You don’t need a complicated spreadsheet to know when your money split feels unfair. If one of you is constantly stressed about rent while the other still has room for dinners out and savings, a 50/50 split isn’t working—no matter how “equal” it looks on paper.

How to fairly split bills when partners earn different incomes (without resentment)

This guide is built for couples where take-home pay differs by 30–70%, whether you’re in a city or suburbs, renting or buying, slowly building savings instead of tracking every latte. You’ll get a percentage-based system, a 5-step setup you can finish in a weekend, three flexible models for edge cases, and a single sanity check to keep lifestyle creep from breaking the budget. This isn’t just about “who pays for rent.” It’s about building a transparent system where both of you feel the same level of financial pressure, instead of one person constantly running on fumes.

The Proportional‑Income Split System (3 Models Inside)

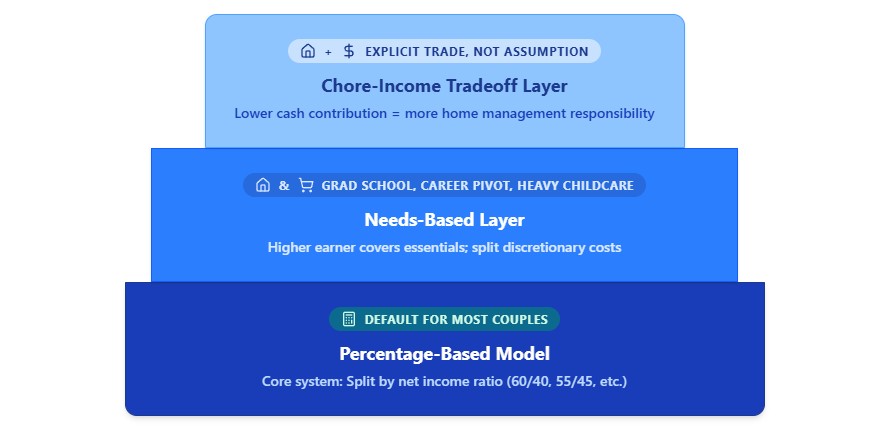

Rather than arguing over 50/50, you match contributions to earning power using actual take-home pay. The system has three layers you can run alone or stack depending on your situation:

- Percentage-Based Model (Core): Each partner pays a share of joint expenses proportional to their net income. Simple division, balanced pressure.

- Needs-Based Layer: The higher earner covers fixed essentials (rent, utilities, basic groceries). Discretionary or “fun” costs get split evenly or by a lighter ratio. Useful during grad school, career pivots, or heavy childcare periods.

- Chore–Income Tradeoff Layer: The lower earner takes a smaller cash cut but explicitly owns more home management (cooking, scheduling, logistics). Treated as a documented trade, not a silent assumption.

Start with the percentage model as your baseline. Add the other two layers only when your cash flow or time commitments shift. These aren’t three competing strategies; they’re three layers of the same system. Whatever combination you choose, write it down. “I thought we agreed…” is a terrible way to start a conversation three months from now.

How percentage-based splitting actually works

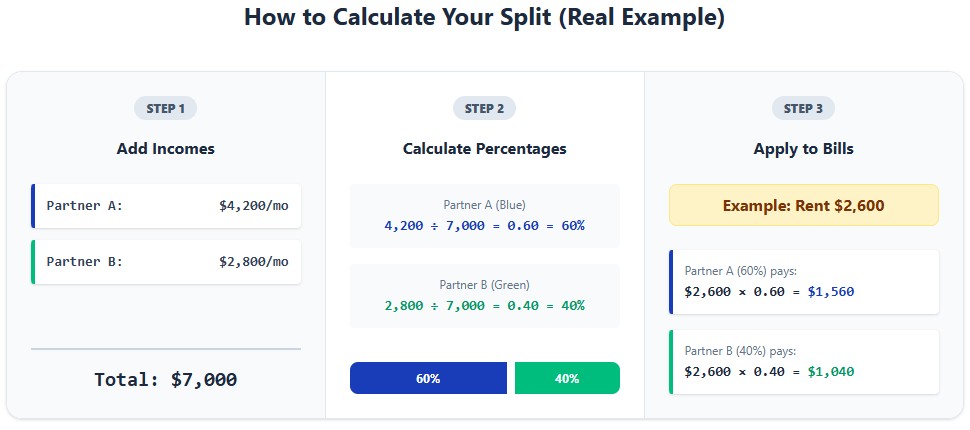

Most people hear “percentage-based” and assume it’s complicated. It’s just one division problem. Out of total household take-home pay, what’s your share?

Example: You bring home $4,200/month. Partner brings home $2,800. Total: $7,000.

