This is not a brand manifesto. It is a financial instrument built to pass SBA underwriting, commercial lender scrutiny, and operational stress-testing. If your plan reads like a menu description, it will be rejected. If it reads like a P&L forecast with embedded cost controls, you will get funded. The following structure uses Brimstone Burger Co. as a live case study. Every metric, cost line, and assumption is pulled from actual Columbus, Ohio commercial data, with typical US ranges noted for adaptability. Copy the framework. Swap the numbers. Keep the math honest.

Table of Contents: Classic Business Plan Structure

- Executive Summary & Capital Needs

- Company Overview & Concept

- Market & Customer Analysis

- Management Team & Organizational Structure

- Menu Engineering & Unit Economics

- Operations, Lease & Throughput

- Marketing & Customer Acquisition

- Financial Projections & Break-Even

- Risk Management & Mitigation

- Appendix & Documentation Checklist

– Legal entity name and structure (LLC/C-Corp)

– Location with nexus details

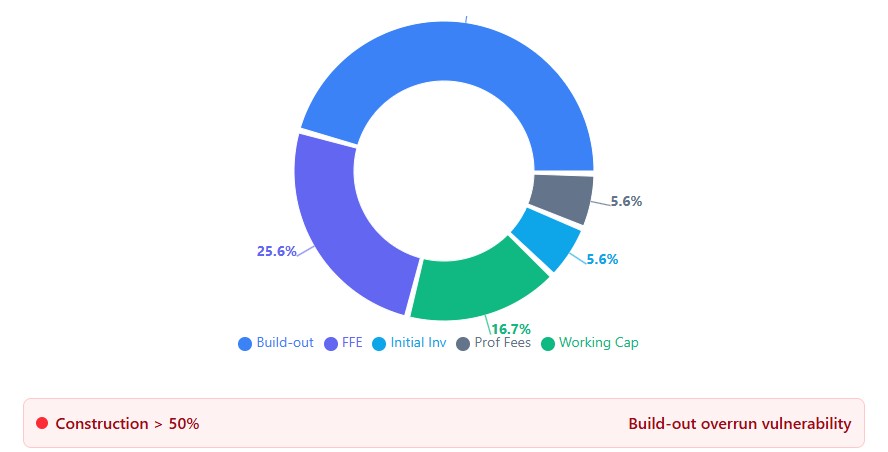

– Total capital required + founder equity injection %

– Loan instrument terms (SBA 7a, conventional, etc.)

– Year 1 revenue target + net margin projection

– Cash-flow break-even month

1. Executive Summary & Capital Needs

Lenders scan this block in under 30 seconds. They look for three things: skin in the game, a clear capital stack, and a defensible path to cash-flow break-even. Lead with the numbers. Leave the origin story for the website.

✓ Owner equity injection ≥10-20% (SBA minimum)

✓ Clear use-of-funds breakdown (build-out, FF&E, working capital)

✓ Realistic Year 1 revenue tied to seat count and turns

✓ Break-even month ≤6 for fast-casual concepts

✗ Vague phrases like “unique concept” or “high demand area”

✗ Missing payroll tax burden in labor projections

✗ No contingency buffer in startup costs

Capital Stack: Brimstone Burger Co. (Columbus, OH Example)

| Line Item | Amount | Structure / Terms |

|---|---|---|

| Company | Brimstone Burger Co., LLC | Fast-casual premium smashburgers + local craft draft beer. |

| Location | Short North Arts District, Columbus, OH | High foot traffic, dense residential and commercial mix. Typical rent range Midwest: $28-42/sq ft NNN. |

| Founder Equity | $75,000 | 16.7% injection. Held in dedicated business account prior to close. |

| SBA 7(a) Loan | $375,000 | 85% funded. 10-year term, estimated 8.5% fixed rate, 12-month payment holiday during build-out. |

| Year 1 Target | $1,150,000 Gross Revenue | 14.2% Net Restaurant Operating Profit (NROP). Cash-flow break-even by Month 4. |

Company: [Your Brand], [LLC/C-Corp]

Concept: [Service style] + [core product] + [differentiator]

Location: [Neighborhood], [City, State] — [foot traffic note]

Founder Equity: $[amount] ([%] injection)

Loan Request: $[amount] via [instrument] at [rate]% [term]-year

Year 1 Target: $[revenue] Gross, [margin]% Net, break-even Month [X]

2. Company Overview & Concept

This section answers: What are you selling, to whom, and why will they pay? Keep it tight. Lenders do not fund “vibes.” They fund clear positioning with defensible margins.

