Sarah just got offered two credit cards. Card A advertises “18% APR.” Card B says “19.25% APR.” She picks Card A because the number is lower, right?

– Wrong.

Card A compounds interest daily. Card B compounds monthly. By the end of the year, Sarah will actually pay more on Card A—even though the advertised rate looks better. She just lost $47 without realizing it.

This is the APR vs. APY trap that catches millions of Americans every year. Banks and lenders use these terms strategically—showing you the number that makes their product look better. But if you don’t understand the difference, you’re making financial decisions blindfolded.

Let’s fix that in the next 10 minutes.

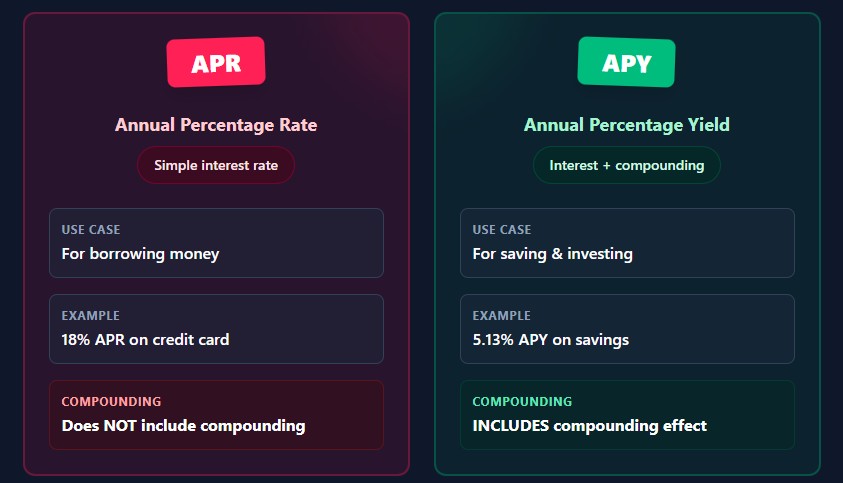

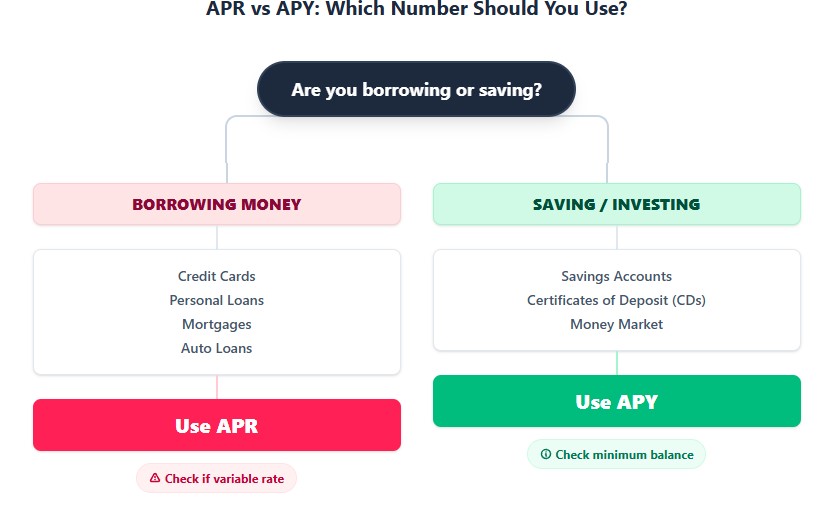

The 30-Second Explanation: APR vs. APY

Think of it this way:

- APR (Annual Percentage Rate) is the sticker price. It’s the simple interest rate without compounding. This is what you see on loan ads and credit card offers.

- APY (Annual Percentage Yield) is the real price. It includes compounding—interest earning interest. This is what you actually pay or earn over a year.

The rule of thumb:

- When you’re borrowing money (loans, credit cards, mortgages), look at APR.

- When you’re earning money (savings accounts, CDs, money market accounts), look at APY.

Why? Because banks want to show you the lower number when you’re borrowing (APR looks smaller than APY) and the higher number when you’re saving (APY looks bigger than APR). It’s marketing, not math.

