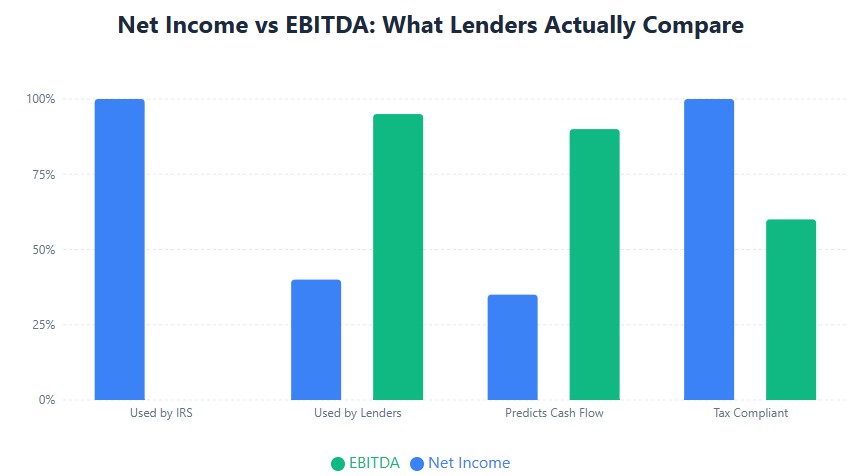

Net Income vs EBITDA: The Quick Comparison

| Metric | What It Is | Who Uses It | Why It Matters for Loans |

|---|---|---|---|

| Net Income | Bottom-line profit after all expenses, per your IRS-filed return (Schedule C, Form 1120, K-1) | IRS, tax preparers, sole props | Starting point for lenders—but often understates cash flow due to non-cash charges and owner-level decisions |

| EBITDA | Earnings Before Interest, Taxes, Depreciation, Amortization—reconstructed by adding back specific items to net income | SBA lenders, regional banks, credit committees | Better predictor of debt service capacity; removes noise from tax strategy and one-time costs |

Source: SBA SOP 50 10

Why Lenders Rebuild EBITDA (Even If Your Tax Return Shows a Loss)

Net income is what you report to the IRS. It’s final for tax purposes—but not always reflective of cash availability. Lenders know this. So they reconstruct a “normalized” EBITDA to assess whether your business can actually service debt.

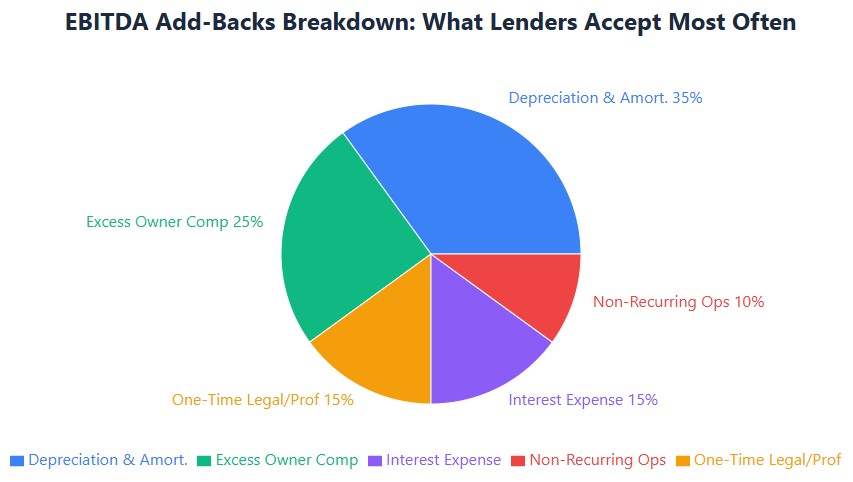

Common adjustments lenders make:

- Owner compensation: If you paid yourself $140K salary when BLS data shows $85K for your role, lenders may add back the $55K excess to EBITDA

- Non-recurring expenses: One-time legal fees, equipment buyouts, or pandemic-related costs—documented and justified