Concept Breakdown

- Service Model: Fast-casual counter service. No full-service table turns. Average dwell time: 45 minutes vs. 90 minutes industry average.

- Core Product: Premium smashburgers (80/20 proprietary blend) + local craft draft beer. High perceived value, controllable COGS.

- Target Daypart Mix: 40% lunch, 45% dinner, 15% late-night/weekend. Lunch drives volume; dinner drives ticket size.

- Off-Premise Strategy: 35% of sales via takeout and delivery. Menu priced 18% higher on third-party apps to offset commission drag.

Service Model: [Fast-casual / QSR / Full-service] + [avg dwell time target]

Core Product: [Primary SKU] + [margin driver: beverage/alcohol/add-ons]

Daypart Mix: [Lunch %] / [Dinner %] / [Other %]

Off-Premise Cap: [%] max to protect blended margin

3. Market & Customer Analysis

Most restaurant plans fail here by writing “everyone loves burgers.” Lenders want to see you understand your trade area, your competition, and your realistic capture rate. This is not a census report. It is a revenue justification.

Trade Area & Demand Validation

| Metric | Brimstone Example (Columbus) | Typical Mid-Market US Range |

|---|---|---|

| Primary Trade Area Radius | 1.5 miles | 1-3 miles for fast-casual |

| Daytime Population (PTA) | 12,400 | 8k-25k depending on urban density |

| Median Household Income | $68,200 | $55k-$95k for target fast-casual demographics |

| Competitor Count (Direct) | 4 smashburger concepts within 1.5 mi | 3-8 direct competitors in viable urban nodes |

| Estimated Market Share Capture (Year 1) | 2.1% of lunch traffic, 1.4% of dinner | 1-3% is realistic for new entrants without brand equity |

Customer Persona (Primary): “Office Olivia,” 28-45, works within 0.5 miles, values speed and quality over lowest price, spends $16-22 on lunch, orders via app 2-3x/week. We target her with pre-order functionality and a loyalty program that rewards frequency, not just spend.

Trade Area Radius: [X] miles

Daytime Population: [number] — source: [Census/ESRI/Placer]

Median Income: $[amount] — validates price point

Direct Competitors: [count] within [radius] — list top 3 by Google rating

Realistic Capture Rate: [X]% of [lunch/dinner] traffic — based on [seats x turns / PTA]

Primary Persona: [Name], [age range], [job context], [spend range], [ordering habit]

4. Management Team & Organizational Structure

Lenders fund people, not concepts. If your team has no restaurant experience, say so—and explain how you are mitigating that risk (advisor, hired GM, fractional CFO). Do not pad resumes. Be specific about roles, compensation, and escalation paths.

Core Team & Compensation

| Role | Experience Highlight | Compensation Structure |

|---|---|---|

| Founder / CEO | 7 years multi-unit QSR operations; P&L responsibility for $4.2M annual revenue portfolio. | Draw-only Year 1 ($3,000/mo max). Salary begins Month 7 if NROP >12% for 2 consecutive months. |

| General Manager (Hired) | 5 years BOH/FOH leadership at regional fast-casual brand. ServSafe certified. | $65,000/year + 2% of NROP above 14% threshold. Bonus paid quarterly. |

| Fractional CFO (Contract) | CPA with 12 restaurant client engagements. Specializes in SBA loan compliance. | $800/month retainer. Scope: monthly P&L review, sales tax filing, cash flow forecast. |

| Head Cook (BOH Lead) | Culinary school + 3 years line cook at high-volume burger concept. | $22/hour + quarterly retention bonus ($500) after 6 months. |

Gap Mitigation: Founder lacks Ohio-specific permitting experience. Mitigation: retained local restaurant attorney ($150/hr, 10-hour monthly cap) for license applications and health inspection prep.

