Here’s the uncomfortable truth: Your balance sheet is lying to you.

Not intentionally. But if you’re valuing equipment at historical cost while replacement costs have jumped 15% due to inflation, or if you’re expensing all R&D while your competitors are capitalizing software development under ASC 985-20, your financial statements don’t reflect reality. And in 2026, with SBA lenders requiring third-party IP appraisals for loans over $250K and the IRS using AI-driven analytics to spot depreciation anomalies, “close enough” gets you denied funding or audited.

This guide is built for CFOs and founders who need actionable frameworks, not theory. We’ll cover:

- How to maintain three parallel valuations (GAAP, Tax, Lender) without losing your mind

- Exact Section 179 and Bonus Depreciation limits for 2026 (with phase-out thresholds)

- Step-by-step DCF model for valuing AI models and proprietary datasets

- Real case study: SaaS startup Series A showing GAAP vs Tax vs Lender balance sheets side-by-side

- Downloadable templates: Book-Tax reconciliation schedule, Fixed Asset Register, IP impairment checklist

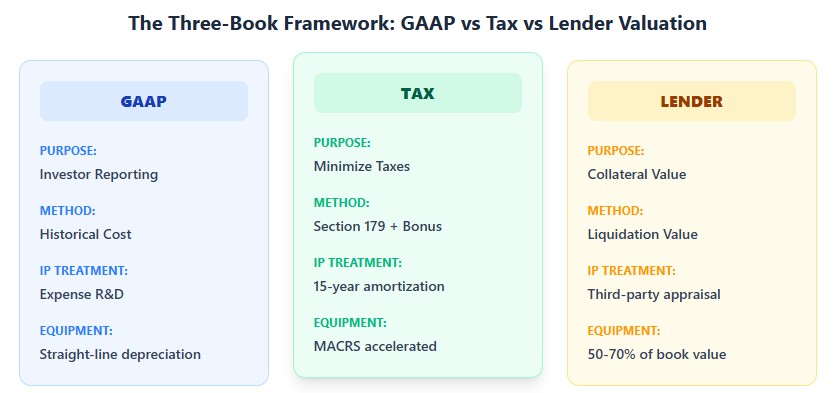

The Three-Book Problem: Why One Asset Has Three Values

You’re not maintaining one balance sheet. You’re maintaining three:

Book 1: GAAP (For Investors & Financial Reporting)

Conservative, historical cost-based, focused on reliability. Internally developed IP? Generally expensed. Equipment? Depreciated over economic useful life using straight-line.

Book 2: IRS Tax (For Minimizing Taxes)

Aggressive deductions. Section 179 allows expensing up to $2.89M in 2026 (up from $1.16M in 2023). Bonus depreciation is 100% for qualified property placed in service after 2025 (per the Tax Cuts and Jobs Act sunset provisions). But California adds back bonus depreciation on state returns.

Book 3: Lender Valuation (For Getting Loans)

Liquidation value, not book value. That $500K server cluster? Worth $250K max in a fire sale. Your proprietary AI model? Worth $0 unless you have a third-party appraisal and proven revenue attribution.

The CFO Strategy: Maintain a Book-Tax Difference Schedule (download template below). Reconcile quarterly. Never mix these valuations in investor presentations.

Equipment Valuation: 2026 Rules and Real Numbers

Inflation has broken the old rules. A $2,500 capitalization threshold made sense in 2020. In 2026, a MacBook Pro costs $3,800. Here’s how to adapt.

What Gets Capitalized (The Complete List)

Under GAAP (ASC 360), capitalize all costs necessary to get the asset ready for its intended use:

- Purchase price

- Sales tax (non-deductible portion)

- Freight and shipping

- Installation and calibration

- Testing costs (materials consumed during testing)

- Professional fees (engineering, legal for installation contracts)

Real Example: You purchase a CNC machine for $150,000. Shipping: $4,500. Installation: $8,000. Calibration materials: $2,500. Legal fees for installation contract: $3,000.

Correct Asset Value: $168,000. Not $150,000.

