Family budgeting for busy dual‑income households (high income, little time)

You’re juggling two careers, keeping up with one or two kids, and bringing in a decent paycheck—yet somehow the money still slips away before you notice. Bills pay themselves, groceries add up, and by the end of the month you’re left wondering where the extra went. It’s not that you’re bad with money. It’s that busy families need a simpler way to keep track without turning budgeting into another chore. This guide skips the generic advice and gives you a clear, repeatable system built for families who earn well but don’t have hours to manage every dollar.

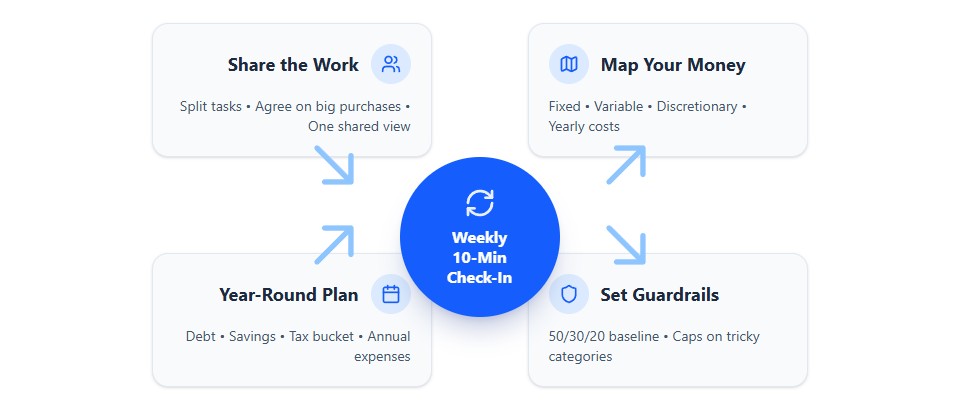

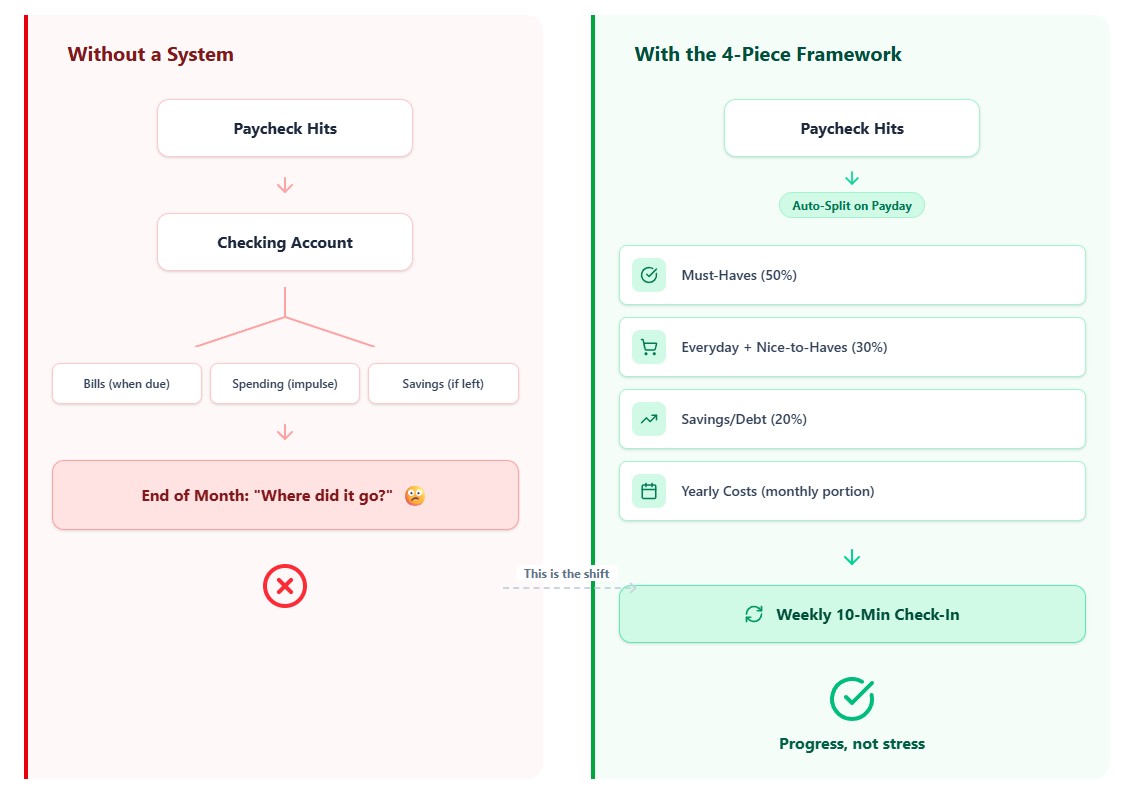

The Busy Family Money System (4‑Piece Budget Framework)

Think of this as your family’s money routine. Set it up once, let the basics run on their own, and step in only when you need to adjust. No spreadsheets required unless you want them.