For each key role, include:

– Name (or “To Be Hired”)

– 1-2 line experience highlight (quantify: “$X revenue”, “X units”, “X years”)

– Compensation: base + variable + triggers

– Gap? → Mitigation: [advisor/consultant/training plan]

5. Menu Engineering & Granular Unit Economics

Profit lives or dies at the plate level. Lenders do not care if your burger wins local awards. They care if your blended food cost sits at 26% or 34%. You must engineer the menu to subsidize high-COGS proteins with high-margin ancillary items. Draft beer, soda, and add-ons are your margin buffer.

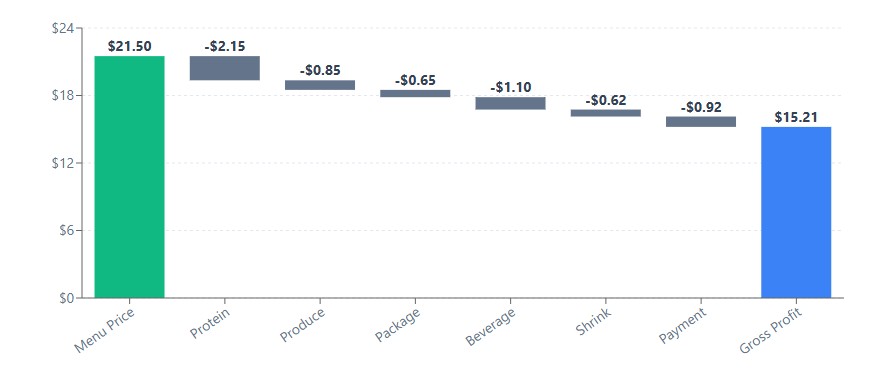

SKU Teardown: The Brimstone Combo

| Component | Cost | Notes |

|---|---|---|

| Menu Retail Price | $21.50 | Final ticket average. |

| Protein & Dairy | $2.15 | 80/20 beef patty, 2 slices American cheese, portion waste factored. |

| Produce & Dry Goods | $0.85 | Brioche bun, house sauce, pickles, 5oz fresh-cut potatoes. |

| Packaging / Disposables | $0.65 | Custom clamshell, liner, paper bag, napkins (accounts for 35% off-premise mix). |

| Beverage Pour Cost | $1.10 | 16oz craft draft pour, keg cost amortized + line loss allowance. |

| Total Landed COGS | $4.75 | |

| Gross Margin | $16.75 (77.9%) | Combo structure protects blended COGS at 26% when averaged with lower-margin a la carte items. |

Menu Price: $[amount]

Protein Cost: $[amount] — [supplier, portion size, waste factor]

Produce/Dry Goods: $[amount] — [list key components]

Packaging: $[amount] — [include if off-premise mix >25%]

Beverage Pour (if applicable): $[amount] — [keg cost / pours + loss allowance]

Total COGS: $[sum]

Gross Margin: $[price – COGS] ([%])

Blended COGS Target: [26-28%] — achieved by [high-margin item] subsidizing [high-cost item]

Reality Check: If your blended COGS exceeds 30% without a clear beverage strategy, your prime cost will bleed. Lock pour costs at 18-22% for draft. Keep food at 26-28%. Weigh every ounce during prep audits. Do not guess.

6. Operations, Lease & Throughput

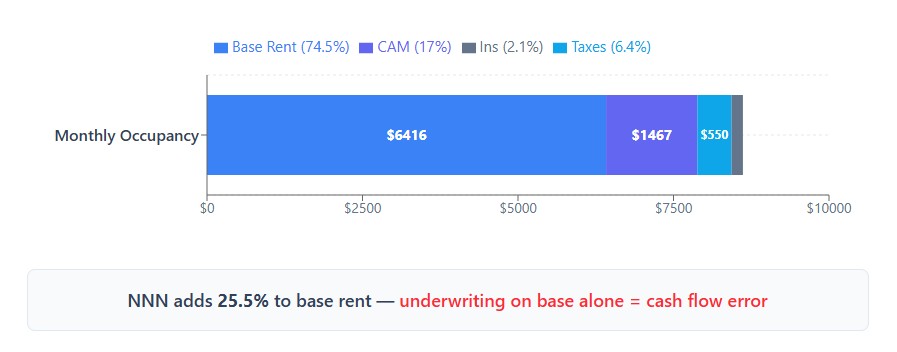

US restaurants lease on a Triple Net (NNN) basis. Base rent covers only 60-70% of your actual monthly occupancy cost. Underwriting on base rent alone means missing cash flow targets by Month 3 and defaulting on the lease.