- Your share: 4,200 ÷ 7,000 = 60%

- Their share: 2,800 ÷ 7,000 = 40%

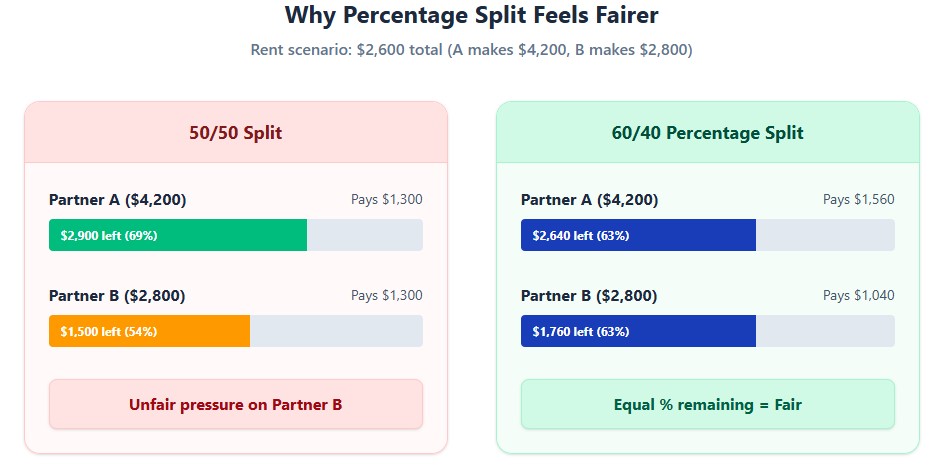

Shared bills get split 60/40. Yes, the higher earner pays more dollars. But after paying their portion, both of you have a similar percentage of income left for food, savings, and actual living.

Splitting rent example: Rent is $2,600. Partner A earns $8,000 net, Partner B earns $5,000 net. Total: $13,000.

- Partner A: 8,000 ÷ 13,000 ≈ 61.5% → $1,599

- Partner B: 5,000 ÷ 13,000 ≈ 38.5% → $1,001

Apply the same ratio to utilities, groceries, shared insurance, streaming, and cleaning supplies. Always use net income. Gross looks bigger on paper but doesn’t reflect what actually hits your checking account after taxes and retirement deductions.

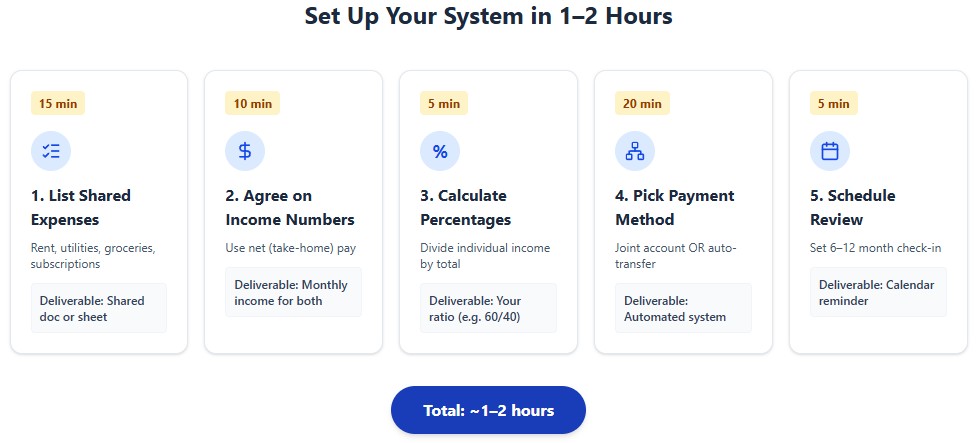

A simple setup you can finish in 1–2 hours

You don’t need to overhaul your finances. This is a straightforward, repeatable process that stops relying on “remember to Venmo later.”

- List shared expenses. Open a doc or sheet. Write down what’s clearly “ours”: rent/mortgage, utilities, internet, groceries, shared subscriptions, joint date-night fund. If something’s borderline (car insurance both drivers use), list it and decide together.

- Agree on income numbers. Use net take-home pay. If income is variable (freelance, tips, commission), average the last 3–6 months. Set a date to recalculate if numbers swing.

- Calculate each person’s percentage. Add incomes together, divide individual income by the total. You’ll get something like 60/40, 68/32, or 55/45. Round to whole numbers if it simplifies tracking without breaking fairness.

