In 2026, the “growth at all costs” era is officially dead. If you are pitching investors today, they aren’t just looking at your top-line revenue growth. They are dissecting your balance sheet to see if your business can survive a winter without their next check.

With interest rates stabilizing but remaining elevated, and venture capital deployment more selective than ever, your balance sheet has become the primary gatekeeper for funding. A messy equity section, inflated receivables, or hidden liabilities won’t just lower your valuation—they will kill the deal before it starts.

This guide cuts through the accounting theory. We’ll show you exactly which balance sheet metrics US investors scrutinize in 2026, how to clean up common red flags, and how to present your financials to pass due diligence with flying colors.

The Big Shift: From P&L Obsession to Balance Sheet Reality

For years, startups lived and died by their Income Statement (P&L). Revenue was king. But in today’s market, investors know that revenue can be manipulated through aggressive recognition policies. The balance sheet, however, tells the truth about liquidity and solvency.

Here is what has changed in investor mindset:

- Liquidity over Growth: Investors now prioritize companies that can fund their own operations for 18+ months. Your cash position and working capital efficiency matter more than your month-over-month growth rate.

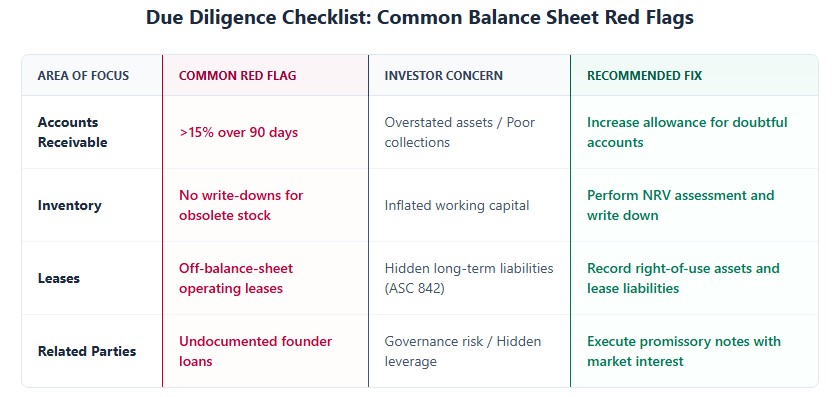

- Quality of Assets: It’s not enough to have $1M in Accounts Receivable. If 40% of it is over 90 days old, investors view it as worthless. They are auditing your aging reports, not just your totals.

- Debt Structure Clarity: Post-SVB, investors are terrified of hidden leverage. They want to see every convertible note, SAFE, and vendor loan clearly classified. No more “off-balance-sheet” surprises.

The 5 Critical Balance Sheet Metrics Investors Check First

When an investor opens your data room, they don’t read every line item immediately. They look for five specific health indicators. If these fail, they often stop digging.

1. The Current Ratio (Liquidity Health)

Formula: Current Assets / Current Liabilities

What it tells investors: Can you pay your bills due in the next 12 months?

The 2026 Benchmark: A ratio below 1.0 is an immediate red flag for insolvency risk. For early-stage startups, investors typically look for a ratio between 1.5 and 2.0. This shows you have enough liquid assets to cover short-term obligations while still investing in growth.

Common Trap: Including slow-moving inventory or uncollectible receivables in “Current Assets.” If your inventory hasn’t moved in six months, it shouldn’t be counted as a liquid asset in your investor pitch.

2. The Quick Ratio (Acid-Test)

Formula: (Cash + Marketable Securities + Accounts Receivable) / Current Liabilities

What it tells investors: Can you survive if your sales stop tomorrow?

Why it matters: Unlike the Current Ratio, this excludes inventory and prepaid expenses. For SaaS and service businesses, this is often a more accurate measure of true liquidity because you don’t have physical stock to sell off in an emergency.

The Target: Ideally above 1.0. If it’s below 1.0, you are relying on selling inventory or collecting old debts to keep the lights on.