2026 Depreciation: GAAP vs Tax Comparison

| Feature | GAAP (ASC 360) | IRS Tax (2026) | Book-Tax Difference |

|---|---|---|---|

| Method | Straight-line (typically) | MACRS 200% DB or Section 179 | Timing difference |

| Useful Life | Economic life (5-7 years for tech) | IRS Class Life (5-year for computers) | Potential permanent difference |

| Section 179 Limit | N/A | $2.89M (2026), phases out at $4.12M | Accelerated deduction |

| Bonus Depreciation | N/A | 100% for qualified property (post-2025) | Full expensing vs multi-year |

| Salvage Value | Subtracted from depreciable base | Ignored under MACRS | Permanent difference |

Case Study: Hardware Startup Equipment Strategy

Company: Robotics manufacturer, Series A, $8M revenue

Equipment: $450K in CNC machines, $120K in testing equipment, $85K in computers

GAAP Treatment:

- CNC machines: 7-year straight-line, $64,286/year depreciation

- Testing equipment: 5-year straight-line, $24,000/year

- Computers: 3-year straight-line, $28,333/year

- Total Year 1 GAAP Depreciation: $116,619

Tax Treatment (Maximizing Deductions):

- Elect Section 179 on CNC machines: $450K immediate deduction

- Bonus depreciation (100%) on testing equipment: $120K immediate deduction

- Computers under de minimis safe harbor ($2,500 threshold): Expense $85K

- Total Year 1 Tax Deduction: $655,000

Book-Tax Difference: $655,000 – $116,619 = $538,381 favorable temporary difference

Lender View (SBA 7(a) Application):

- Equipment appraised at 60% of book value (ordered liquidation value)

- CNC machines: $270,000 collateral value

- Testing equipment: $72,000 collateral value

- Computers: $0 (too specialized/rapid obsolescence)

- Total Collateral Value: $342,000 (vs $655,000 book cost)

Strategic Insight: The startup maximizes tax deductions while maintaining clean GAAP books for investors. But when applying for an SBA loan, they can only borrow against 52% of their equipment cost. This gap must be bridged with other collateral or personal guarantees.

Intellectual Property Valuation: The 2026 Framework

IP valuation has changed dramatically. In 2023, a self-prepared valuation might suffice. In 2026, SBA lenders and Series A investors require third-party appraisals for IP over $250K, especially for AI models and proprietary datasets.

When Can You Capitalize IP? (Decision Tree)

Step 1: Is the IP for internal use or external sale?

- Internal Use (ASC 350-40): Expense all development costs. Examples: Internal ERP, custom CRM, proprietary data analytics tools.

- External Sale/Lease (ASC 985-20): Continue to Step 2.

Step 2: Has technological feasibility been established?

- No: Expense all costs as R&D.

- Yes: Capitalize direct development costs (developer salaries, cloud infrastructure for testing, third-party contractors).

Step 3: Has the product been released?

- No: Continue capitalizing.

- Yes: Stop capitalizing. Begin amortization over useful life (typically 3-5 years for software).

Documentation Required:

- Working prototype with test results

- Technical feasibility sign-off from CTO/lead engineer

- Time tracking logs for capitalized hours

- Cloud infrastructure costs allocated to development vs production

Three Valuation Methods (With 2026 Examples)

1. Cost Approach (The Floor)

Formula: (Development Hours × Market Rate) + Legal Fees + Testing Costs + Overhead Allocation

Example: Proprietary AI recommendation engine

- Senior ML Engineer: 800 hours × $175/hour = $140,000

- Junior Engineer: 1,200 hours × $95/hour = $114,000

- Cloud infrastructure (AWS SageMaker): $28,000

- Legal fees (patent filing): $18,000

- Testing/QA: $15,000

- Total Cost: $315,000

When to Use: Early-stage IP with no revenue. Sets the minimum value.

Limitation: Doesn’t reflect market value. A failed product cost money but is worth $0.

2. Market Approach (The Benchmark)

Formula: Comparable Licensing Deals × Revenue Multiple or Royalty Rate

Example: SaaS platform with $2M ARR

- Comparable SaaS acquisitions trade at 8-12× ARR

- Midpoint: 10× $2M = $20M enterprise value

- IP represents 60% of value (rest is team, customers, brand)

- IP Value: $12M

When to Use: M&A transactions, investor valuations.

Limitation: Requires comparable transactions. Hard for unique AI models.

