In 2026, with commercial lending standards tighter than ever, personal capital injections are no longer just a backup plan for small businesses—they are a primary funding source. But here is the hard truth most founders learn the hard way: putting your own money into your business does not automatically create “equity” on paper.

How you classify that transfer—whether as an equity contribution, a shareholder loan, or an owner draw—dictates your tax liability, your SBA loan eligibility, and your vulnerability to IRS scrutiny. The IRS is actively using data-matching algorithms to flag commingled funds, and SBA 7(a) underwriters routinely deny applications where personal deposits lack a clear, documented paper trail.

This guide cuts through the accounting jargon. We will show you exactly how to record personal investments under US GAAP, how to navigate IRS rules for 2026, and how to structure your equity section to satisfy lenders, investors, and auditors.

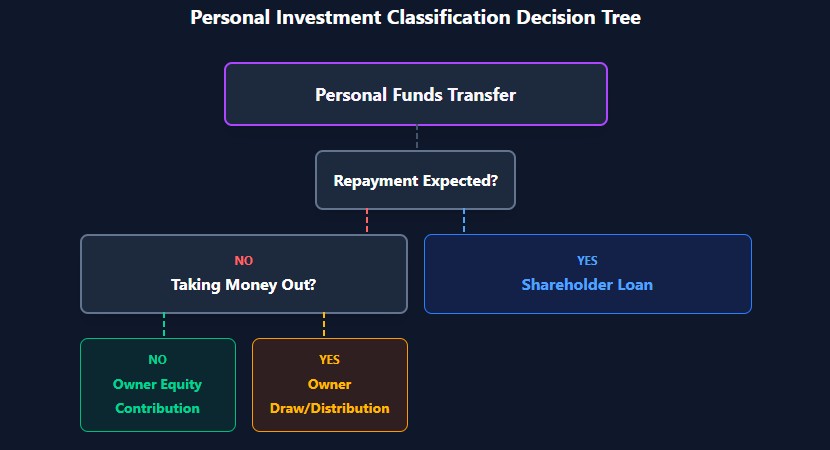

The Three Paths: How Personal Money Enters Your Business

Under US GAAP and IRS guidelines, personal funds injected into a business must follow one of three distinct paths. The path you choose is dictated by intent and documentation, not just the movement of cash.

1. Owner Equity Contribution (Capital Injection)

Intent: You are buying or increasing your ownership stake. There is no expectation of repayment.

Financial Impact: Increases the Cash asset and increases the Owner’s Equity (or Paid-In Capital) on the balance sheet. It is not taxable income to the business or the owner.

Best For: Bootstrapping, meeting SBA equity injection requirements, and building a strong balance sheet for future investors.

2. Shareholder or Owner Loan

Intent: You are lending money to the business with the explicit expectation of repayment.

Financial Impact: Increases Cash and creates a Liability (e.g., “Due to Shareholder”). The business can deduct the interest paid to you, and you must report that interest as personal income.

Best For: Short-term cash flow gaps where you want to extract the cash tax-free later, or when you want to avoid diluting your ownership percentage.

2026 IRS Trap: If you do not charge interest at or above the IRS Applicable Federal Rate (AFR)—currently hovering around 4.5% to 5.0% for mid-term loans—the IRS will “impute” interest. This means they will tax you on phantom interest income you never actually received, under IRC §7872.

3. Owner Draw or Distribution

Intent: You are taking money out of the business for personal use. (Note: Founders sometimes accidentally record a personal deposit as a “negative draw” to balance the books. This is a massive red flag).

Financial Impact: Decreases Cash and decreases Owner’s Equity (as a contra-equity account). It is not a business expense.

Best For: Mature, profitable pass-through entities (Sole Props, LLCs, S-Corps) where the owner is taking profits.

