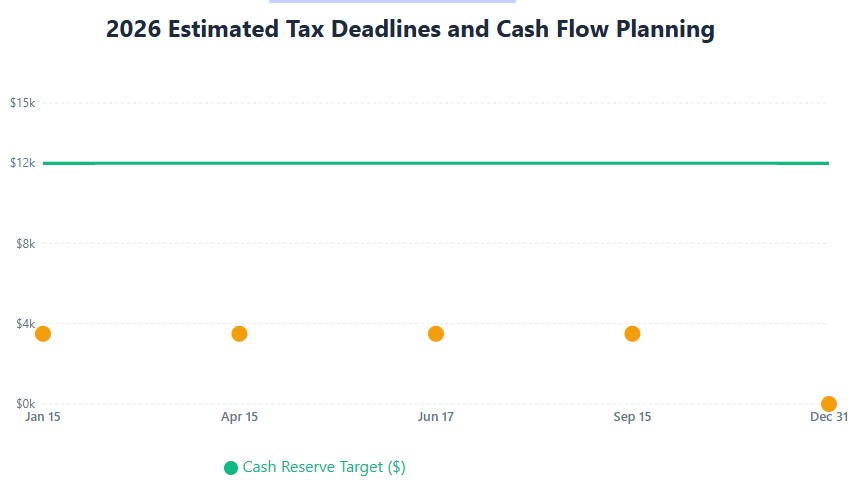

- Taxes don’t wait: Quarterly estimated tax deadlines (April 15, June 17, Sept 15, Jan 15) are fixed. Miss one, and you face penalties under IRC Section 6654—even if your client just paid late.

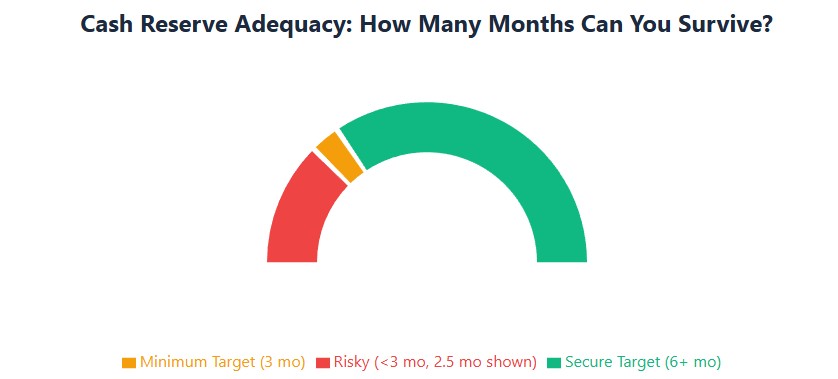

- Reserves are non-negotiable: The SBA recommends 3–6 months of operating expenses in cash. For a solopreneur spending $4,000/month, that’s $12,000–$24,000. Your forecast tells you if you’re on track.

Your Cash Flow Forecast Template (Ready to Use)

Copy this template structure. Fill in your numbers. Update monthly.

| Category | January | February | March | April | May | June | July | August | September | October | November | December |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

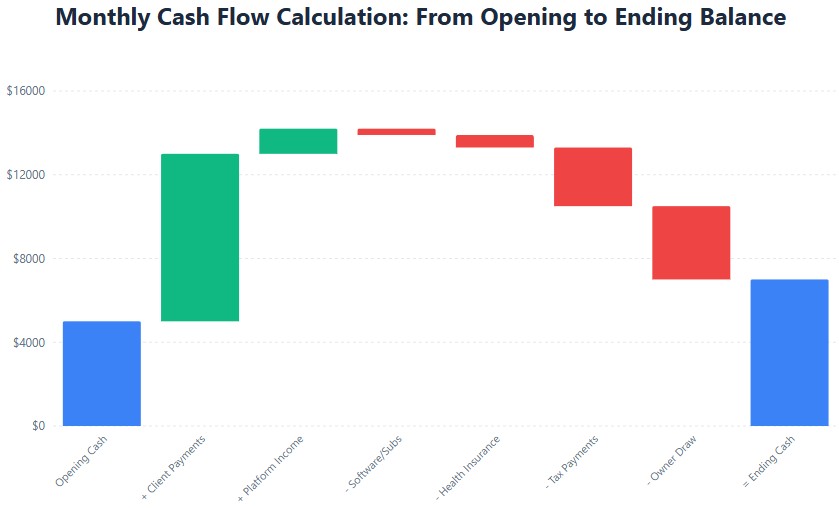

| OPENING CASH BALANCE | $5,000 | |||||||||||

| CASH INFLOWS | ||||||||||||

| Client Payments (Net 30) | $0 | $8,000 | $8,000 | $8,000 | $8,000 | $8,000 | $8,000 | $8,000 | $8,000 | $8,000 | $8,000 | $8,000 |