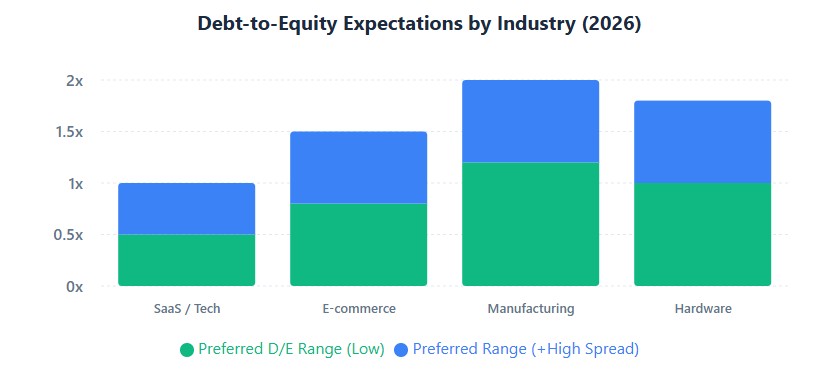

3. Debt-to-Equity Ratio (Leverage Risk)

Formula: Total Liabilities / Total Shareholders’ Equity

What it tells investors: How much of your company is funded by debt vs. owner/investor money?

The 2026 Benchmark: This varies heavily by industry.

- SaaS/Tech: Investors prefer a low ratio (0.5 – 1.0) because these companies should be asset-light.

- Manufacturing/Hardware: Higher ratios (1.5 – 2.0) are acceptable due to heavy equipment costs.

Red Flag: A rising D/E ratio without a corresponding increase in revenue suggests you are borrowing to survive, not to grow.

4. Working Capital Efficiency

Formula: Current Assets – Current Liabilities

What it tells investors: Do you have enough operational cushion?

Investor Focus: They don’t just look at the total number; they look at the trend. Is your working capital shrinking while revenue grows? That’s a sign of poor cash management. They want to see positive working capital that scales with your business.

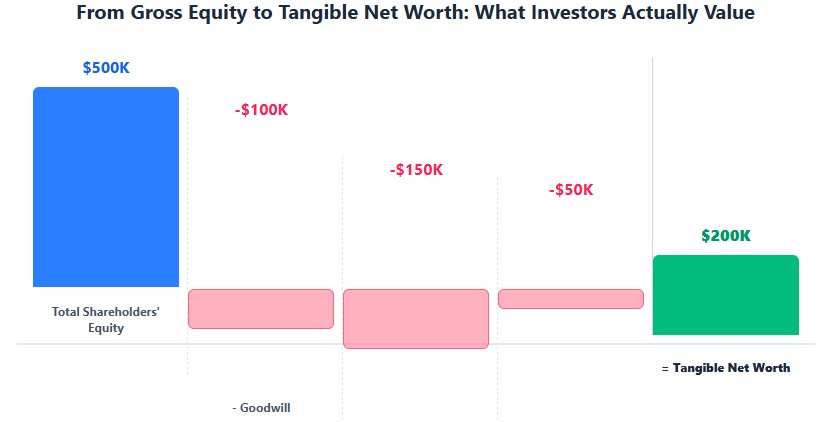

5. Tangible Net Worth

Formula: Total Equity – Intangible Assets (Goodwill, Patents, IP)

What it tells investors: What is the hard value of your company if you shut down today?

Why it matters: In a downturn, intangible assets like “brand value” or “goodwill” can vanish overnight. Lenders and conservative investors focus on tangible net worth to assess downside protection. If your tangible net worth is negative, you are technically insolvent from a liquidation perspective.

Asset Quality: The Hidden Due Diligence Traps

Investors know that not all assets are created equal. They will dig into the quality of your biggest balance sheet items.