- Depreciation & amortization: Non-cash charges that reduce taxable income but don’t impact cash flow

- Interest expense: Added back because DSCR calculation uses pre-interest cash flow

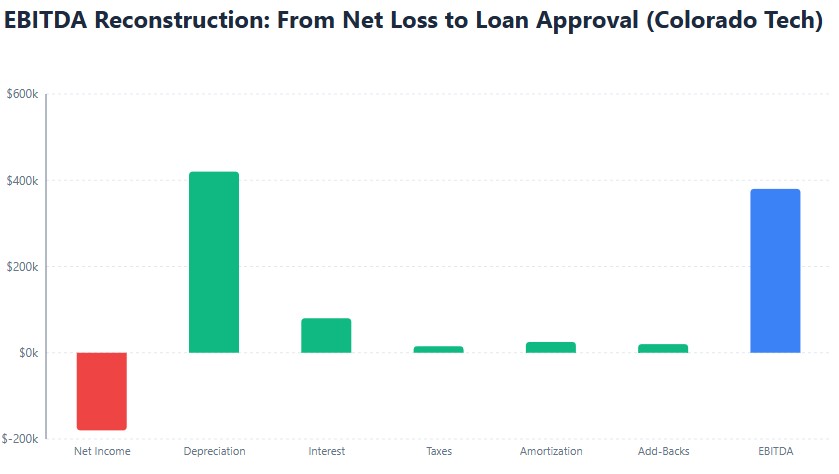

Real example: A Colorado tech startup reported a $180K net loss due to R&D tax credits and $420K in depreciation. After adding back non-cash expenses and normalizing founder pay, EBITDA hit $380K. Lender approved a $600K SBA 7(a) loan with a DSCR of 1.22x.

How to Calculate Lender-Ready EBITDA (Step by Step)

- Start with your IRS-filed net income

Pull line 31 from Schedule C, line 23 from Form 1120, or your K-1. This is your official profitability—and the foundation lenders verify via IRS Form 4506-C. - Add back interest, taxes, depreciation, amortization

These are the core EBITDA add-backs. Pull depreciation from IRS Form 4562. Interest and taxes come from your P&L. - Document allowable adjustments

Only add back expenses that are: (a) non-recurring, (b) well-documented, and (c) not part of ongoing operations. Examples: $18K one-time legal settlement, $12K equipment buyout, excess owner salary (with BLS justification). - Normalize owner compensation

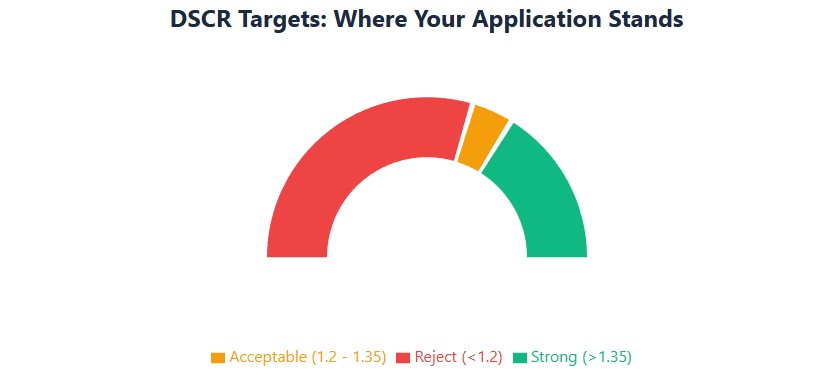

Use BLS Occupational Employment Statistics or industry surveys to justify adjustments. Lenders won’t accept “I pay myself what I want” without data. - Calculate DSCR

Formula: Normalized EBITDA ÷ Annual Debt Service

Target: ≥1.2x minimum; ≥1.35x to stand out. Example: $150K EBITDA ÷ $100K annual loan payments = 1.5x DSCR. - Bundle your package

Include: 3 years of tax returns, personal financial statement (SBA Form 413), business bank statements (last 12 months), and a one-page EBITDA reconciliation worksheet.