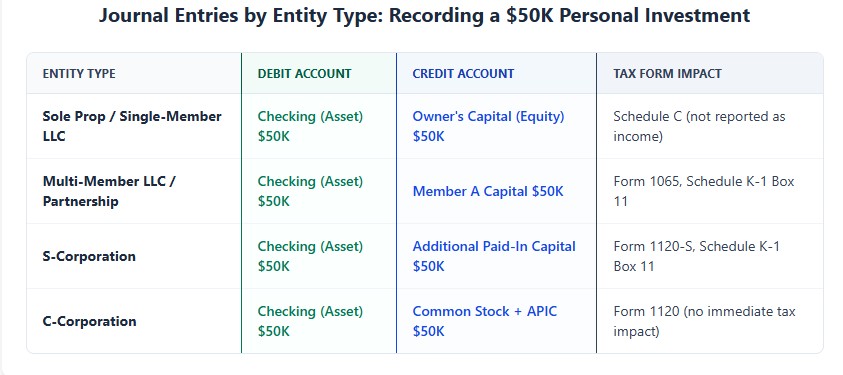

Step-by-Step: Exact Journal Entries for Your Accounting Software

Whether you use QuickBooks Online, Xero, or NetSuite, the underlying double-entry accounting remains the same. Here is exactly how to record a $50,000 personal investment based on your entity type.

Sole Proprietorship or Single-Member LLC (Disregarded Entity)

- Debit: Checking Account (Asset) – $50,000

- Credit: Owner’s Capital (Equity, typically account 3000 series) – $50,000

- Memo: “Personal capital contribution, [Date]”

Note: For tax purposes (Schedule C), this contribution is not reported as income. It simply increases your tax basis, which protects you if the business generates a loss.

Multi-Member LLC or Partnership

- Debit: Checking Account (Asset) – $50,000

- Credit: Member A Capital Account (Equity) – $50,000

- Memo: “Capital contribution per Operating Agreement dated [Date]”

Note: Treasury Regulation §1.704-1 requires partnerships to maintain specific capital accounts for each partner to track basis and allocate profits/losses correctly. A generic “Owner Equity” account is insufficient and will trigger IRS scrutiny on Form 1065.

S-Corporation

- Debit: Checking Account (Asset) – $50,000

- Credit: Additional Paid-In Capital (APIC) or Common Stock (Equity) – $50,000

- Memo: “Shareholder capital contribution, no new shares issued”

Note: In an S-Corp, contributions increase the shareholder’s stock basis (Form 1120-S, Schedule K-1, Box 11). This is critical because S-Corp losses can only be deducted up to the shareholder’s basis. If you take money out without basis, it becomes a taxable capital gain.

C-Corporation

- Debit: Checking Account (Asset) – $50,000

- Credit: Common Stock (at par value, e.g., $10) and Additional Paid-In Capital (APIC) (for the remainder, e.g., $49,990)

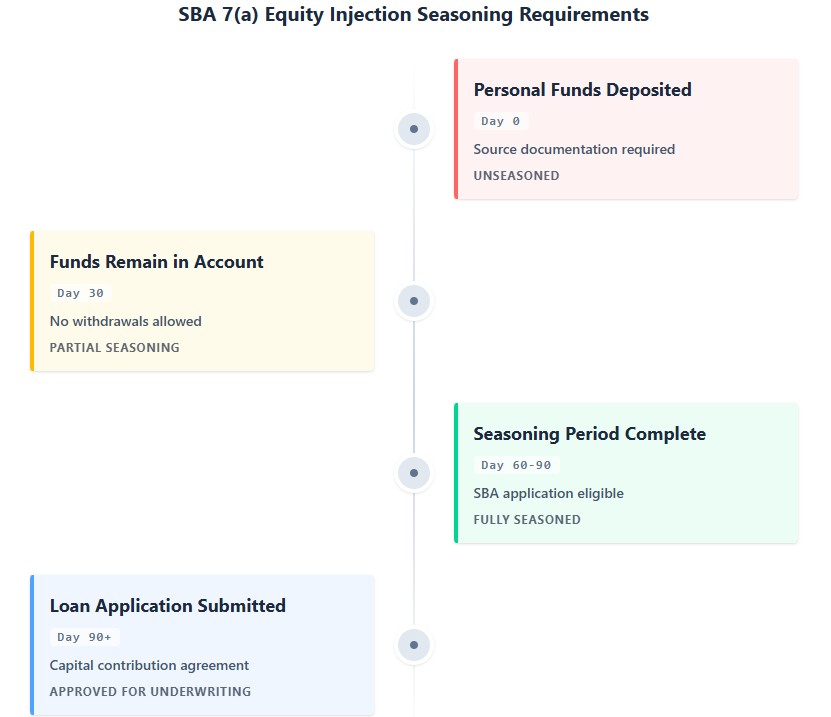

The SBA 7(a) Reality Check: The “Seasoning” Rule

If you are injecting personal funds to qualify for an SBA 7(a) loan, you must understand the Equity Injection Seasoning Rule. This is the number one reason small business loan applications are delayed or denied.