Real-Life Example #1: The Credit Card Trap

Let’s say you carry a $5,000 balance on a credit card with an 18% APR. You think, “Okay, I’ll pay $900 in interest this year (18% of $5,000).”

But here’s what actually happens:

Credit cards compound interest daily. That means every single day, the bank calculates interest on your balance and adds it. The next day, you’re paying interest on yesterday’s interest.

Let’s do the math:

| Scenario | Calculation | Interest Paid in Year 1 |

|---|---|---|

| Simple interest (no compounding) | $5,000 × 18% | $900 |

| Daily compounding (what credit cards do) | $5,000 × [(1 + 0.18/365)^365 – 1] | $991 |

That’s $91 extra you didn’t budget for. Over three years, it’s $273. Over ten years, if you keep carrying that balance, it’s over $900.

The APY equivalent of that 18% APR is actually 19.72%. That’s the real cost of borrowing.

Real-Life Example #2: The Savings Account Surprise

Now flip it. You’re shopping for a high-yield savings account. Bank A offers 4.50% APY. Bank B offers 4.40% APY. Bank A looks better, right?

Maybe. But check the fine print:

- Bank A: 4.50% APY, but you need to maintain a $10,000 minimum balance. Drop below that, and your rate drops to 0.10%.

- Bank B: 4.40% APY, no minimum balance, compounds daily.

If you only have $8,000 to save, Bank B is actually better—even though the advertised rate is lower. Bank A’s 4.50% APY is a carrot they dangle to get you in the door.

Here’s another twist: two accounts both advertise 4.50% APY. One compounds monthly, the other compounds daily. By the end of the year, you’ll have almost exactly the same amount. But if you withdraw money after 6 months, the daily-compounding account will have paid you slightly more because you earned interest on interest sooner.

The Magic (and Danger) of Compound Interest

Compound interest is Einstein’s “eighth wonder of the world.” It’s how your money grows exponentially—or how your debt spirals out of control.

Here’s how it works with a simple example:

You deposit $10,000 in a savings account with a 5% annual interest rate.

Scenario A: Simple Interest (No Compounding)

Every year, you earn 5% of your original $10,000 = $500.

| Year | Balance | Interest Earned |

|---|---|---|

| Year 1 | $10,500 | $500 |

| Year 2 | $11,000 | $500 |

| Year 3 | $11,500 | $500 |

| Year 10 | $15,000 | $500 |

Scenario B: Annual Compounding

Every year, you earn 5% of your current balance (which includes previous interest).

| Year | Balance | Interest Earned |

|---|---|---|

| Year 1 | $10,500 | $500 |

| Year 2 | $11,025 | $525 |

| Year 3 | $11,576 | $551 |

| Year 10 | $16,289 | $775 |

After 10 years, compounding earned you an extra $1,289. Not life-changing, but it adds up.

Scenario C: Daily Compounding (What Most Savings Accounts Do)

Now the bank calculates interest every single day and adds it to your balance. The next day, you earn interest on yesterday’s interest.

With 5% APR compounded daily, your APY is actually 5.13%.

After 10 years on $10,000:

- Simple interest: $15,000

- Annual compounding: $16,289

- Daily compounding: $16,487

That’s $1,487 extra—almost 10% more than simple interest. And the longer you wait, the bigger the gap gets.

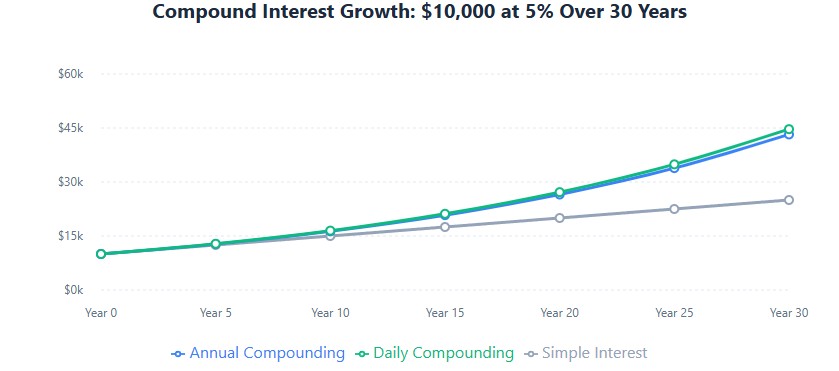

After 30 years on $10,000 at 5%:

- Simple interest: $25,000

- Annual compounding: $43,219

- Daily compounding: $44,677

Now we’re talking. Daily compounding gave you almost $20,000 more than simple interest.