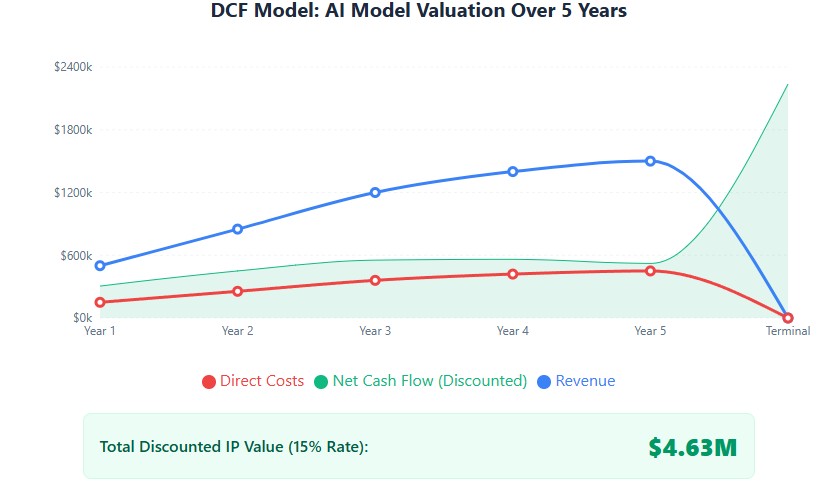

3. Income Approach (The Gold Standard for 2026)

Formula: DCF of IP-Attributable Cash Flows, Discounted at Risk-Adjusted Rate

Step-by-Step DCF Model:

| Year | IP Revenue | Direct Costs | Net Cash Flow | Discount Factor (15%) | PV |

|---|---|---|---|---|---|

| Year 1 | $500,000 | $150,000 | $350,000 | 0.870 | $304,500 |

| Year 2 | $850,000 | $255,000 | $595,000 | 0.756 | $449,820 |

| Year 3 | $1,200,000 | $360,000 | $840,000 | 0.658 | $552,720 |

| Year 4 | $1,400,000 | $420,000 | $980,000 | 0.572 | $560,560 |

| Year 5 | $1,500,000 | $450,000 | $1,050,000 | 0.497 | $521,850 |

| Terminal Value (Year 5 × 3× multiple) | 0.497 | $2,236,500 | |||

| Total IP Value (Sum of PV) | $4,625,950 | ||||

Key Assumptions:

- Revenue growth: 70% → 41% → 17% → 7% (maturing product)

- Direct costs: 30% of revenue (cloud infrastructure, support)

- Discount rate: 15% (startup risk premium)

- Terminal multiple: 3× (conservative for established IP)

- Useful life: 5 years (software obsolescence)

When to Use: SBA loans, Series A+ fundraising, M&A. This is what lenders and investors expect in 2026.

2026 Trend: AI Model and Dataset Valuation

Traditional IP valuation doesn’t work for AI models. Here’s what lenders are asking for:

Required Documentation:

- Training Cost Breakdown: GPU hours, data acquisition costs, engineer time

- Performance Metrics: Accuracy, precision, recall compared to benchmarks

- Revenue Attribution: What % of revenue is directly attributable to the AI model? (Use A/B testing data)

- Defensibility: Patents, trade secrets, data moats

- Third-Party Appraisal: Required for loans >$250K. Use ASA (American Society of Appraisers) certified professionals.

Case Study: Fintech startup with proprietary fraud detection AI

Model: Neural network trained on 5M transactions

Valuation Method: Income approach with A/B testing validation

Result: Model reduces fraud by 0.3%, saving $2M/year. Capitalized value: $8.5M (4.25× annual savings, 5-year life, 15% discount rate).

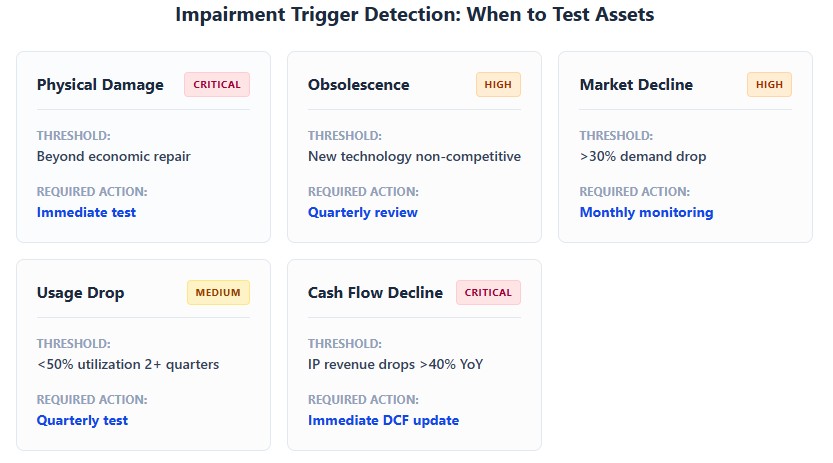

Impairment Testing: When to Write Down Assets

You don’t test annually. You test when triggering events occur. Missing these is a common audit flag.