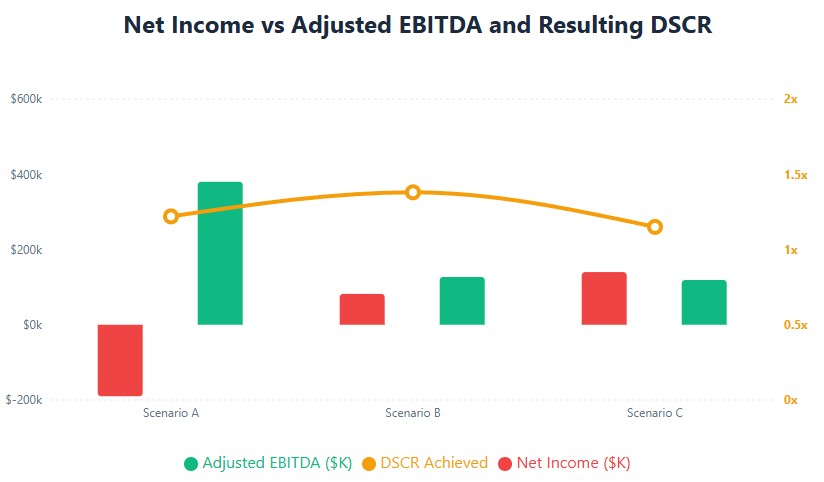

Real Scenarios: How Lenders Weigh EBITDA vs Net Income in 2026

One-size-fits-all doesn’t work. Your business stage and structure should dictate your financial narrative.

Scenario 1: Asset-Heavy Startup with High Depreciation

- Reported: $190K net loss (due to R&D credits + $420K depreciation)

- Lender adjustment: Added back depreciation, normalized founder salary, excluded one-time setup costs

- Result: $380K EBITDA → DSCR 1.22x → $600K SBA 7(a) approved

- Key takeaway: Lead with EBITDA when non-cash charges distort net income

Scenario 2: Sole Proprietor with Above-Market Owner Pay

- Reported: $82K net income on Schedule C

- Lender adjustment: Added back $45K excess salary (market rate: $85K vs. paid: $130K)

- Result: $127K EBITDA → DSCR 1.38x → loan approved with standard terms

- Key takeaway: Document owner compensation benchmarks—don’t assume lenders will guess

Scenario 3: Mature LLC with Declining Cash Flow

- Reported: $140K net income, but EBITDA down 15% YoY

- Lender response: Required two years of reviewed financials + cash flow covenant

- Result: Approved with tighter terms (higher rate, shorter amortization)

- Key takeaway: Trend matters more than a single year. Show a plan to stabilize or grow EBITDA

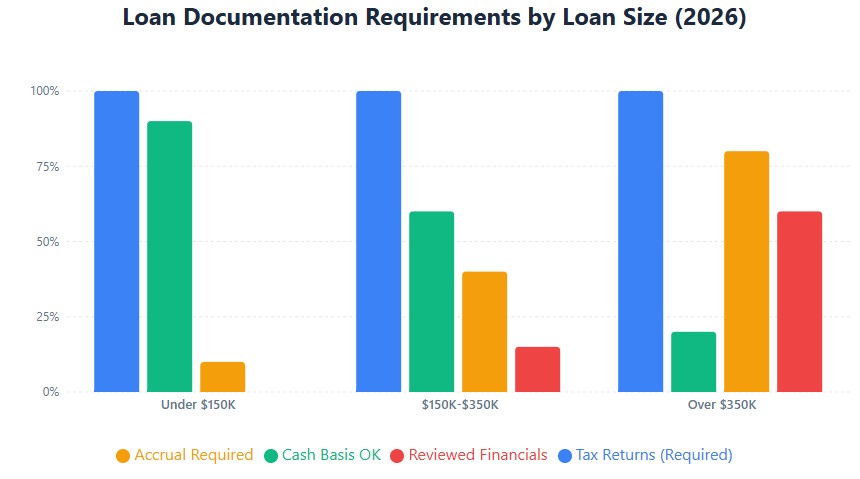

5 Mistakes That Kill Loan Applications (And How to Avoid Them)

- Submitting cash-basis statements for loans over $350K

Most SBA lenders require accrual-basis financials for larger loans. Cash basis can spike revenue from pre-paid contracts, distorting trends. Fix: Work with a CPA to restate financials—or apply for a smaller amount. - Adding back expenses without documentation

