The money side of having a baby usually hits in one of two ways: a vague sense that “this will be expensive” or a very real “how are we going to pay for this delivery bill?” The fix isn’t earning six figures—it’s having a clear checklist and knowing which levers to pull first. This guide walks through how to prepare financially for a baby, what the first-year budget really looks like, and how to avoid the most common money traps new parents hit.

Financial checklist for having a baby (without blowing up your budget)

Whether you’re planning, already pregnant, or staring at a due date, this guide gives you a practical financial plan—not just a list of generic tips. You’ll get a 5-step process, realistic first-year budget ranges, insurance and legal must-dos, tax credits you might be missing, and the specific money traps that catch parents off guard. This works whether you’re dual-income, single-income, or somewhere in between.

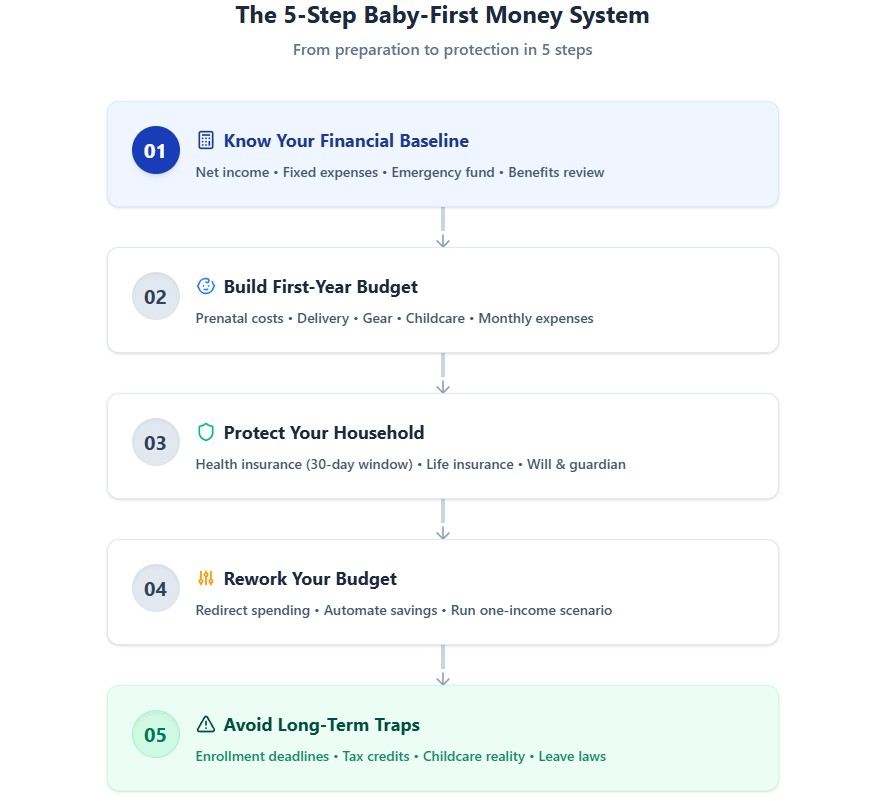

The 5-Step Baby-First Money System

Think of this as your financial roadmap for the baby journey. The system covers five critical areas: knowing your current financial baseline, building a realistic first-year budget, protecting your household with insurance and legal moves, reworking your budget around the baby, and avoiding long-term money traps. Once you set it up, you’ll have clarity instead of panic—and you’ll actually know where your money is going.

Step 1: Know where your money actually stands

Before you worry about a baby expenses list, you need a snapshot of your current finances. Not a perfect spreadsheet—just a clear picture.

Start with three quick numbers:

- Monthly net income: What hits your bank each month after taxes and benefits.

- Fixed expenses: Housing, utilities, insurance, debt payments, basic groceries, transportation.

- Emergency savings: Cash you could access within a few days.

Now connect those to “baby reality” instead of abstract goals.

- Discretionary cash flow: Subtract fixed expenses from net income. Whatever’s left is what can move to baby costs, savings, or debt payoff.