SBA lenders require a minimum equity injection (typically 10% for new businesses or acquisitions). However, they will not accept a $50,000 personal deposit made the day before you apply. They view this as “unseasoned” funds, suspecting it might be a hidden, undisclosed loan from a friend or a credit card cash advance.

The 2026 Lender Standard:

- Seasoning Period: Funds must sit in the business checking account for at least 60 to 90 days prior to the loan application.

- Source Documentation: If the funds are not seasoned, you must provide a clear paper trail: personal bank statements showing the money was yours, the transfer receipt, and a signed “Gift Letter” or “Capital Contribution Agreement” stating the funds are not a loan and require no repayment.

- No Borrowed Equity: You cannot take a HELOC or personal loan to fund the business equity injection unless it is fully secured by assets outside the business (like your primary residence) and disclosed to the SBA.

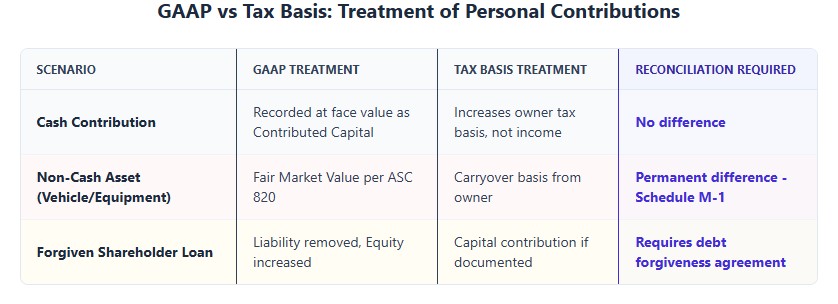

GAAP vs. Tax Basis: The Reconciliation Gap

Most small businesses prepare tax returns on a cash or tax basis but may need GAAP-compliant financials for lenders or investors. A personal contribution highlights the difference between these two frameworks.

| Scenario | GAAP Treatment (ASC 210 / ASC 820) | Tax Basis Treatment (IRS) | Reconciliation Note |

|---|---|---|---|

| Cash Contribution | Recorded at face value as Contributed Capital. | Increases owner’s tax basis. Not reported as income on the tax return. | No book-tax difference. Both show increased equity/basis. |

| Non-Cash Contribution (e.g., Founder’s Vehicle) | Recorded at Fair Market Value (FMV) on the date of transfer (per ASC 820). | Generally, the business takes the founder’s carryover basis (what the founder originally paid, minus depreciation), not the FMV. | Permanent Difference: GAAP shows a higher asset and equity value than the tax return. Requires a Schedule M-1 or M-3 reconciliation. |

| Owner Loan Forgiven | Liability is removed, Equity is increased. | May be treated as a capital contribution (non-taxable) if properly documented, or cancellation of debt (COD) income if not. | Requires a formal “Debt Forgiveness Agreement” to avoid IRS treating it as taxable income. |

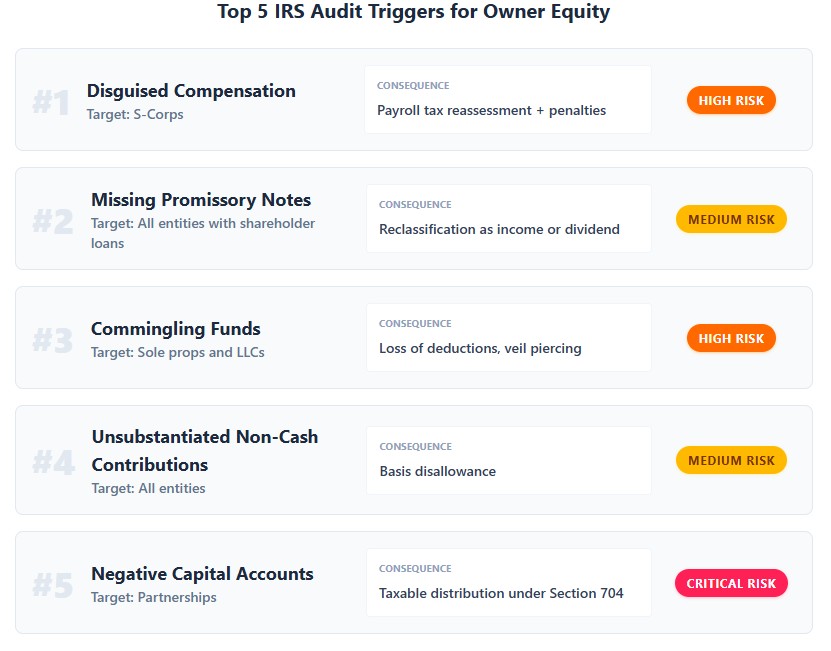

Top 5 IRS Audit Triggers Related to Owner Equity

The IRS does not audit small businesses randomly. Their automated systems look for specific anomalies in the equity and liability sections of your return.