Claiming a $30K “consulting” add-back with no contract, invoice, or 1099? Lenders will reject it. Fix: Keep a reconciliation worksheet with receipts, vendor names, and business purpose for every adjustment. - Confusing owner draws with salary

Draws don’t hit the P&L—they’re balance sheet movements. You can’t “add back” a draw. Fix: Pay yourself a documented salary (W-2 for corps, guaranteed payment for LLCs) and track draws separately. - Ignoring state nexus obligations

Storing inventory in California creates an $800 annual franchise tax liability—even if your LLC is registered in Nevada. Unpaid state taxes can delay or deny SBA loans. Fix: Run a nexus check via the Streamlined Sales Tax Governing Board before applying. - Overlooking personal credit and global cash flow

For sole props and small LLCs, lenders often combine business and personal cash flow. A 620 personal credit score can offset strong business EBITDA. Fix: Check your personal credit (Experian, Equifax, TransUnion) and address errors early.

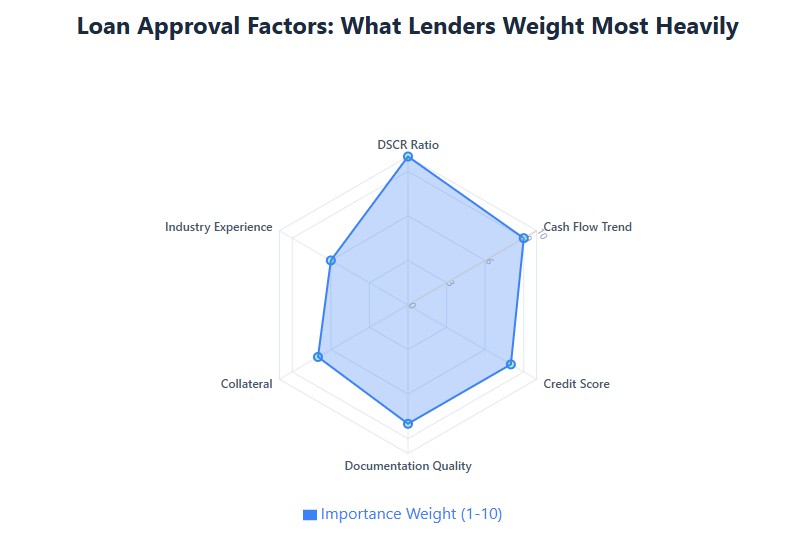

What Lenders Actually Require: The 2026 Documentation Checklist

This isn’t pass/fail—but missing items will stall your application. Lenders cross-check every box.

- Three years of filed tax returns (Schedule C, Form 1120/1120-S, or K-1s) + IRS transcripts via Form 4506-C

- Year-to-date financial statements (P&L, balance sheet, cash flow)—accrual basis preferred for loans >$350K

- Personal financial statement (SBA Form 413) for owners with 20%+ stake

- Business bank statements (last 12 months) to reconcile revenue and cash flow

- EBITDA reconciliation worksheet (one page) showing net income → EBITDA → DSCR calculation

- Debt schedule listing all existing loans, payments, and maturity dates

- Collateral documentation (real estate deeds, equipment titles, inventory appraisals) if required

Source: SBA SOP 50 10 (Latest Revision)

When to Lead with EBITDA vs Net Income

| Your Situation | Lead With | Why | DSCR Target |

|---|---|---|---|

| Startup with heavy depreciation or R&D costs | EBITDA | Net income is distorted by non-cash charges; EBITDA shows operating cash generation | ≥1.15x (with strong pro forma) |

| Mature business with steady profits | Net Income | Consistency and tax compliance signal reliability; less need for adjustments | ≥1.25x |

| Multi-owner LLC with variable compensation | Adjusted EBITDA | Normalizing owner pay reveals true cash flow; requires clear operating agreement | ≥1.2x |

| Business with recent one-time costs | EBITDA + Add-Back Memo | Documenting non-recurring expenses justifies higher cash flow for debt service | ≥1.2x (with documentation) |

Founder FAQs (2026 Answers)

Is EBITDA required for SBA loan applications?