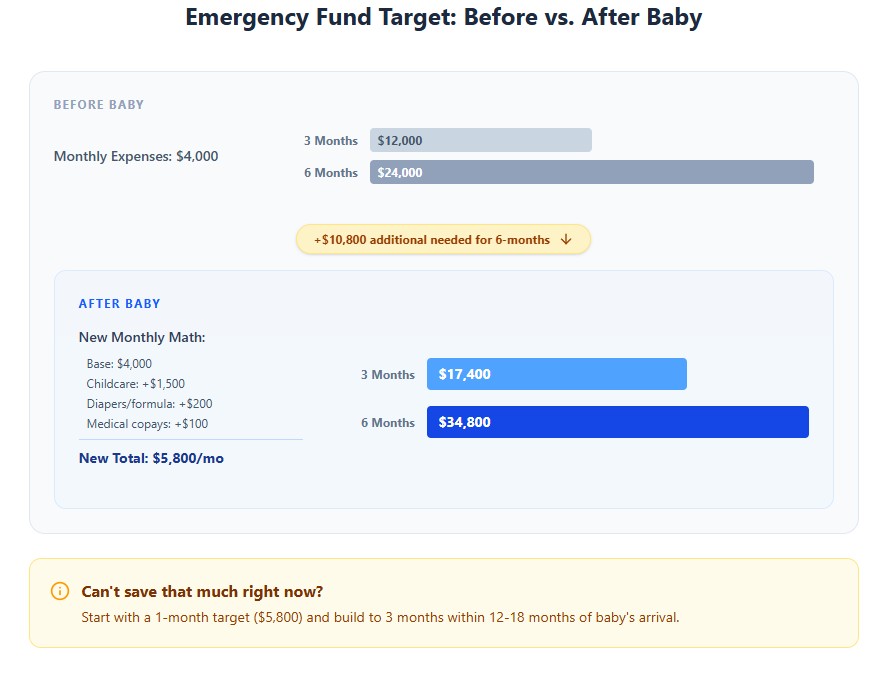

- Emergency fund target: Aim for 3–6 months of expenses, but adjust the “expenses” number to include expected baby costs like diapers and childcare. If that feels impossible right now, set a smaller milestone (1 month) and build from there. Learn how to build an emergency fund that actually works.

- Credit and backup plan: Pull your credit report and score. You don’t want to discover a surprise collections account while applying for a new card to cover medical bills. Understanding credit score basics: how it really works and what actually matters can help you prepare.

Last piece in this step: employer benefits. These are the hidden levers most people don’t read until they’re already in the hospital.

- Check your parental leave policy (paid vs unpaid, eligibility rules, how long you must stay employed after leave).

- Review health insurance: deductible, out-of-pocket max, in-network hospitals and OBs, and what counts as maternity coverage.

- Confirm whether you can use a Flexible Spending Account (FSA) or Health Savings Account (HSA) for pregnancy and baby-related medical costs.

This is the foundation for every decision that follows. Without it, “budget for a baby first year” is just guesswork. Use a realistic budget you’ll stick to to track these changes over time.