Lease Terms & Monthly Burden (Columbus Example)

| Line Item | Annual / One-Time | Monthly Equivalent |

|---|---|---|

| Base Rent ($35/sq ft) | $77,000 | $6,416 |

| NNN (CAM, Taxes, Insurance) | $26,400 | $2,200 |

| Total Monthly Rent Burden | $103,400 | $8,616 |

| Security Deposit | $17,232 | Due at lease execution (First + Last month). |

| Tenant Improvement (TI) Allowance | $50,000 credit | Applied to Months 2-3 rent. Offsets Type 1 hood vent upgrades. |

Typical NNN Range US Mid-Market: $8-18/sq ft annually. Coastal markets: $15-35/sq ft. Always request a 3-year NNN history from the landlord before signing.

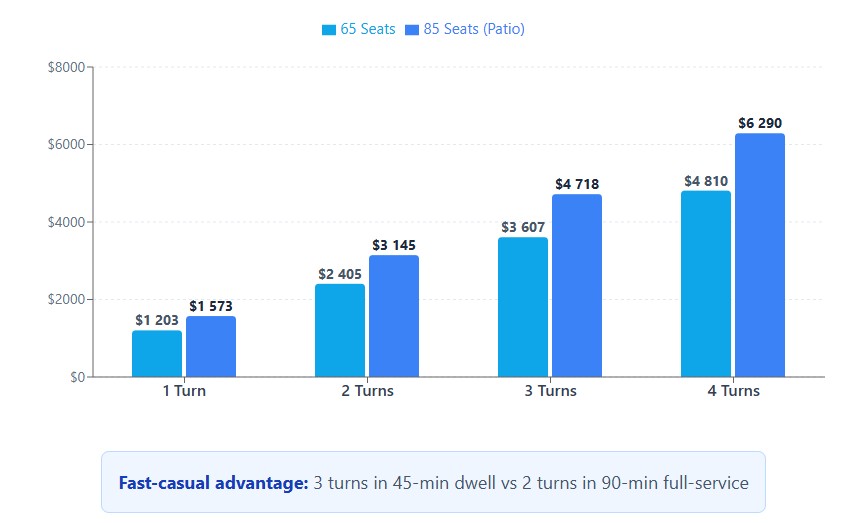

Capacity, Throughput & RevPASH

- Physical Capacity: 65 interior seats, 20 seasonal patio seats.

- Sales Mix: 65% Dine-In / 35% Off-Premise (Takeout + Third-Party Delivery).

- Peak Dinner Shift (6 PM – 9 PM): Target of 3 full table turns.

- Max Nightly Dine-In Gross: 65 seats × 3 turns × $18.50 avg ticket = $3,607 (Fri/Sat peak).

- RevPASH (Revenue Per Available Seat Hour): Target $4.20 during peak hours. Calculated as peak revenue ÷ (seats × peak hours).