1. Share the Work & Check In Weekly

Money works better when it’s a team effort. Split tasks based on who has time or interest—not who “should” do it. One person handles the regular bills (mortgage, insurance, subscriptions, childcare). The other keeps an eye on savings, investments, and long-term goals. Both of you agree on big purchases ahead of time. Then, set a quick 10-minute chat once a week—same day, same time. Use one place you can both see: a shared app like Monarch or YNAB, or even a simple Google Sheet. If you can’t both see it, it won’t stick.

2. Map Your Money & Plan for the Big, Infrequent Bills

Start by looking at three months of take-home pay. Sort your spending into three groups: Must-Haves (rent, loans, insurance), Everyday Needs (groceries, gas, utilities), and Nice-to-Haves (dining out, hobbies, extras). Then, spot the bigger bills that don’t hit every month—like car insurance, summer camp, holiday travel, or school fees. Add them up, divide by 12, and set aside that amount each month in a separate savings spot. Use BLS Consumer Expenditure data to get realistic averages for groceries and utilities in your area, so you’re not guessing.

3. Mix Simple Rules With Guardrails for Tricky Spending

Start with a simple 50/30/20 split: about half your income to Must-Haves, 30% to Everyday and Nice-to-Haves, and 20% to savings and debt. You don’t need to track every coffee unless spending feels out of control. For categories where you tend to overspend—like eating out, online shopping, or kids’ activities—set a monthly limit in your banking app. When you hit the limit, pause and reassess. This keeps most of your budget running smoothly while adding gentle boundaries where you need them most.