The Formula (Don’t Panic—It’s Simple)

If you want to calculate APY from APR yourself, here’s the formula:

APY = (1 + r/n)^n – 1

Where:

- r = APR as a decimal (5% = 0.05)

- n = number of times interest compounds per year (12 for monthly, 365 for daily)

Example: 6% APR compounded monthly

- r = 0.06

- n = 12

- APY = (1 + 0.06/12)^12 – 1 = 6.17%

That 6% APR is actually 6.17% APY. Not a huge difference, but it matters when you’re comparing offers.

Reverse formula (APY to APR):

APR = n × [(APY + 1)^(1/n) – 1]

You don’t need to memorize these. Just know they exist and use an online calculator when comparing offers.

Real-World Comparison: Where Should You Put $50,000?

Let’s say you have $50,000 to save for a house down payment in 3 years. You’re looking at three options:

| Bank | Advertised Rate | Compounding | Minimum Balance | Actual APY | Balance After 3 Years |

|---|---|---|---|---|---|

| Bank A | 4.50% APR | Daily | $0 | 4.60% | $57,028 |

| Bank B | 4.55% APY | Monthly | $10,000 | 4.55% | $57,095 |

| Bank C | 4.60% APY | Annually | $25,000 | 4.60% | $57,162 |

Bank C looks best on paper (4.60% APY), but you need $25,000 minimum. If you might need access to that money, Bank A or B might be better despite the lower rate.

Bank B advertises 4.55% APY, but if you read the fine print, that rate only applies if you maintain $10,000. Drop below that, and you earn 0.50% APY. That’s a trap.

The lesson: Always read the terms. The advertised rate is just the starting point.

The Hidden Fees That Change Everything

APR on loans isn’t just about interest. It includes certain fees, which is supposed to make it a more accurate picture of cost. But not all fees are included.

What’s Included in APR:

- Interest rate

- Origination fees (for personal loans)

- Discount points (for mortgages)

- Mortgage insurance (if required)

- Certain closing costs

What’s NOT Included in APR:

- Appraisal fees

- Title insurance

- Notary fees

- Late payment penalties

- Prepayment penalties (sometimes)

So two lenders might both advertise 7% APR on a mortgage, but one charges $3,000 in origination fees and the other charges $0. The APR is the same, but the real cost is very different.

Always ask: “What’s the total cost of this loan over the full term, including all fees?”

Credit Card APR: The Fine Print Nightmare

Credit cards are where APR gets really tricky. Here’s what you need to know:

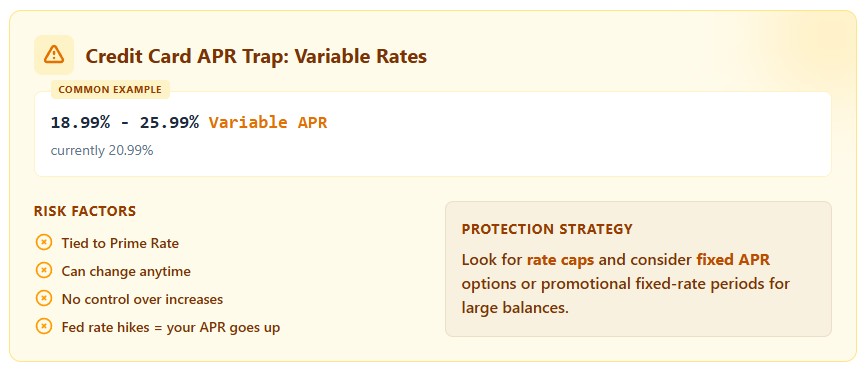

Variable vs. Fixed APR

Most credit cards have variable APR, which means it can change. It’s usually tied to the Prime Rate (what banks charge their best customers) plus a margin.