1. The “Disguised Compensation” Trap (S-Corps)

If you funnel personal money into the business as a “loan” or “equity,” but then take it out as an “owner draw” instead of W-2 wages, the IRS will flag you. S-Corp owners must pay themselves “reasonable compensation” subject to payroll taxes. Using equity accounts to bypass payroll taxes is a primary target for IRS audits.

2. Missing Promissory Notes for “Loans”

If your balance sheet shows a $100,000 “Due to Shareholder” liability, but there is no signed promissory note, no stated interest rate, and no actual repayment history, the IRS may reclassify the entire amount. They could view the initial deposit as income (if it looks like a customer payment) or the eventual repayment as a taxable dividend.

3. Commingling of Funds

Paying personal mortgage payments directly from the business checking account, or depositing business revenue into a personal account, destroys the “corporate veil.” While not always a direct tax violation for sole props, it makes your financial statements unreliable and can lead to the IRS disallowing business deductions entirely.

4. Unsubstantiated Non-Cash Contributions

Contributing a $15,000 laptop to the business and claiming a $15,000 basis increase without an appraisal or original purchase receipt will be disallowed upon audit. The IRS requires substantiation for the FMV of non-cash contributions.

5. Negative Capital Accounts in Partnerships

If a partner takes distributions exceeding their basis, their capital account goes negative. The IRS views this as a taxable event (a disguised loan or capital gain). Treasury Regulation §1.704-1(b)(2)(ii)(d) strictly governs this, and negative balances are a massive red flag on Form 1065.

State-Specific Compliance Nuances for 2026

While the IRS handles federal taxes, state agencies have their own rules regarding capital and equity reporting.

- California: The Franchise Tax Board (FTB) closely scrutinizes S-Corp and LLC filings. If your federal return shows a large shareholder loan but your California return does not reconcile the basis correctly, expect a notice. California also requires a biennial Statement of Information, though it does not require detailed capital breakdowns.

- Texas: The Texas Franchise Tax is based on “margin,” not capital. However, the Comptroller may request your balance sheet during an audit to verify your Cost of Goods Sold (COGS) or compensation deductions, making accurate equity and liability classification critical.

- Delaware: If you are a C-Corp, your annual Franchise Tax is calculated based on your authorized shares or assumed par value capital. A massive, undocumented increase in your “Common Stock” account without updating your Certificate of Incorporation can lead to miscalculated taxes and penalties.

- New York: New York LLCs must file a Biennial Statement. While it focuses on addresses and registered agents, the Department of Taxation and Finance actively cross-references federal K-1s with state filings to ensure capital contributions are properly reported for the fixed dollar minimum tax calculations.