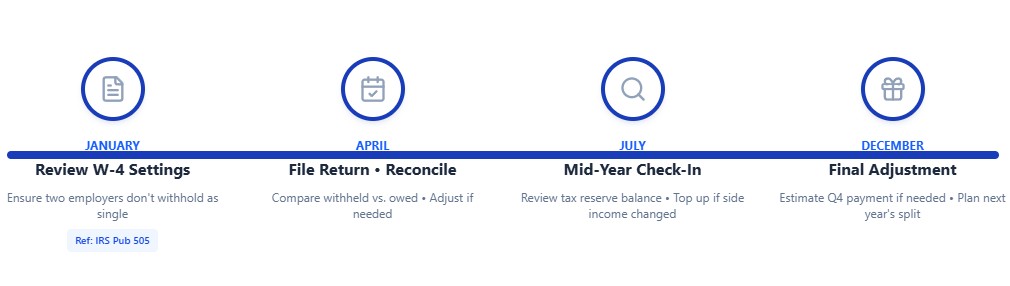

4. Keep a Simple Year‑Round Plan (Including Taxes & Extra Income)

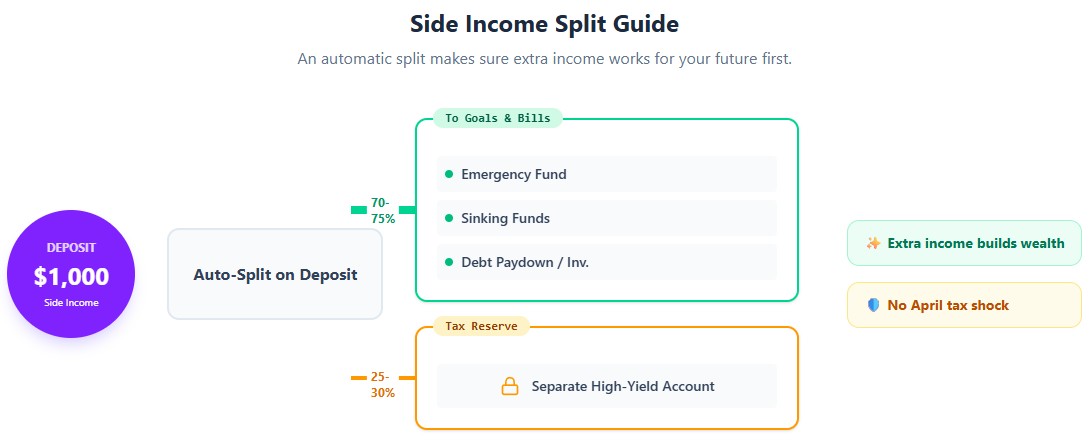

Track four things on one page: your monthly cash flow, what you owe (balances and payoff order), your savings goals (emergency fund, college, retirement), and a calendar of yearly expenses. If you or your partner earn extra money on the side, treat it like part of the plan, not a bonus. Set up an automatic split: most goes to savings or bills, and a portion goes to a separate account for taxes. Once a year, review your W-4 forms so two jobs don’t withhold taxes as if you only have one. IRS Publication 505 walks through how to adjust withholding for dual-income households.

This isn’t a pile of disconnected tips. It’s one simple system that grows with your family. Once it’s set up, your money moves where it needs to go. You just check in to adjust or celebrate progress.

Why busy families with good incomes still feel stuck (and how to fix it)

- Spending grows quietly with income. Raises happen, new subscriptions appear, and suddenly you’re spending more but saving the same. Fix: The 50/30/20 baseline ties your “fun money” to what you actually take home. Any raise automatically boosts savings first, so lifestyle grows on purpose, not by accident.

- Big yearly costs sneak up. Camp fees, holiday travel, and annual premiums can blow a hole in an otherwise calm month. Fix: By setting aside a little each month for these known expenses, they stop feeling like surprises.

- Taxes get tricky with two jobs. When both employers withhold like you’re single, you might overpay all year or owe a surprise bill in April. Fix: A quick annual W-4 check plus a separate tax savings bucket keeps things predictable.

- Side income feels like “extra.” Freelance or gig money often funds impulse buys instead of goals. Fix: An automatic split—most to savings, some to taxes—makes sure extra income works for your future first.

- Too many accounts, too little clarity. Multiple cards, apps, and logins make it hard to see the full picture. Fix: One shared dashboard and a short weekly check-in give you both clarity without daily tracking.