1. Covers: [target] per day → [actual] → variance %

2. Avg Ticket: $[target] → $[actual] → variance %

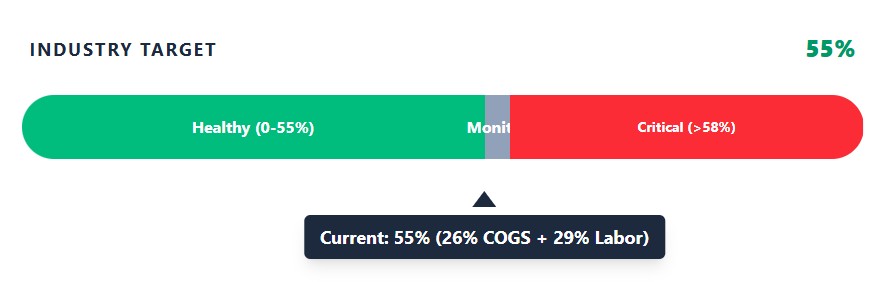

3. Prime Cost: [55% target] → [actual %] → action trigger if >58%

4. RevPASH (Peak): $[target] → $[actual] → adjust staffing if -15%

5. Cash Balance: $[minimum buffer] → alert if <21 days of OpEx

7. Marketing & Customer Acquisition

Restaurants do not scale on boosted posts. They scale on foot traffic, local SEO dominance, and repeat visit frequency. Third-party delivery apps drain 25-30% margin. Use them for acquisition, then funnel customers to direct ordering with a loyalty discount.

Acquisition Funnel & Economics

| Channel | Strategy | Target Metric | Margin Impact |

|---|---|---|---|

| Pre-Opening Email Capture | Site landing page + local geo-fenced ads. Offer: Free draft on opening week. | 2,500 opt-ins | $0 CAC. Direct email ownership. |

| Grand Opening (Days 1-14) | Local radio, neighborhood canvassing, influencer tastings (product only, no cash). | 1,200 covers in 14 days | High volume, low margin. Acceptable for traffic injection. |

| Third-Party Delivery | UberEats/DoorDash used strictly for new zip code penetration. | 15% of total sales max | -28% commission drag. Menu marked up 18% to offset. |

| Direct Ordering + Loyalty | Toast native ordering + SMS opt-in. 5% discount on direct orders. | Convert 30% of 3P customers to direct within 60 days | Recovers full margin. LTV increases 2.1x after 3 visits. |

Channel: [Name]

Strategy: [1-line tactic]

Target Metric: [quantifiable goal]

CAC Estimate: $[amount] or $0 if organic

Margin Impact: [+X% / -Y%] — explain offset if negative

Cap Rule: [e.g., “3P sales ≤20% of total”]

Rule: Third-party delivery is a customer acquisition cost, not a revenue channel. If 3P volume exceeds 20% of total sales, unit economics collapse. Cap it. Redirect to direct.

8. Financial Projections & Break-Even

Forget hockey-stick revenue charts. Manage to the daily cover count required to keep the doors open. If you do not know your survival number, you are gambling, not operating.

Monthly Break-Even Math

Fixed Monthly Overhead: $18,500

(Includes $8,616 NNN rent, GM salary allocation, $800 liability insurance, $1,500 baseline utilities, $595 software stack.)

Variable Contribution Margin: 45% of gross sales.

(After deducting actual food costs and hourly labor, $0.45 of every dollar covers fixed costs and profit.)

Break-Even Revenue: $18,500 ÷ 0.45 = $41,111 per month.

$41,111 ÷ 30 days = $1,370 per day.

At an $18.50 blended average ticket, you need exactly 74 covers per day.

Capturing 1.5 lunch turns and 2 dinner turns at 30% physical capacity makes this achievable by Month 4.

FILL-IN YOUR NUMBERS:

Fixed Monthly Overhead: $[sum of rent, salaries, insurance, utilities, software]

Contribution Margin: [X]% — calculate as (Revenue – COGS – Hourly Labor) / Revenue

Break-Even Revenue: [Fixed Costs] ÷ [Contribution Margin % as decimal]

Daily Target: [Monthly BE] ÷ 30

Covers Needed: [Daily Target] ÷ [Your Avg Ticket]

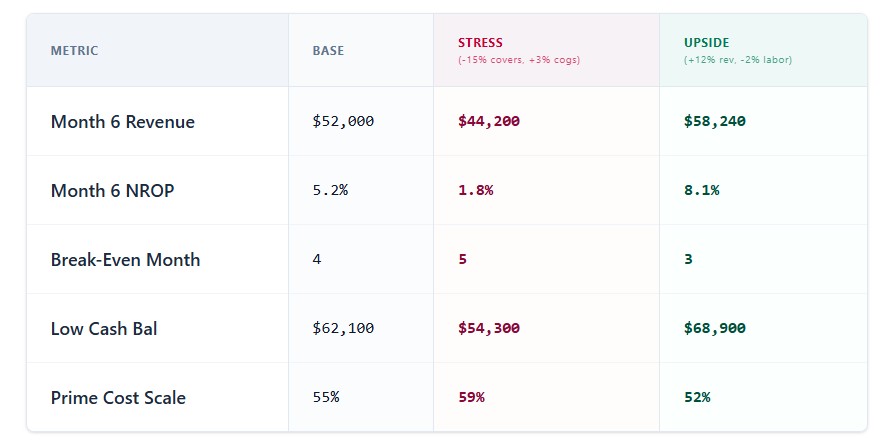

36-Month P&L Snapshot (Text Summary)