Step 2: Build a realistic first-year baby budget

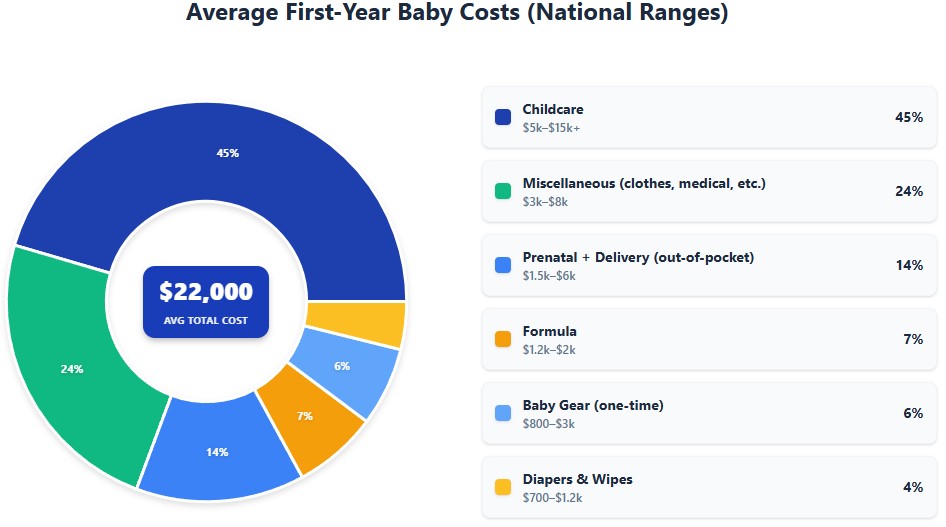

Here’s the answer to the question everyone Googles: there isn’t one single “right” number for how much a baby costs in the first year. But there are ranges you can plan around, then adjust for your area and lifestyle.

Those are national ranges. To make your own budget useful, do this on paper or in a simple sheet:

- List the categories above plus anything specific to you (e.g., extra travel to see family, higher rent if you’re not sure what you’ll pick).

- Call your insurer or log in to your portal and get a rough total for prenatal + delivery under your plan (based on your deductible and out-of-pocket max).

- Get local quotes for childcare now, even if you’re not sure what you’ll pick. Sticker shock is better in month 3 of pregnancy than month 3 of leave.

- Decide what you’ll buy new vs used. Car seat and crib safety come first; most other things can be gently used.

One tax detail that’s actually worth paying attention to: many pregnancy and delivery costs qualify as deductible medical expenses under IRS Section 213(d). That doesn’t mean you’ll automatically get a deduction, but it does mean you should keep every bill and receipt in one place for tax time.

Step 3: Protect the household (insurance, legal, and taxes)

This is the part almost everyone skips while they’re shopping for strollers. It’s not glamorous, but it keeps your family financially intact if something goes wrong.

Insurance and legal essentials

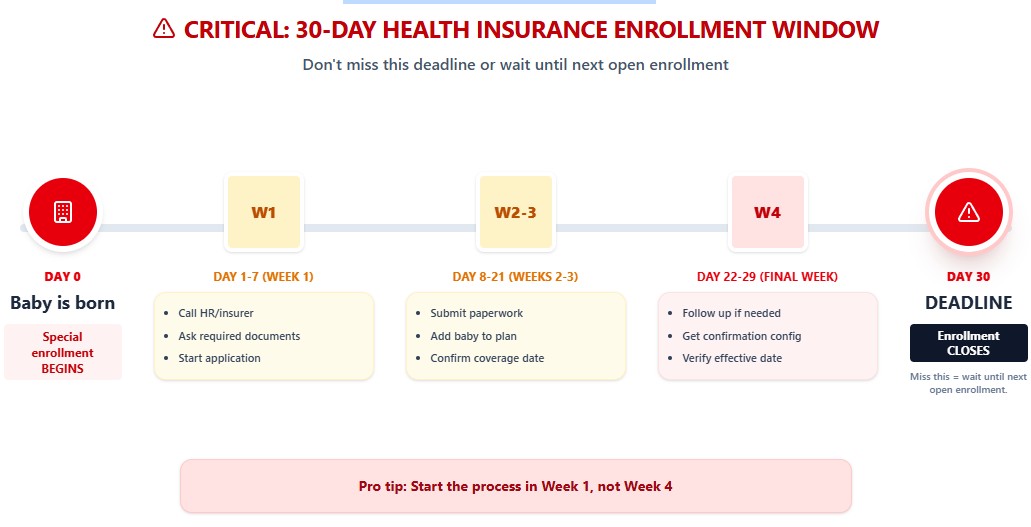

There’s a 30-day clock running after your baby is born, and missing it can get expensive fast.

- Add your baby to health insurance: Birth triggers a “special enrollment” window for employer plans and marketplace plans. You usually have 30 days to add your child. Call HR or your insurer and ask exactly what they need and by when.

- Life insurance: If someone depends on your income to live in your home and eat your food, they also depend on your income to exist if you’re gone. A common rule of thumb is about 10x your annual income in term life for primary earners.