Example: “18.99% – 25.99% Variable APR, currently 20.99%”

That “currently” is doing a lot of work. If the Fed raises rates, your APR goes up. If they cut rates, it goes down. You have no control over this.

Purchase APR vs. Cash Advance APR

Your card might have different APRs for different types of transactions:

- Purchase APR: 18.99% (what you pay when you buy something)

- Cash Advance APR: 25.99% (what you pay when you withdraw cash from an ATM)

- Balance Transfer APR: 0% for 12 months, then 20.99%

Never use a credit card for a cash advance unless it’s a true emergency. The APR is higher, there’s usually a fee (3-5% of the amount), and interest starts accruing immediately—no grace period.

Penalty APR

Miss a payment or go over your credit limit, and your APR can jump to 29.99% or higher. This is the penalty APR, and it can stay in effect for six months or more even after you get back on track.

Introductory APR

Many cards offer 0% APR for 12-18 months on purchases or balance transfers. This is a great deal—if you pay off the balance before the intro period ends. If you don’t, you’ll be hit with the regular APR (often 20%+) on the remaining balance.

The trap: Some cards defer interest during the intro period. If you don’t pay off the full balance by the end of the intro period, you owe interest on the original balance, not just what’s left. This is called “deferred interest,” and it’s brutal.

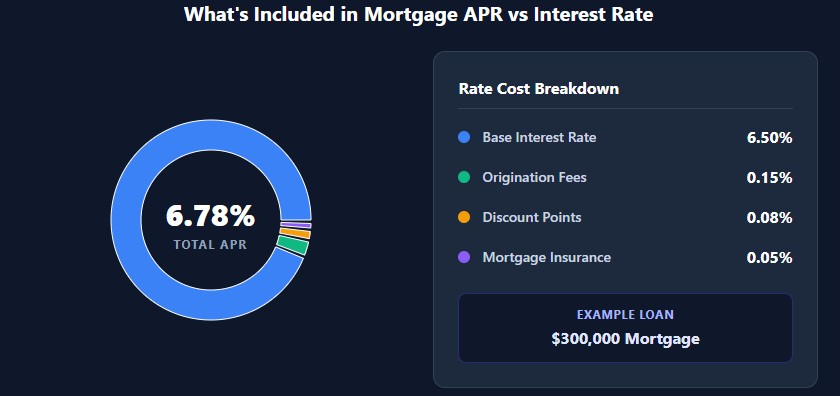

Mortgage APR: Why It’s Higher Than Your Interest Rate

When you get a mortgage, you’ll see two numbers:

- Interest rate: 6.50%

- APR: 6.78%

Why is the APR higher? Because it includes fees like origination charges, discount points, and mortgage insurance. The APR is supposed to give you a more complete picture of the loan’s cost.

Example: $300,000 mortgage

| Lender | Interest Rate | Points | Origination Fee | APR | Monthly Payment |

|---|---|---|---|---|---|

| Lender A | 6.50% | 0 | $3,000 | 6.78% | $1,896 |

| Lender B | 6.75% | 0 | $0 | 6.75% | $1,945 |

Lender A has a lower interest rate but charges $3,000 in fees. Lender B has a higher rate but no fees. Which is better?

If you plan to stay in the house for 30 years, Lender A saves you money overall. If you’ll sell in 5 years, Lender B is better because you won’t recoup the $3,000 in fees.

The lesson: APR helps you compare loans, but you also need to consider how long you’ll keep the loan.

The 5 Questions to Ask Before You Sign Anything

Before you take out a loan or open a savings account, ask these questions:

- Is this APR or APY? Make sure you’re comparing apples to apples.

- How often does it compound? Daily, monthly, annually? More frequent compounding means higher APY (good for savings, bad for loans).

- Is the rate fixed or variable? If it’s variable, what’s it tied to? How often can it change? Is there a cap?

- What fees are included in the APR? For loans, ask for a complete list of all fees. For savings accounts, ask about maintenance fees, minimum balance requirements, and withdrawal penalties.