| Platform Income (Stripe/PayPal) | $1,200 | $1,200 | $1,200 | $1,200 | $1,200 | $1,200 | $1,200 | $1,200 | $1,200 | $1,200 | $1,200 | $1,200 |

| Other Income (grants, refunds) | $0 | $0 | $500 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| TOTAL CASH INFLOWS | $1,200 | $9,200 | $9,700 | $9,200 | $9,200 | $9,200 | $9,200 | $9,200 | $9,200 | $9,200 | $9,200 | $9,200 |

| CASH OUTFLOWS | ||||||||||||

| Fixed Costs: | ||||||||||||

| Software & Subscriptions | $300 | $300 | $300 | $300 | $300 | $300 | $300 | $300 | $300 | $300 | $300 | $300 |

| Health Insurance | $600 | $600 | $600 | $600 | $600 | $600 | $600 | $600 | $600 | $600 | $600 | $600 |

| State Fees (monthly avg) | $67 | $67 | $67 | $67 | $67 | $67 | $67 | $67 | $67 | $67 | $67 | $67 |

| Variable Costs: | ||||||||||||

| Supplies & Equipment | $200 | $150 | $200 | $100 | $200 | $150 | $200 | $100 | $200 | $150 | $200 | $300 |

| Marketing & Advertising | $150 | $150 | $150 | $150 | $150 | $150 | $150 | $150 | $150 | $150 | $150 | $200 |

| Contractor Help | $0 | $500 | $0 | $0 | $500 | $0 | $0 | $500 | $0 | $0 | $500 | $0 |

| Tax Payments: | ||||||||||||

| Quarterly Estimated Taxes | $0 | $0 | $0 | $3,500 | $0 | $0 | $0 | $0 | $3,500 | $0 | $0 | $3,500 |

| Owner Draw: | ||||||||||||

| Monthly Take-Home Pay | $3,500 | $3,500 | $3,500 | $3,500 | $3,500 | $3,500 | $3,500 | $3,500 | $3,500 | $3,500 | $3,500 | $3,500 |

| TOTAL CASH OUTFLOWS | $4,817 | $5,267 | $4,817 | $8,317 | $5,317 | $4,767 | $4,817 | $5,267 | $8,317 | $4,767 | $4,817 | $8,267 |

| ENDING CASH BALANCE | $1,383 | $5,316 | $10,199 | $11,082 | $14,965 | $19,398 | $23,781 | $27,714 | $28,597 | $33,030 | $37,413 | $38,346 |

| 3-Month Reserve Target | $12,000 | $12,000 | $12,000 | $12,000 | $12,000 | $12,000 | $12,000 | $12,000 | $12,000 | $12,000 | $12,000 | $12,000 |

| Above/Below Target | -$10,617 | -$6,684 | -$1,801 | -$918 | +$2,965 | +$7,398 | +$11,781 | +$15,714 | +$16,597 | +$21,030 | +$25,413 | +$26,346 |

How to use this template: Copy the structure into your preferred spreadsheet tool. Replace example numbers with your actual data. The Ending Cash Balance formula is: Opening Cash + Total Inflows – Total Outflows. Each month’s Opening Cash = prior month’s Ending Cash.

The Simple Forecasting Method: 6 Steps

Here’s how to build and maintain your cash flow forecast in under 20 minutes each month.

Step 1: Set Up Your Structure

Create columns for each month (Jan–Dec) and rows for:

- Opening Cash Balance (carried from prior month)

- Cash Inflows (client payments, platform payouts, reimbursements)

- Fixed Outflows (software, insurance, subscriptions)

- Variable Outflows (supplies, travel, contractor help)

- Tax Payments (quarterly estimates, self-employment tax)

- Owner Draw (your take-home pay)

- Ending Cash Balance (calculated)

Step 2: Input Inflows by Expected Collection Date

Don’t record revenue when you invoice—record it when you expect the cash to hit your account.

- If you invoice a client on Net 30 terms in January, put the payment in February’s Cash Inflows column.