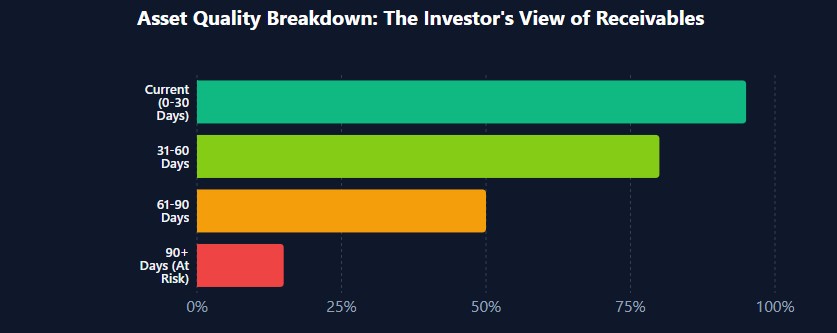

Accounts Receivable (AR) Aging

Having $500K in AR looks great on paper. But if $200K of it is from a client who went bankrupt last month, your assets are overstated.

What Investors Do: They request your AR Aging Report. If more than 10-15% of your receivables are over 90 days past due, they will apply a “haircut” to your valuation, assuming those funds will never be collected. They may also require you to establish a larger Allowance for Doubtful Accounts under GAAP (ASC 326), which reduces your net income.

Inventory Valuation

If you hold physical goods, investors will check your valuation method (FIFO vs. LIFO). More importantly, they look for obsolete stock.

The Fix: Perform a regular inventory write-down. It’s better to take a small hit on your P&L now than to have an investor discover $100K of unsellable product during due diligence and question your entire management team’s competence.

Intangible Assets & Goodwill

Startups often capitalize development costs or assign high values to acquired IP. Investors are skeptical of these numbers.

Reality Check: Unless you have a third-party appraisal or a clear revenue stream attached to that IP, most early-stage investors will value it at zero for their internal models. Don’t build your fundraising case on the back of inflated intangible assets.

Liability Classification: Where Startups Get Caught

Misclassifying liabilities is one of the fastest ways to lose investor trust. It suggests either incompetence or an attempt to hide debt.

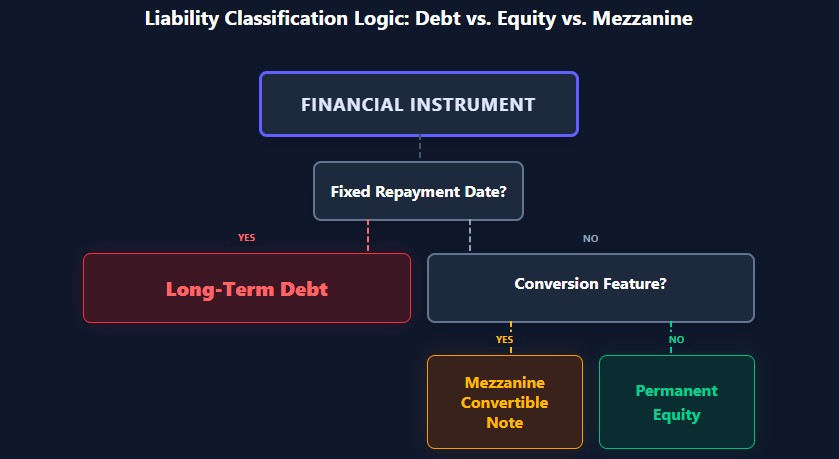

Convertible Notes and SAFEs

Are your SAFEs equity or debt? Technically, SAFEs are not debt, but they are not traditional equity either. Under certain accounting standards (like ASC 480), if there are redemption features, they might need to be classified as liabilities.

Investor Expectation: Clear disclosure in the footnotes. Show exactly how much ownership dilution will occur if all notes and SAFEs convert. Hide this, and you will face intense scrutiny.

Lease Obligations (ASC 842)

Since the implementation of ASC 842, most operating leases must be recorded on the balance sheet as both a right-of-use asset and a lease liability.