- What’s the total cost over the full term? For a loan, ask: “If I make all payments on time, how much will I pay in total, including interest and fees?” For a savings account, ask: “If I leave this money here for X years, what will the balance be?”

Quick Reference: APR vs. APY Cheat Sheet

| Product | What to Look For | Why | Red Flags |

|---|---|---|---|

| Credit Cards | APR | Shows the cost of carrying a balance | Variable APR without a cap, high penalty APR, deferred interest promos |

| Personal Loans | APR | Includes fees, so it’s the true cost | Origination fees not disclosed, prepayment penalties |

| Mortgages | APR | Includes closing costs and points | Huge gap between interest rate and APR (means high fees) |

| Auto Loans | APR | Standardized comparison metric | Long loan terms (72+ months) with high APR |

| Savings Accounts | APY | Shows what you’ll actually earn with compounding | High minimum balance requirements, tiered rates |

| CDs (Certificates of Deposit) | APY | Shows total return over the term | Early withdrawal penalties, bump-up rate restrictions |

| Money Market Accounts | APY | Shows actual earnings with compounding | High minimum balance, limited transactions |

FAQ: Real Questions People Ask

Q: Can APR ever be higher than APY?

A: No. APY always includes compounding, so it’s always equal to or higher than APR. If you see an ad where APR looks higher, they’re either making a mistake or trying to confuse you.

Q: Why do credit cards use APR instead of APY?

A: Because APR looks lower, and banks want you to borrow. If they showed you the APY (the real cost), it would scare you off. It’s required by law (Truth in Lending Act) to show APR for loans.

Q: Is daily compounding really that much better than monthly?

A: On small amounts over short periods, no. On $100,000 over 20 years at 5%, daily compounding earns you about $1,500 more than monthly. It adds up.

Q: What’s a good APR for a credit card?

A: As of 2026, the average credit card APR is around 22-24%. Anything below 18% is considered good. If you have excellent credit, you might qualify for 15-17%.

Q: What’s a good APY for a savings account?

A: High-yield savings accounts in 2026 are offering 4-5% APY. Traditional bank savings accounts offer 0.01-0.50% APY. Always compare to inflation—if inflation is 3% and your savings earn 2%, you’re losing purchasing power.

Q: Can I negotiate APR?

A: Sometimes. If you have good credit and a long relationship with your bank, call and ask for a lower rate. It works more often than you’d think, especially for credit cards.

Q: What’s the difference between nominal rate and effective rate?

A: Nominal rate is the stated rate (APR). Effective rate is the actual rate after compounding (APY). They’re the same concepts, just different terminology.

Your Action Plan: What to Do Right Now

- Check your credit cards. Log in and look at your APR. Is it variable? What’s the penalty APR? If you’re carrying a balance, calculate how much you’re really paying using the APY formula.

- Review your savings accounts. What APY are you earning? If it’s below 4%, you’re leaving money on the table. Shop around for high-yield savings accounts.

- Before your next loan or credit card application, compare at least 3 offers. Make sure you’re comparing APR to APR (for loans) or APY to APY (for savings). Don’t just look at the advertised rate—read the terms.

- Use an online calculator. Before signing anything, plug the numbers into an APR/APY calculator. See what you’ll actually pay or earn over the full term.

- Ask questions. If a bank rep can’t clearly explain the difference between APR and APY, or if they get defensive when you ask about fees, walk away. You deserve transparency.

The Bottom Line

APR and APY aren’t just accounting terms—they’re the difference between keeping your money and losing it to interest. Banks count on you not understanding these concepts. They use confusing jargon, hide fees in fine print, and advertise the number that makes their product look best.

But now you know better. You know that APR is the sticker price and APY is the real price. You know how compounding works and why it matters. You know what questions to ask and what red flags to watch for.

The next time you see an ad for “5% APR!” or “4.5% APY!”, you won’t just glance at the number and move on. You’ll dig deeper. You’ll compare. You’ll calculate.

And that’s how you stop being a victim of financial marketing and start making decisions that actually build wealth.