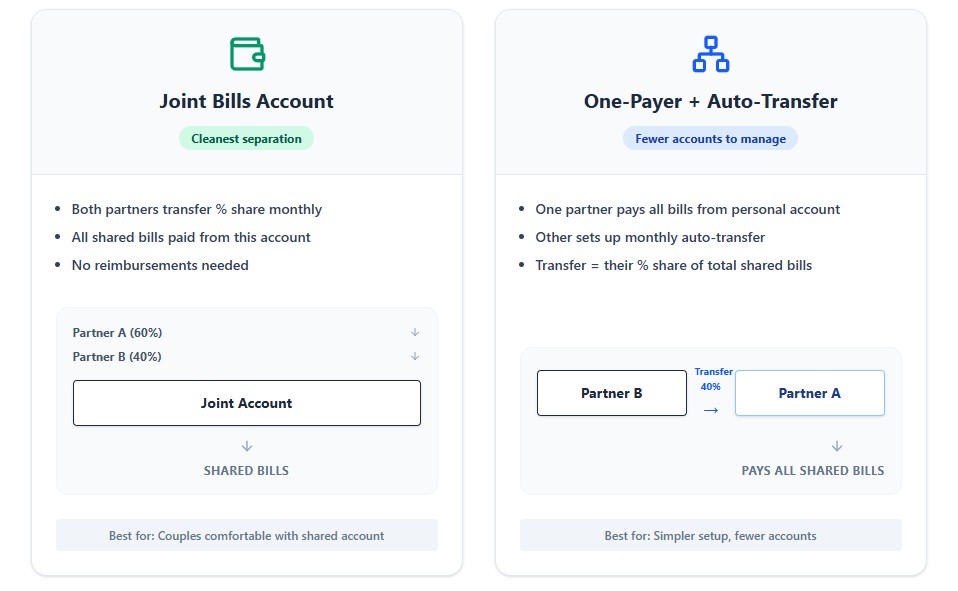

- Pick a payment method that enforces the split. Don’t just agree on paper and pay the old way. Resentment creeps back in. Two options that work:

- Joint “bills” account: Both transfer their percentage of total shared costs into one checking account monthly. All joint bills auto-pay from there.

- One-payer + auto-transfer: One partner pays everything. The other sets up a standing monthly transfer for their calculated share.

- Schedule a quick review. Put a 20–30 minute check-in on the calendar every 6–12 months, or immediately after a raise, job change, or major schedule shift. Update the numbers, ask if the split still feels fair, and adjust. Document the new agreement with a date and next review deadline.

Tools that make this stick

Apps don’t fix fairness, but they do make it visible. Use them to take emotion out of the daily math.

- Splitwise: Track shared purchases and apply custom percentages to each expense automatically.

- Honeydue or a joint banking portal: See balances, upcoming bills, and transaction history in one dashboard.

- Shared spreadsheet: Dead simple. Columns for date, expense, who paid, calculated split, and status. Works best when both partners open it monthly during check-ins.

The tool doesn’t matter. The point is shared visibility. Neither of you should carry the mental ledger alone.

How to avoid resentment when splitting bills with unequal incomes

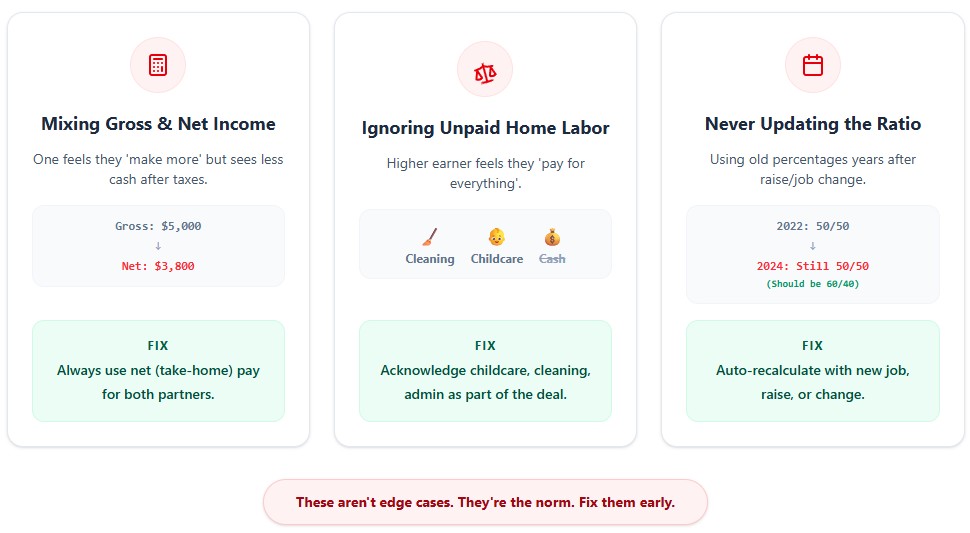

Most money fights aren’t math problems. They’re mismatched expectations and unspoken tradeoffs. These three issues quietly break percentage splits in roughly 80% of couples.