Not formally—but lenders calculate it to assess DSCR. Provide a reconciliation worksheet to control the narrative and avoid surprises.

Can I use EBITDA if my business has never made a profit?

Rarely for conventional loans. For startups, some lenders accept pro forma EBITDA if backed by signed contracts, revenue pipeline, and clear assumptions. SBA Form 159 is required if a third party prepares the application.

How do lenders verify my net income?

Via IRS Form 4506-C—lenders request tax transcripts directly. Discrepancies between your application and IRS data are automatic red flags. Always review your own transcripts first using IRS Get Transcript.

What’s the minimum credit score for a business loan?

Most SBA lenders prefer 680+ for the primary owner, but it’s not absolute. Lower scores may require more collateral, a co-signer, or a stronger EBITDA story.

Do I need accrual accounting to get a loan?

Not always—but for loans over $350K, most SBA lenders will request accrual-basis financials. Cash basis can work for smaller amounts if revenue recognition is straightforward.

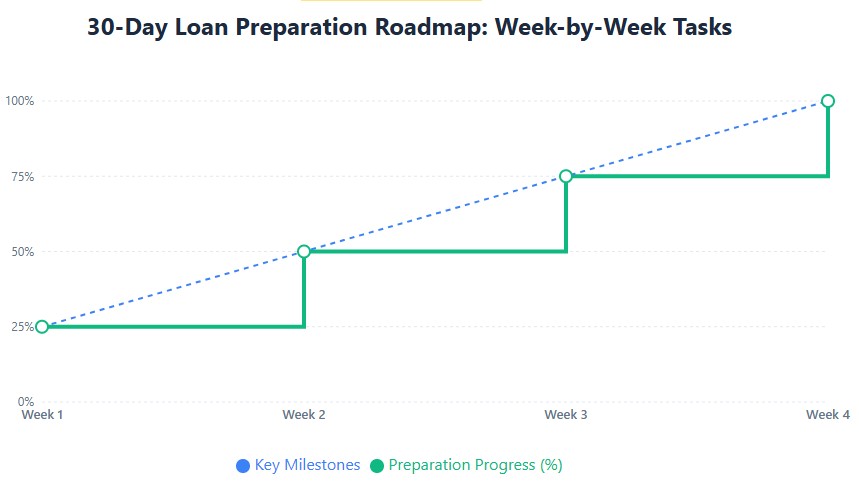

Next Steps: Get Loan-Ready in 30 Days

- Week 1: Request your IRS tax transcripts via Form 4506-T. Review for accuracy. Pull your Dun & Bradstreet PAYDEX score and dispute errors.

- Week 2: Reconstruct EBITDA using the 5-step method above. Draft a one-page reconciliation worksheet with documentation references.

- Week 3: Consult a CPA with SBA lending experience. Clarify Form 1120 vs. 1120-S implications, state filings, and accrual restatement needs.

- Week 4: Assemble your package: tax returns, financials, bank statements, EBITDA worksheet, and personal financial statement. Pre-screen with a CDC or SBA lender before formal submission.

One Last Thing

Lenders don’t lend on tax returns alone. They lend on cash flow confidence. Your job isn’t to game the numbers—it’s to present them clearly, document adjustments rigorously, and show that your business can repay debt even when the IRS says you barely broke even.

Get this right, and you’ll stand out from applicants who just submit forms and hope. That’s the difference between “maybe” and “approved.”