- For platform income (Stripe, PayPal, Etsy), use your payout schedule (often 2–7 days after sale).

- Include irregular inflows: grants, refunds, affiliate commissions. Tag them so you can filter later.

Step 3: List Outflows—Fixed First, Then Variable

Fixed costs are predictable. Variable costs aren’t. Separate them so you can stress-test your forecast.

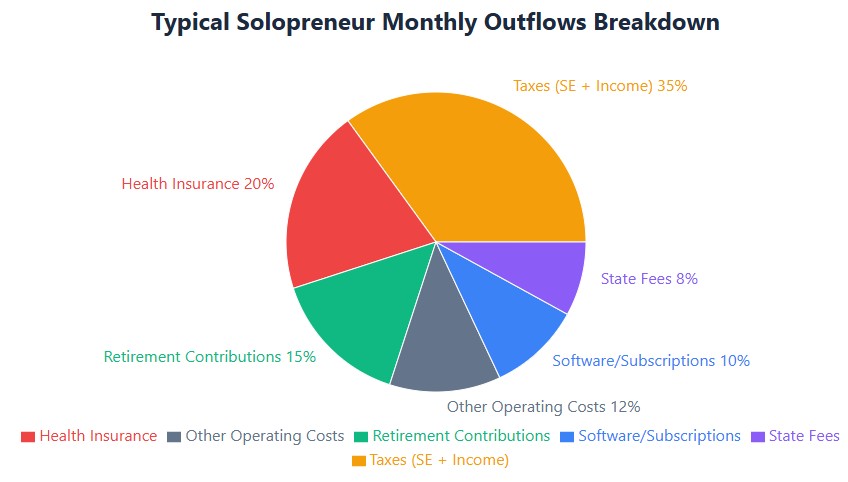

Typical fixed outflows for solopreneurs:

- Software subscriptions: $50–$300/month (accounting, project management, design tools)

- Health insurance: $300–$800/month (varies by state and plan)

- Retirement contributions: SEP-IRA or Solo 401(k) contributions (often quarterly)

- State fees: CA LLC franchise tax ($800/yr = $67/mo), DE franchise tax ($300/yr = $25/mo), etc.

Typical variable outflows:

- Supplies, equipment repairs, contractor help, travel, marketing tests

Step 4: Add Tax Payments—Don’t Guess

Solopreneurs often underestimate tax outflows. Here’s how to avoid that:

- Self-employment tax: 15.3% on net earnings (12.4% Social Security + 2.9% Medicare). Set aside this % of every payment you receive.

- Income tax: Use IRS Form 1040-ES worksheet. If your prior-year AGI exceeded $150,000, aim to pay 110% of last year’s tax to avoid underpayment penalties.

- State taxes: CA top rate: 13.3%; NY: 10.9%; TX: 0% income tax but may require sales tax collection. Factor these in.

Enter quarterly tax payments in the months they’re due: April, June, September, January.

Step 5: Build the Ending Cash Formula

In your Ending Cash column, use this formula (adjust cell references as needed):

=Opening Cash + Cash Inflows - Fixed Outflows - Variable Outflows - Tax Payments - Owner Draw

Then, set the next month’s Opening Cash to equal the prior month’s Ending Cash. This creates a rolling forecast.

Step 6: Add a Reserve Tracker and Alerts

Calculate your target cash reserve: =AVERAGE(Fixed Outflows + Variable Outflows) × 3

Then compare your Ending Cash to this target each month. If Ending Cash falls below your 3-month reserve target, that’s your early-warning signal to cut costs or accelerate collections.

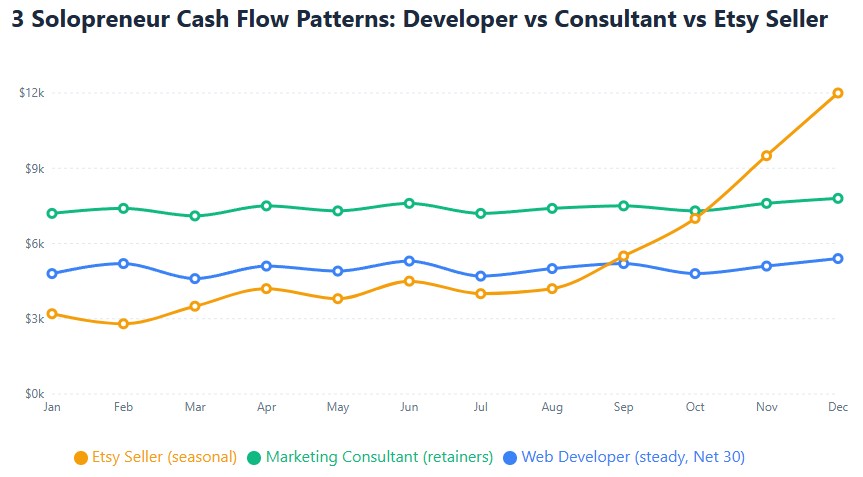

Real Scenarios: How This Works for Different Solopreneurs

One template, three different realities. Here’s how the method adapts.