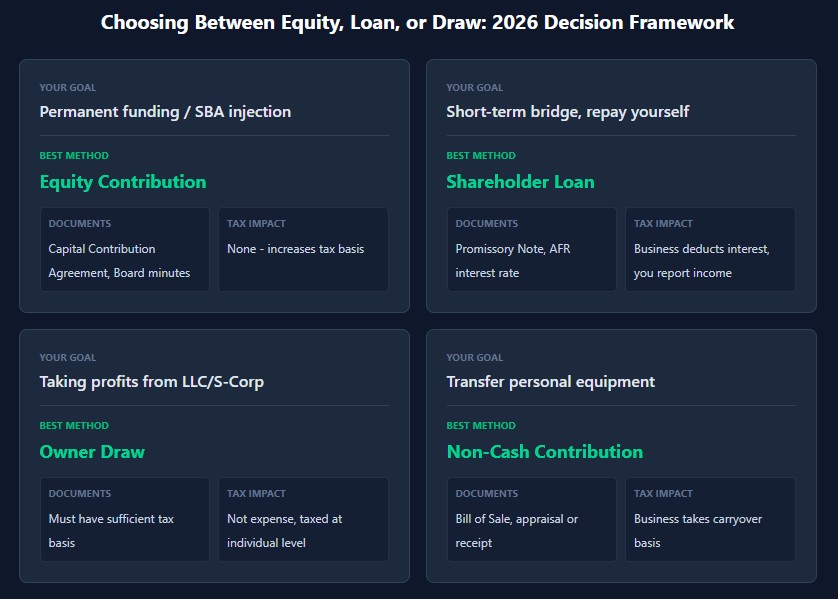

Decision Framework: Equity vs. Loan vs. Draw

Before transferring your next $20,000, run it through this quick decision matrix.

| Goal | Recommended Method | Required Documentation | Tax Consequence |

|---|---|---|---|

| Permanently fund the business / SBA equity injection | Equity Contribution | Capital Contribution Agreement, board minutes (if Corp) | None. Increases tax basis. |

| Short-term cash flow bridge, plan to repay yourself | Shareholder Loan | Promissory Note, AFR interest rate, repayment schedule | Business deducts interest; you report interest income. |

| Taking profits out of a profitable LLC/S-Corp | Owner Draw / Distribution | None (but must have sufficient tax basis) | Not a business expense. Taxed at the individual level (already taxed at entity level for pass-throughs). |

| Transferring personal equipment to the business | Non-Cash Contribution | Bill of Sale, independent appraisal or original receipt | Business takes carryover basis for tax; FMV for GAAP. |

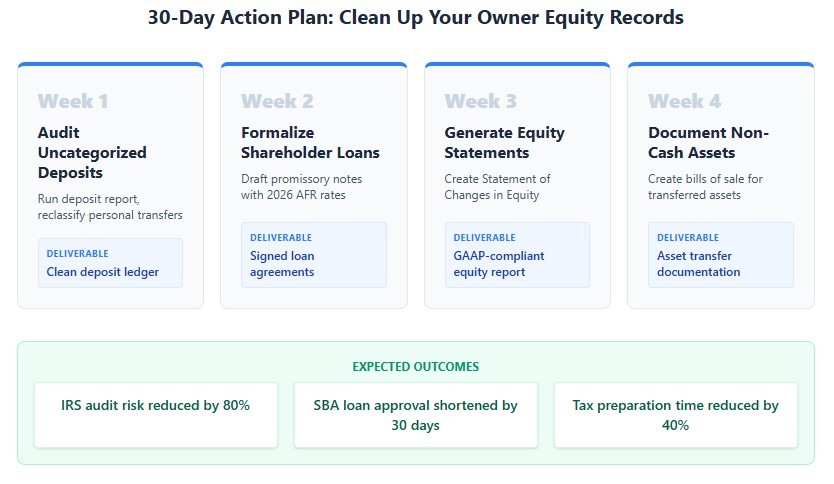

Your 30-Day Action Plan for Clean Equity Records

Do not wait for tax season or a loan application to fix your equity section. Take these steps this month:

- Audit Your “Uncategorized” Deposits: Run a deposit report in QuickBooks/Xero for the last 12 months. Identify any personal transfers labeled “Deposit” or “Transfer” and reclassify them to the correct equity or liability account.

- Formalize Existing Loans: If you have a “Due to Shareholder” balance, draft a retroactive promissory note with a 2026 AFR-compliant interest rate and begin making documented repayments.

- Generate a Statement of Changes in Equity: If you are an LLC or Corporation, ensure your CPA generates this statement. It clearly shows Beginning Equity + Contributions – Distributions + Net Income = Ending Equity.

- Document Non-Cash Assets: If you are using a personal vehicle or computer for the business, create a simple “Bill of Sale” transferring it to the business at a documented fair market value.

- Separate Your Accounts: If you are still using one bank account for personal and business expenses, open a dedicated business account today. The cost of fixing commingling later far exceeds the cost of a new bank account.

Final Thoughts

Your balance sheet is a legal document. Every dollar that crosses the threshold between your personal life and your business must have a name, a purpose, and a paper trail. Treating owner equity as a “black box” might save you five minutes today, but it invites IRS scrutiny, complicates tax prep, and can single-handedly derail an SBA loan application tomorrow.

By classifying your personal investments correctly, maintaining strict GAAP and tax basis alignment, and documenting your intent, you transform your financial statements from a source of risk into a tool for growth.