Full model available in downloadable template. Key trajectory:

- Months 1-3: Revenue ramp from $18k to $52k/month. Net loss as marketing spend peaks. Cash burn covered by working capital reserve.

- Months 4-6: Break-even achieved. Prime cost stabilizes at 54-56%. NROP turns positive (3-5%).

- Months 7-12: Revenue averages $98k/month. NROP targets 12-14%. Founder draw begins. Loan payments commence Month 13.

- Year 2: Modest menu price increase (3.5%) + catering program launch. Target NROP: 16-18%.

- Year 3: Evaluate second unit. Reinvest 50% of retained earnings; refinance SBA loan if rates improve.

✗ Revenue growth >25% MoM without marketing spend increase → unrealistic

✗ COGS flat at 24% while scaling → ignores volume discount phase-in

✗ Labor % drops below 25% at scale → understaffing risk, quality erosion

✓ Prime cost tracked weekly with trigger actions at 56% and 58%

✓ Scenario tabs: Base, Stress (+10% COGS, -15% covers), Upside (+5% ticket)

✓ Cash flow statement shows loan payment start date and reserve buffer

9. Risk Management & Mitigation

Every restaurant faces predictable failures. Staff walk out during peak. Grease traps back up. Utility rates spike. Health inspectors find a missing thermometer. Price these risks into your operating model or you will not survive Year 1.

Risk Matrix & Operational Controls

| Risk | Probability | Financial Impact | Mitigation |

|---|---|---|---|

| High Staff Turnover (BOH) | High | +$3,200/month in retraining + overtime | $19/hr base + clear tip pool distribution. Cross-train prep to line. No-poach clauses with local culinary schools. |

| Food Safety Violation | Low-Medium | $1,500 fine + 3-day closure = $12,000 lost revenue | Daily temp logs. Digital HACCP tracking. Manager on duty holds ServSafe certification. Weekly mock health inspections. |

| Utility Rate Spike | Medium | +$400-$600/month HVAC/gas fluctuation | Energy audit during build-out. LED retrofits. Demand-controlled hood ventilation. Lock 12-month utility hedging where available. |

| Delivery App Commission Increase | Medium | Margin compression on 3P orders | Menu price parity policy. Push direct ordering via receipt QR codes. Cap 3P at 20% of sales. |

10. Appendix & Required Documentation Checklist

Lenders do not accept projections without documentation. Before submitting the plan, assemble the following documents in a single, organized directory. Use consistent file naming: YYYY-MM-DD_DocName_Version. Do not rely on cloud links; financial institutions block external URLs for security compliance.

| Document | Purpose | Submission Requirements |

|---|---|---|

| Stamped Architecture & MEP Plans | Confirms zoning, ADA compliance, and construction estimate accuracy. | PDF + CAD files, engineer/architect seal, dated within 60 days. |

| Equipment Vendor Quotes | Validates FF&E line items. Lenders reject estimates without current pricing. | Itemized SKUs, delivery timelines, payment terms (Net 30/50). |

| Executed Letter of Intent (LOI) | Locks lease terms, NNN breakdown, and TI allowance. | Signed copy with landlord contacts and effective dates. |

| Liquor License Application Receipt | Proves regulatory progress. Delayed licenses delay openings. | State tracking number, fee receipt, current status. |

| 36-Month Pro Forma P&L | Core financial model. Must include Base, Stress, and Upside scenarios. | Excel/Google Sheets with unlocked formulas for lender audit. |

| HACCP & Food Safety Plan | Required for county health permits. Missing documents stall inspections. | Allergen matrix, temperature logs, cooling protocols, ServSafe certificates. |