Scenario 1: Freelance Web Developer (California)

- Income pattern: $8,000/month average, but clients pay Net 30

- Key outflows: $1,200 software/tools, $600 health insurance, $1,400 quarterly SEP-IRA, $2,800 estimated taxes

- Forecast insight: Without tracking payment timing, the developer overspent in January thinking a $10K invoice had cleared. The forecast flagged a $4,200 tax shortfall in Q1—90 days early.

Scenario 2: Marketing Consultant (Texas)

- Income pattern: $10,000/month retainer clients, paid on the 1st

- Key outflows: $300 software, $400 health insurance, $2,000 quarterly SEP-IRA contribution

- Forecast insight: By spreading the $6,000 quarterly retirement contribution across three months in the forecast, the consultant avoided a cash crunch and reduced taxable income proactively.

Scenario 3: Etsy Seller (Florida)

- Income pattern: $12,000 in December, drops to $3,000 by February

- Key outflows: Inventory spikes in Q4 ($5,000), shipping supplies, platform fees

- Forecast insight: The model showed a $7,000 reserve drawdown in Q1. The seller secured a small line of credit in November—before the cash pinch hit.

5 Cash Flow Mistakes Solopreneurs Make (And How to Avoid Them)

- Recording revenue when invoiced, not when paid

If you invoice on Net 30 terms, the cash isn’t yours for 30 days. Fix: Base inflows on expected collection date, not invoice date. - Forgetting quarterly tax deadlines

Miss an estimated tax payment, and you face penalties—even if you had the money. Fix: Enter tax due dates in your forecast and set calendar alerts 7 days prior. - Mixing personal and business cash

Using one bank account for everything makes forecasting impossible. Fix: Open a separate business checking account. Transfer a fixed “owner draw” to your personal account monthly. - Ignoring state filing obligations

Earning income from clients in California, New York, or Washington may trigger state tax filings—even if you live elsewhere. - Not reconciling monthly

A forecast that doesn’t match reality is useless. Fix: After each month ends, compare your forecasted Ending Cash to your actual bank balance. Adjust assumptions for the next month.

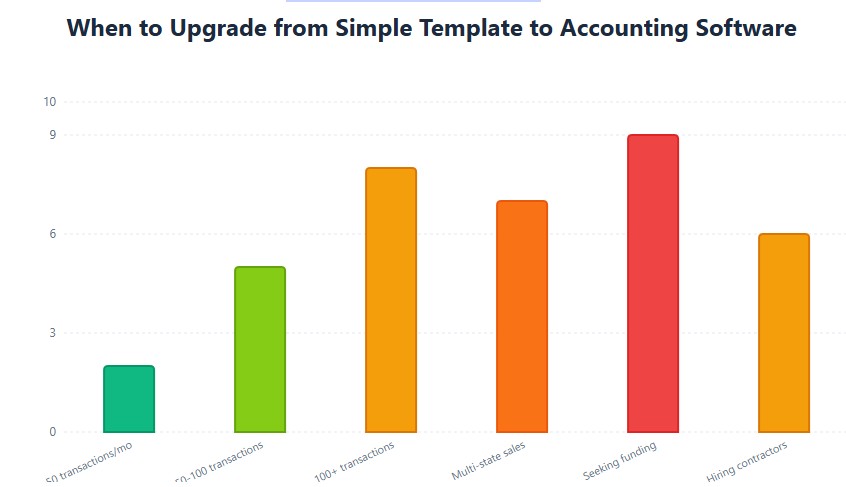

When to Upgrade: From Simple Template to Accounting Software

Simple templates work great—until they don’t. Here’s when to consider upgrading:

- You have 50+ monthly transactions: Manual entry becomes error-prone. QuickBooks Online or Xero auto-categorize and reconcile.