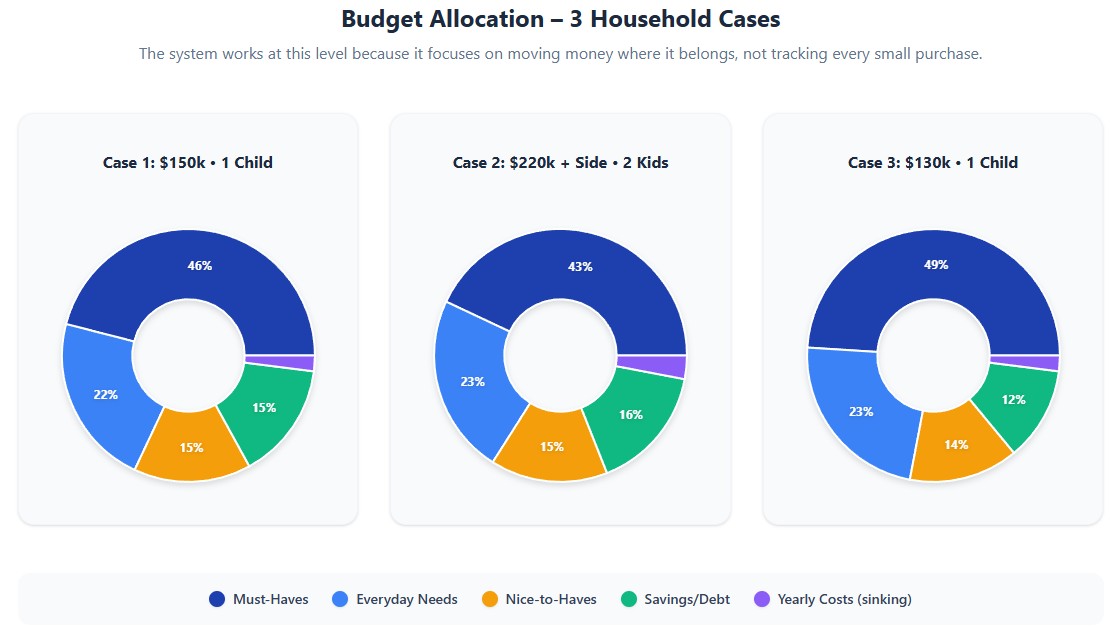

Example budgets for busy dual‑income households

Case 1: $150k Household Income, One Child

Monthly take-home: ~$9,800. Must-Haves: $4,500 (mortgage, childcare, insurance). Everyday Needs: $2,200 (groceries, utilities, gas). Nice-to-Haves: $1,500. Savings/Debt: $1,600. Yearly costs like car registration or holiday gifts average $200/month and go into a separate savings spot. The 4-Piece Framework helps by setting clear limits on dining and weekend trips, while automatically building an emergency fund until it hits $18k, then shifting focus to college savings. Weekly check-ins keep spending on track without micromanaging.

| Category | Amount | % of Take-Home |

|---|---|---|

| Must-Haves | $4,500 | 46% |

| Everyday Needs | $2,200 | 22% |

| Nice-to-Haves | $1,500 | 15% |

| Yearly Costs (saved monthly) | $200 | 2% |

| Savings / Debt | $1,400 | 15% |

Case 2: $220k Household Income + $15k Side Income, Two Children

Monthly base take-home: ~$13,500. Side income splits automatically: most to bills/savings, 25% to a tax savings account. Must-Haves: $5,800 (larger home, two childcare slots, health coverage). Everyday Needs: $3,100. Nice-to-Haves: $2,000. Savings/Investments: $2,600. The system keeps lifestyle growth in check by routing 20% of base pay and 30% of side income directly to savings before it hits your main account. Simple spending limits help manage extracurriculars and weekend trips. The tax account builds about $1,200 per quarter for estimated payments.

| Category | Amount | % of Take-Home |

|---|---|---|

| Must-Haves | $5,800 | 43% |

| Everyday Needs | $3,100 | 23% |

| Nice-to-Haves | $2,000 | 15% |

| Yearly Costs (saved monthly) | $400 | 3% |

| Savings / Investments | $2,200 | 16% |

Case 3: $130k Household Income, One Child

Monthly take-home: ~$8,600. Must-Haves: $4,200. Everyday Needs: $2,000. Nice-to-Haves: $1,200. Savings/Debt: $1,200. Yearly costs: $150/month. Simple spending limits help keep groceries and gas in check. The emergency fund reaches $15k first through automatic transfers, then shifts focus to retirement matching and student loans. The system works at this level because it focuses on moving money where it belongs, not tracking every small purchase.

| Category | Amount | % of Take-Home |

|---|---|---|

| Must-Haves | $4,200 | 49% |

| Everyday Needs | $2,000 | 23% |

| Nice-to-Haves | $1,200 | 14% |

| Yearly Costs (saved monthly) | $150 | 2% |

| Savings / Debt | $1,050 | 12% |

One‑Page family budget planner (copy‑paste version)

Copy this table into Google Sheets or Excel. Set up automatic transfers on payday to match your savings, yearly-cost funds, and tax bucket. Update the numbers during your 10-minute weekly chat. No formulas needed—just compare what you planned to what actually happened. If you overspend in one category for two months in a row, adjust the limit instead of ignoring it.

| Month | Income | Must-Haves | Everyday Needs | Nice-to-Haves | Savings | Debt | Yearly Costs (saved monthly) | Notes |

|---|---|---|---|---|---|---|---|---|

| Jan | ||||||||

| Feb | ||||||||

| Mar | ||||||||

| Apr | ||||||||

| May | ||||||||

| Jun | ||||||||

| Jul | ||||||||

| Aug | ||||||||

| Sep | ||||||||

| Oct | ||||||||

| Nov | ||||||||

| Dec |

Why this system works for busy dual‑income families

The Busy Family Money System keeps things simple: money goes where it needs to go before you even see it. Automation handles deposits, bills, and savings. You only step in to adjust or review. The 4-piece framework grows with your family—new job, new baby, move, or side hustle—because it focuses on setting up good habits, not tracking every penny. It helps avoid tax surprises, keeps spending in check as income rises, and gives both partners a clear view without daily effort.

![]() You don’t need more time. You just need a simple plan that moves your money where it belongs. This is that plan.

You don’t need more time. You just need a simple plan that moves your money where it belongs. This is that plan.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or tax advice. Tax rules and account options vary by state and personal situation. Talk with a qualified CPA or financial planner for guidance tailored to your household. For trusted planning resources, see SEC Investor.gov and CFPB consumer guides.