Triggering Events (ASC 360-10-35)

- Physical Damage: Equipment destroyed or damaged beyond economic repair

- Obsolescence: New technology makes your asset non-competitive (e.g., CPU architecture shift)

- Market Decline: >30% drop in demand for products using the asset

- Regulatory Change: New laws restrict or ban your technology

- Usage Drop: Equipment utilization falls below 50% for 2+ consecutive quarters

- Cash Flow Decline: IP-attributable revenue drops >40% YoY

Impairment Test Process

Step 1: Recoverability Test

Compare Asset Carrying Value to Undiscounted Future Cash Flows.

Example: Patent with $400K book value

– Expected cash flows (undiscounted): $350K

– Result: Impaired (cash flows < carrying value)

Step 2: Measurement

Write down to Fair Market Value.

Example (continued):

– Carrying value: $400K

– Fair value (appraisal): $280K

– Impairment loss: $120K (recognized on P&L)

Book-Tax Reconciliation: The 2026 Template

This is the document your CPA needs. Maintain it quarterly.

| Item | GAAP Book | Tax Return | Difference | Type |

|---|---|---|---|---|

| Equipment Depreciation | ||||

| CNC Machines | ($64,286) | ($450,000) | $385,714 | Temporary |

| Testing Equipment | ($24,000) | ($120,000) | $96,000 | Temporary |

| Computers | ($28,333) | ($85,000) | $56,667 | Temporary |

| Software Development | ||||

| R&D Expenses | ($450,000) | ($450,000) | $0 | None |

| Capitalized Software | $180,000 | $0 | $180,000 | Temporary |

| Net Book-Tax Difference | $718,981 |

Deferred Tax Liability: $718,981 × 21% = $150,986

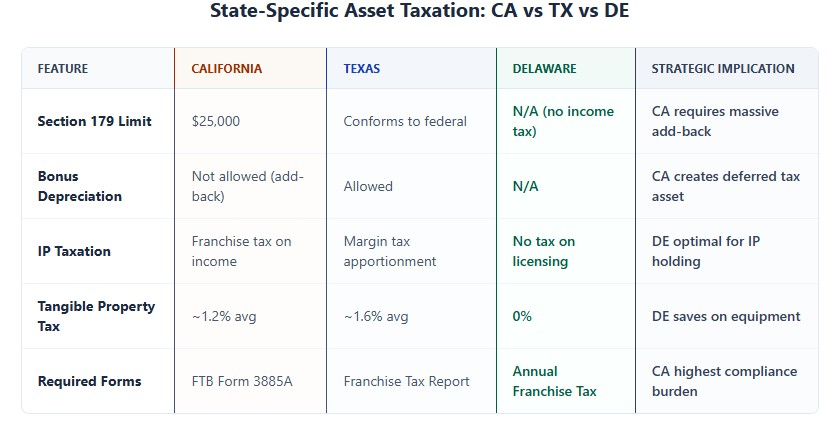

State-Specific Compliance: California, Texas, Delaware

California: The Conformity Trap

Issue: California does NOT conform to federal bonus depreciation or Section 179 limits.

Impact: If you expense $450K under Section 179 federally, you must add it back on California Form 3885A and depreciate it over 5-7 years for state tax.

2026 California Limits:

- Section 179: $25,000 (vs $2.89M federal)

- Bonus depreciation: Not allowed

- Result: Massive book-tax difference requiring detailed tracking

Texas: Franchise Tax Nuances

Issue: Texas franchise tax is based on margin, not income. Equipment depreciation affects your cost of goods sold calculation.

Strategy: Maximize COGS by properly capitalizing equipment used in production. This reduces your taxable margin.

Delaware: IP Holding Strategy

Advantage: No tangible personal property tax. No state income tax on IP licensing revenue if structured correctly.

Warning: If you hold IP in a Delaware LLC but operate in California, California may still tax the income under “economic nexus” rules.

Federal Audit Risks: What the IRS Actually Looks For

The IRS uses the Audit Technique Guide for Intangibles (ATG-12B). Here are the top triggers:

Top 5 Audit Triggers

- Missing Form 4562: If you claim depreciation or Section 179, you MUST file Form 4562. No exceptions. Missing form = automatic disallowance.

- Capitalized R&D Without Documentation: You capitalized $200K in software development but can’t produce:

- Technological feasibility documentation

- Time tracking logs

- Cloud infrastructure allocation

- Inconsistent Useful Lives: Depreciating laptops over 10 years to boost profit. IRS expects 5 years under MACRS. Result: Adjustment + interest.