The Mistake: Many startups still keep leases off the balance sheet to make their debt levels look lower. Investors using GAAP-compliant reviews will catch this immediately. It’s better to be transparent and show you understand modern accounting standards.

Related-Party Transactions

Did your company borrow money from the founder’s spouse? Did you buy equipment from another company owned by your co-founder? These must be disclosed.

Why it matters: Undisclosed related-party loans look like hidden liabilities or potential fraud. Always document these with formal promissory notes and market-rate interest terms.

Regulatory Compliance: The Silent Deal Killers

Your balance sheet isn’t just for investors; it’s for regulators too. Non-compliance can stall or cancel a funding round.

GAAP vs. Tax Basis Discrepancies

Most small businesses file taxes on a cash basis but need to present GAAP (accrual) financials to investors. The differences—such as deferred revenue or accrued expenses—must be reconciled. If your tax return shows $0 profit but your investor deck shows $1M profit, you need a clear, CPA-verified reconciliation schedule.

State Nexus and Sales Tax Liabilities

If you sell software or products nationwide, do you have sales tax liabilities in states where you have economic nexus? Many startups ignore this until due diligence. Investors will ask for a sales tax exposure analysis. Unpaid sales tax can become a massive, unexpected liability that comes out of the acquisition price or funding amount.

Delaware Franchise Tax

If you are a Delaware C-Corp (as most VC-backed startups are), you must pay annual franchise tax. It’s calculated based on authorized shares or assumed par value. Many founders miscalculate this and end up owing thousands in penalties. Ensure your balance sheet reflects any accrued but unpaid franchise taxes.

How to Prepare Your Balance Sheet for Due Diligence

Don’t wait until the term sheet arrives to clean up your books. Do it now.

- Reconcile All Accounts Monthly: Bank accounts, credit cards, and loan accounts must match your general ledger exactly. No exceptions.

- Audit Your AR Aging: Write off truly uncollectible debts. Establish a realistic allowance for doubtful accounts. Be prepared to explain any large, overdue invoices.

- Review Inventory: Identify obsolete or slow-moving stock and write it down. It’s better to show a lean, efficient inventory list than a bloated one.

- Document All Debt: Gather all promissory notes, loan agreements, and SAFE documents. Ensure they are signed and stored in your data room.

- Disclose Related-Party Transactions: Create a simple schedule listing any transactions with founders, family members, or affiliated entities. Transparency builds trust.

- Hire a CPA for a Review: Before raising a Series A or significant seed round, have a CPA perform a review engagement. It’s cheaper than an audit but provides enough assurance to satisfy most investors.

Case Study: Cleaning Up for a Series A

The Situation: TechFlow Inc., a B2B SaaS company, was raising a $5M Series A. Their initial balance sheet showed a Current Ratio of 0.8 and a Debt-to-Equity ratio of 2.5.

The Problems:

- $200K in receivables were over 120 days old and unlikely to be collected.

- $150K in convertible notes were incorrectly classified as equity instead of mezzanine debt.

- Inventory (for hardware components) included $50K of obsolete parts from a previous product version.

The Fix:

- Wrote off the bad receivables and increased the allowance for doubtful accounts.

- Reclassified the convertible notes correctly and disclosed the conversion terms.

- Written down the obsolete inventory to net realizable value ($0).

The Result: After adjustments, the Current Ratio improved to 1.4 (by removing bad assets) and the Debt-to-Equity ratio clarified the true capital structure. Investors appreciated the transparency and rigorous accounting, leading to a successful close at the target valuation.

Final Thoughts

Your balance sheet is more than a statutory requirement; it’s a story of your company’s financial discipline. In 2026, investors are looking for partners who understand the mechanics of their business, not just the vision. A clean, accurate, and well-analyzed balance sheet signals that you are ready to scale responsibly. Take the time to get it right—it’s the foundation of every successful funding conversation.