- Will and guardian designation: You’re not writing a novel here. You’re answering: “Who makes decisions and cares for this kid if we’re not around?” A basic will that names a guardian and backup guardian is far better than no plan.

- Starter savings for the baby: Decide whether you care more about flexibility (UTMA/UGMA custodial account) or college-specific tax benefits (529 plan). You don’t have to fund it heavily on day one; even $25–$50 a month gets you in the habit.

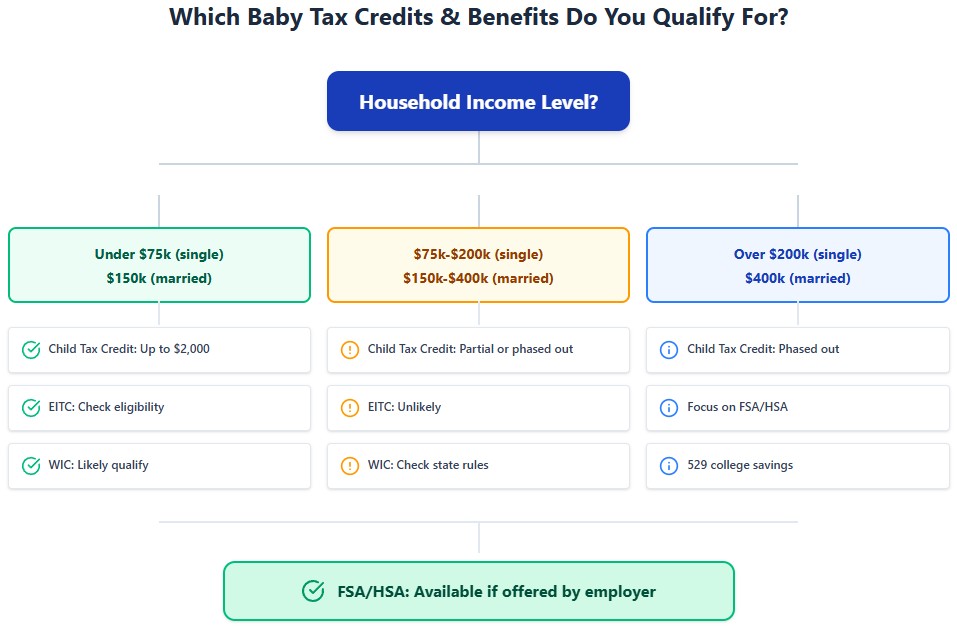

Tax credits and benefits you don’t want to miss

A lot of new parents leave money on the table simply because they don’t realize how many baby-related tax breaks exist.

- Child Tax Credit: Worth up to $2,000 per qualifying child under 17, with income limits and a portion that may be refundable. If your income is high, check the phase-out rules so you don’t count on money that won’t show up.

- Earned Income Tax Credit (EITC): If your household income is on the lower side, adding a child can increase your EITC amount significantly. It’s worth running your numbers, even if you’ve never qualified before.

- WIC (Women, Infants, and Children): If you qualify, WIC can offset formula and food costs. It’s not charity; it’s a federal nutrition program.

- FSA/HSA: Many baby-related medical costs are eligible: breast pumps, some baby meds, certain specialty formulas (often with a prescription). Paying for those with pre-tax dollars is an instant discount.

One thing that can slow all of this down: not having a Social Security number for your baby when you file taxes. Ask the hospital how and when they submit the SSN application, and don’t file until you have that number or you’re okay with a delayed refund.

Step 4: Rework your budget around the baby

This is where the “financial checklist for having a baby” turns into actual behavior. You don’t need to give up everything you enjoy—you just need to be intentional.

Start by deciding what gives:

- Look at the last 3 months of card and bank statements and total up dining out, subscriptions, and impulse buys.

- Decide how much of that you’re willing to redirect into childcare, medical bills, and baby gear.

- Set a specific monthly target: “We’re moving $300/month from ‘fun spending’ to ‘baby fund’ from now until birth.”

On the spending side, apply a simple rule: pay for function, not vibes.

- Borrow or buy used clothes, swings, bassinets, and toys from friends or trusted marketplaces.