| Problem | What happens | Better approach |

|---|---|---|

| Mixing gross and net income | One person feels they “make more” on paper but see way less cash after taxes and 401(k) deductions | Use net (take-home) for both partners so the split matches actual cash flow |

| Ignoring unpaid home labor | The higher earner feels they’re “paying for everything,” the lower earner feels their time doesn’t count | State it out loud. If one handles more childcare, cleaning, or admin, acknowledge it as part of the arrangement. Adjust the cash split or apply the chore–income tradeoff layer. |

| Never updating the ratio | Someone gets a raise, switches to part-time, or loses a gig, but you keep using old percentages for years | Agree upfront: new job, major raise, or big schedule change = automatic percentage recalculation |

Watch for the subtle trap: lifestyle creep with unequal impact. If the higher earner pushes for a pricier apartment “because we can afford it,” but that really means “I,” the lower earner still ends up stretched thin. Run this sanity check: Can both of us still save a meaningful amount, cover emergencies, and keep some guilt-free spending money after bills? If the answer is no for either of you, your shared expenses are simply too high. No percentage split will fix that.

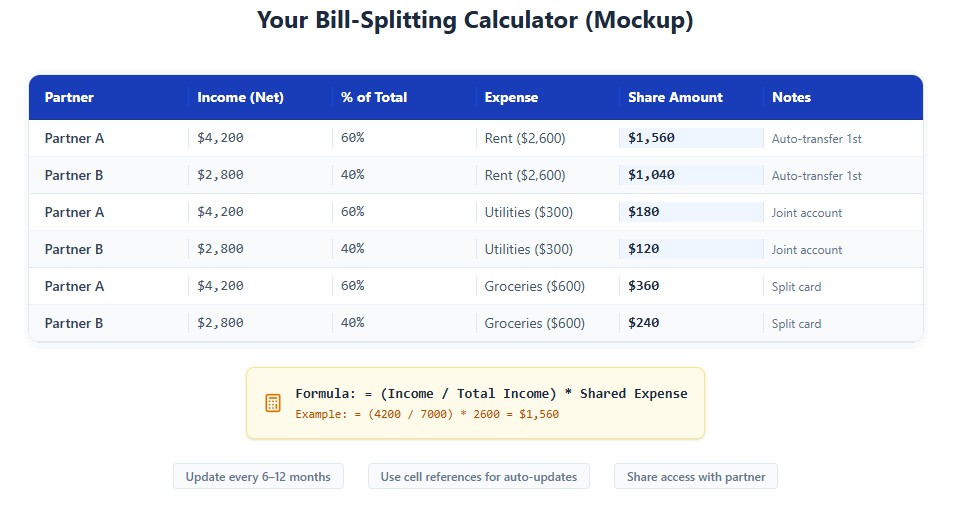

One‑page bill‑splitting calculator (copy‑paste version)

Copy this table into Google Sheets or Excel. Update the numbers every 6–12 months or when a paycheck changes. It keeps the math visible and removes guesswork from monthly transfers.

| Partner | Income (Net) | % of Total | Shared Expense | Share Amount | Notes |

|---|---|---|---|---|---|

| Partner A | $4,200 | 60% | Rent ($2,600) | $1,560 | Auto-transfer 1st of month |

| Partner B | $2,800 | 40% | Rent ($2,600) | $1,040 | Auto-transfer 1st of month |

| Partner A | $4,200 | 60% | Utilities & Internet ($300) | $180 | Joint account payment |

| Partner B | $2,800 | 40% | Utilities & Internet ($300) | $120 | Joint account payment |

| Partner A | $4,200 | 60% | Groceries ($600) | $360 | Split grocery card charge |

| Partner B | $2,800 | 40% | Groceries ($600) | $240 | Split grocery card charge |

Quick formula tip: In Sheets/Excel, calculate the share automatically with = (Income / Total Income) * Shared Expense. Replace static numbers with cell references, and your calculator updates itself every time income or bills change.

Why this system works for couples with unequal incomes

Percentage-based splitting removes the “I’m carrying everything” and “I’m bleeding cash” dynamic by tying contributions directly to take-home reality. The 5-step setup takes a weekend to implement, runs mostly on autopilot, and only needs recalibrating when life actually changes. The three model layers let you adapt without starting over—whether one partner is in school, managing heavy home labor, or navigating variable freelance income. You don’t need perfect numbers. You just need a documented, transparent agreement that treats both incomes fairly. When the math matches your actual cash flow, money stops being a source of friction and starts working as a practical tool for building a life together.

Disclaimer: This article is for general information only and isn’t financial, legal, or tax advice. Rules and best options depend on your country, local laws, and personal situation. Talk to a qualified professional for advice tailored to you.