- Section 179 Exceeding Income: You claimed $500K Section 179 but only had $300K taxable income. You must carry forward the excess. Failure to track = audit flag.

- IP Valuation Without Appraisal: You put $2M IP on the balance sheet with no third-party appraisal. Lenders and auditors will question this.

Decision Tools and Templates

Decision Tree: Capitalize vs. Expense

Equipment:

- Cost > $2,500 (or your capitalization threshold)? → Yes → Capitalize

- Cost < $2,500? → Expense under de minimis safe harbor (Rev. Proc. 2015-54)

Software Development:

- Internal use (ASC 350-40)? → Expense all costs

- External sale (ASC 985-20)? → Continue

- Technological feasibility established? → No → Expense | Yes → Capitalize

- Product released? → No → Continue capitalizing | Yes → Begin amortization

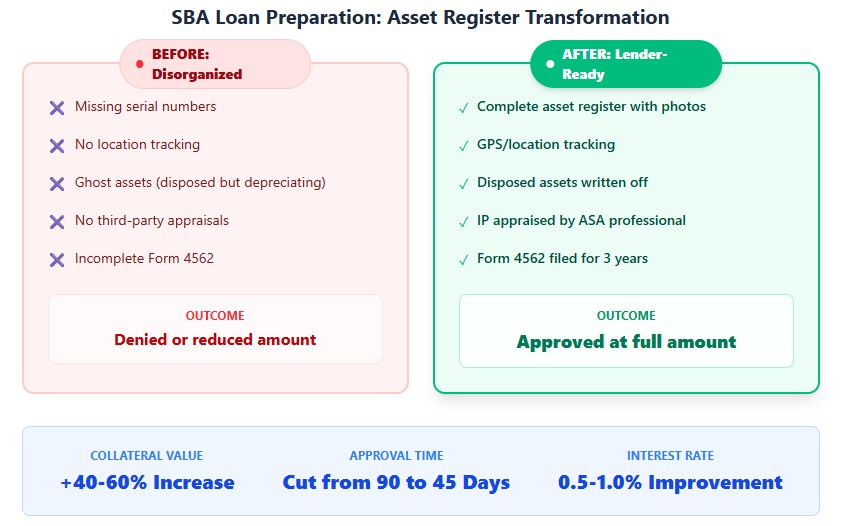

Checklist: SBA 7(a) Loan Asset Documentation

Before applying, ensure you have:

- [ ] Fixed Asset Register with serial numbers, locations, purchase dates

- [ ] Form 4562 filings for last 3 years

- [ ] Third-party appraisal for IP >$250K (ASA certified)

- [ ] Equipment insurance policies with replacement cost coverage

- [ ] Book-Tax reconciliation schedule

- [ ] Impairment testing documentation (if applicable)

- [ ] State tax clearance letters (CA, TX, NY if applicable)

- [ ] Purchase invoices and proof of payment for all assets >$10K

30-Day Action Plan for CFOs

Week 1: Audit Your Fixed Asset Register

- Export asset list from QuickBooks/Xero

- Physically verify equipment >$5K exists

- Identify “ghost assets” (still depreciating but disposed)

- Update capitalization threshold to $5K for 2026

Week 2: Review IP Classification

- List all internally developed software/patents

- Apply capitalize vs. expense decision tree

- Ensure legal fees for patents are capitalized

- Document technological feasibility for any capitalized software

Week 3: Prepare Book-Tax Reconciliation

- Work with CPA to prepare Form 4562

- Calculate deferred tax liabilities

- Review state conformity issues (especially CA)

- Update depreciation schedules for 2026 limits

Week 4: Lender/Investor Preparation

- Get equipment replacement cost quotes (for insurance)

- Engage third-party appraiser for IP >$250K

- Prepare lender valuation schedule (liquidation values)

- Update balance sheet notes with valuation methodologies

Final Thoughts

Valuing equipment and IP isn’t just compliance. It’s strategy. The startups that win in 2026 are those that:

- Maintain clean parallel books (GAAP, Tax, Lender)

- Maximize tax deductions without compromising GAAP integrity

- Document IP valuations with third-party appraisals

- Test for impairment proactively, not reactively

- Use book-tax differences as a strategic tool, not a burden

Your balance sheet tells a story. Make sure it’s the story you want investors, lenders, and the IRS to hear.