- Resist the “registry inflation” spiral—if you’re not sure you’ll need it, wait. Target and Amazon exist after the baby arrives.

- Automate a transfer into a dedicated “baby” savings account as soon as you’re paid. If it never hits your main checking, you’re far more likely to stick to the plan.

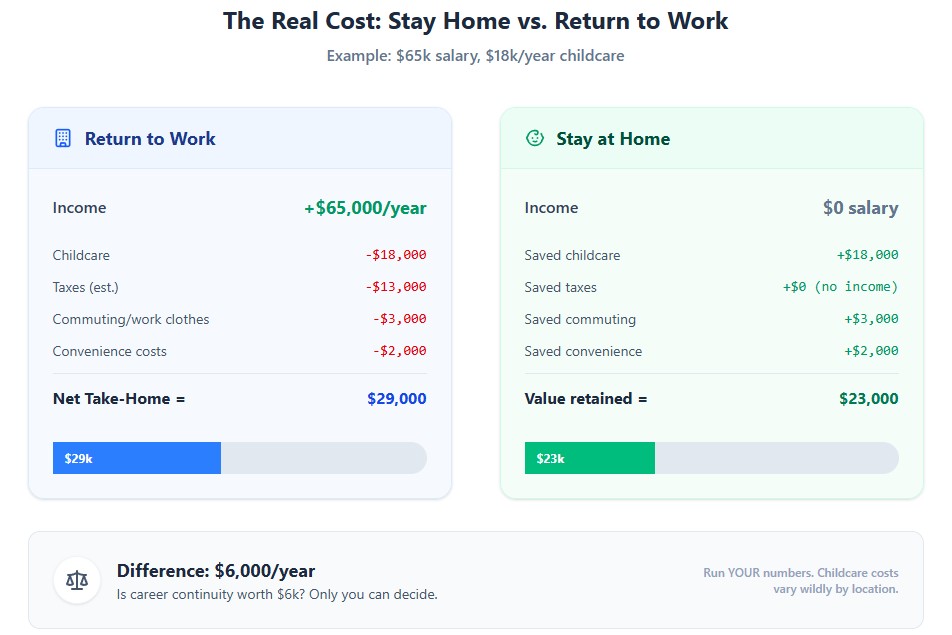

If one parent might reduce hours or stop working, run that scenario on paper:

“If I step back to part-time, we lose $X in take-home pay but save $Y in taxes and $Z in childcare.” Put real monthly numbers on that. Sometimes the “obvious” choice changes once you see the full math.

Step 5: Avoid the money traps that haunt parents for years

Most long-term financial problems from the baby stage come from a few predictable missteps. If you can dodge these, you’re already ahead.

- Delaying insurance enrollment: If you miss the special enrollment period, you may be stuck without coverage for your baby until the next open enrollment. That’s a nightmare scenario with NICU or follow-up visits.

- Assuming you’ll get every tax credit: Child Tax Credit and other benefits phase out at higher incomes. Don’t build your budget around them until you’ve confirmed eligibility.

- Underestimating childcare: In a lot of states, infant care costs more than in-state public college tuition. Sanity check your assumptions with at least two real quotes.

- Ignoring leave laws: Federal FMLA and state-level leave laws don’t all work the same. You might have job protection without pay, pay without job protection, or neither if you don’t meet the rules. HR is your first stop; your state labor site is your second.

- Raiding retirement to cover baby costs: It’s tempting, but tapping 401(k)s or IRAs early often triggers taxes and penalties and sets your future self on fire to keep your present self warm. Exhaust other options first.

Longer term, fold baby-related costs into your bigger financial plan instead of treating them as an emergency forever. That means checking in on:

- Whether your retirement contributions are still on track, even if temporarily reduced.

- How much you want to commit to education savings vs. your own financial stability.

- Whether your estate plan (wills, accounts, beneficiaries) still matches your actual wishes now that a new human is in the mix.