- You sell in multiple states: Sales tax rules get complex. TaxJar or Avalara automate calculations and filings.

- You’re applying for funding: Lenders want formal, audit-ready financials. Accounting software generates P&L, balance sheet, and cash flow statements.

- You hire contractors or employees: Gusto or Rippling automate payroll taxes, 1099 filings, and compliance.

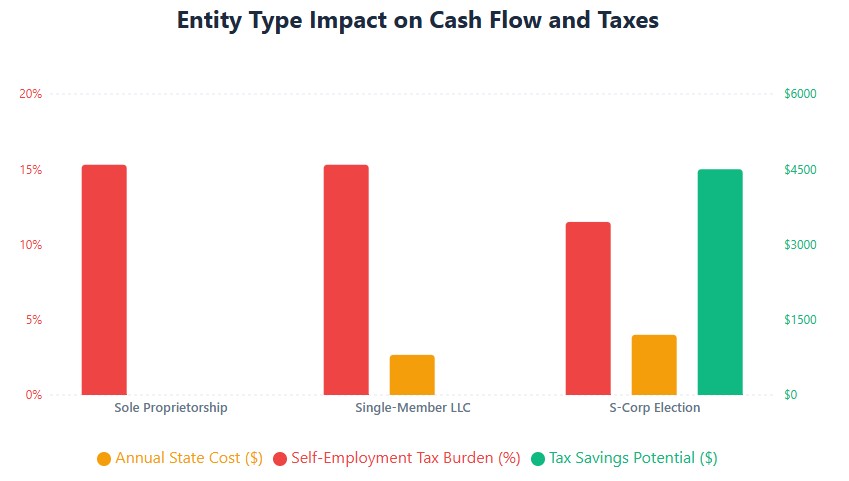

Entity Choice and Cash Flow: A Quick Guide

Your business structure affects your cash flow. Here’s how to think about it:

| Structure | Best For | Tax Impact | State Cost | Cash Flow Note |

|---|---|---|---|---|

| Sole Proprietorship | Starting out, low risk | 15.3% self-employment tax on net income | $0 in most states | Simple, but no liability protection |

| Single-Member LLC | Liability protection, still simple | Same tax as sole prop (default) | $50–$800/yr (CA: $800) | Protects personal assets; same tax treatment |

| S-Corp Election | Net profit > $60K, want tax savings | Split salary (subject to payroll tax) + distributions (not subject to SE tax) | +$175–$800/yr + payroll setup | Potential 15–30% tax savings, but adds complexity |

Source: IRS Small Business Resources; SBA Business Structure Guide

Founder FAQs (2026 Answers)

How often should I update my forecast?

Monthly, after you reconcile your bank account. Re-forecast immediately if you lose a major client, land a big project, or your income drops 20%+.

Do I need to track cash reserves for tax purposes?

No—but low reserves increase your risk of missing estimated tax payments. The IRS doesn’t care why you missed a payment. Keep 3 months of expenses liquid if possible.

Can I use this forecast for an IRS audit?

Yes—if it’s reconciled monthly, backed by bank records, and clearly separates business from personal transactions. Keep digital copies of receipts and invoices for 3+ years.

What if my income is highly irregular?

Use a conservative baseline: forecast using your lowest-earning month from the past year. Treat any extra income as a buffer, not a guarantee.

Do I need to track sales tax in my cash flow forecast?

If you sell taxable goods or services and meet a state’s economic nexus threshold (often $100K in sales or 200 transactions), yes. Sales tax collected isn’t your money—it’s held in trust for the state. Track it separately so you don’t accidentally spend it.

Next Steps: Get Started Today

- Copy the template above into your preferred spreadsheet tool. Fill in your actual numbers for the current month.

- Input your last 3 months of actuals to test the formula. Does Ending Cash match your bank balance? If not, adjust your categories.

- Forecast the next 3 months using expected payment dates, not invoice dates. Flag any month where Ending Cash falls below your 3-month reserve target.

- Schedule your next estimated tax payment via IRS Direct Pay. Set a calendar alert 7 days prior.

- Reconcile monthly: Compare forecast vs. actual. Adjust assumptions. This is how the forecast stays useful.

One Last Thing

Cash flow forecasting isn’t about perfection. It’s about awareness. When you know what’s coming—good or bad—you can make decisions instead of reacting to emergencies.

Start simple. Update monthly. Adjust as you learn. That’s how solopreneurs build resilience in 2026.