First-year baby budget ranges (with practical ways to control costs)

Use this table as your starting point. These are national averages—your actual costs will vary based on location, insurance coverage, and childcare choices. The key is getting real quotes early and building your own version of this table with local numbers.

| Expense Category | Type | Estimated Year 1 Range (USD) | How to Control the Cost |

|---|---|---|---|

| Prenatal care & delivery | One-time | $10,000–$30,000+ (before insurance) | Confirm in-network providers, understand your deductible and out-of-pocket max, ask for pre-estimates. |

| Diapers & wipes | Recurring | $700–$1,000/year | Buy in bulk, track per-diaper cost, consider cloth once you’re through the newborn chaos. |

| Infant formula | Recurring | $1,200–$1,800/year | Check eligibility for WIC, price out generics, ask pediatrician about safe lower-cost options. |

| Baby gear (crib, stroller, car seat) | One-time | $800–$2,000 | Buy quality used for everything except car seats and cribs unless you can verify safety/recall status. |

| Childcare | Recurring | $5,000–$15,000+/year | Compare daycare vs nanny share vs family care; lock this in early, especially in major cities. |

Tax credits, benefits, and savings paths new parents often miss

Many families don’t realize they qualify for tax breaks and programs that can save thousands in the first few years. This isn’t about gaming the system—it’s about using what’s already available.

Child Tax Credit: Worth up to $2,000 per qualifying child under 17. Check phase-out rules if your income is high so you don’t count on money that won’t show up. A portion may be refundable even if you don’t owe taxes.

Earned Income Tax Credit (EITC): If your household income is on the lower side, adding a child can increase your EITC amount significantly. It’s worth running your numbers, even if you’ve never qualified before.

WIC (Women, Infants, and Children): If you qualify, WIC can offset formula and food costs. It’s a federal nutrition program, not charity, and many eligible families don’t use it.

FSA/HSA: Many baby-related medical costs are eligible: breast pumps, some baby meds, certain specialty formulas (often with a prescription). Paying for those with pre-tax dollars is an instant discount.

Medical expense deduction: Many pregnancy and delivery costs qualify as deductible medical expenses under IRS Section 213(d). Keep every bill and receipt in one place for tax time.

One-page baby-first-year financial checklist (copy-paste version)

Copy this table into Google Sheets or Excel. Use it to track what’s done, what’s in progress, and what’s still on your plate. Assign responsibilities and set reminder dates so nothing falls through the cracks.

| Checklist Item | Status | Responsible Person | Deadline / Reminder | Notes |

|---|---|---|---|---|

| Review health insurance maternity coverage | ||||

| Check parental leave policy (paid/unpaid) | ||||

| Calculate emergency fund target (3-6 months) | ||||

| Get prenatal + delivery cost estimate from insurer | ||||

| Get 2-3 local childcare quotes | ||||

| Decide new vs used for baby gear | ||||

| Set up dedicated baby savings account | ||||

| Add baby to health insurance (within 30 days of birth) | ||||

| Apply for baby’s Social Security number | ||||

| Review/update life insurance coverage | ||||

| Create will and name guardian | ||||

| Confirm Child Tax Credit eligibility | ||||

| Check WIC eligibility | ||||

| Set up 529 or UTMA account (optional) | ||||

| Run one-income scenario (if applicable) |

Why this 5-step system works for new parents

The 5-Step Baby-First Money System covers all the critical bases without overwhelming you. Step 1 gives you clarity on where you stand. Step 2 turns vague worry into concrete numbers. Step 3 protects your family from insurance, legal, and tax surprises. Step 4 makes the budget actually work in real life. Step 5 keeps you from making the mistakes that haunt parents for years.

This system works whether you’re making $60k or $160k because it focuses on process, not perfection. You’re not trying to save every penny or buy the cheapest everything. You’re building a financial structure that moves money where it needs to go before you even think about it.

The result? You avoid the 30-day insurance enrollment nightmare, you don’t miss tax credits worth thousands, you know exactly what childcare will cost before you sign anything, and you have a plan instead of panic. That’s the difference between surviving the first year and actually enjoying it.

Disclaimer: This content is for informational purposes only and doesn’t replace professional financial, legal, or tax advice. Rules and programs change and vary by location. Talk with a qualified advisor, tax professional, or attorney about your specific situation.