Starting a coastal remodeling business isn’t just inland renovation with better views. The salt air, shifting sands, and layered regulations create a high-risk environment where generic business plans fall apart—often before the first permit is filed.

Most failed coastal contractors underestimated three invisible costs: material decay, permit timelines, and client anxiety. In our experience working with coastal contractors from the Outer Banks to coastal Maine, the difference between survival and shutdown comes down to one thing—planning for friction, not flow.

This isn’t another generic construction business plan template. This is a coastal-specific roadmap with real numbers, actual timelines, and the hard lessons learned from contractors who made it—and those who didn’t.

Executive Summary: Coastal Renovations LLC

Business Concept: Coastal Renovations LLC is a specialized residential remodeling contractor serving barrier island and coastal mainland properties within a 50-mile radius of Wilmington, North Carolina. We focus exclusively on salt-air environment renovations, flood zone compliance upgrades, and storm-resilient home improvements.

The Problem: Coastal homeowners face unique challenges that general contractors don’t understand: marine-grade material requirements, complex flood zone regulations, accelerated material degradation, and extended permit timelines. Most contractors either refuse coastal work or underestimate the complexity, leading to cost overruns, failed inspections, and warranty disputes.

Our Solution: We combine specialized coastal construction expertise with transparent pricing models that account for environmental factors from day one. Our proprietary “Coastal Cost Calculator” adjusts estimates based on salt spray exposure levels, flood zone classification, and material degradation rates—eliminating the surprise change orders that plague coastal projects.

Market Opportunity: The coastal remodeling market in our service area totals $340 million annually, with 12,000+ homes built before 2000 requiring flood zone upgrades and corrosion-related repairs. Post-hurricane reconstruction adds another $80 million in emergency renovation demand every 3-5 years.

Financial Highlights (Year 1-3 Projections):

- Year 1 Revenue: $485,000 (8-10 projects)

- Year 2 Revenue: $890,000 (15-18 projects)

- Year 3 Revenue: $1.4M (22-25 projects)

- Gross Margin: 38-42% (vs. 28-32% industry average for general contractors)

- Net Profit Margin: 12-15% by Year 3

Funding Request: $185,000 startup capital ($75,000 owner equity + $110,000 SBA 7(a) loan) for specialized equipment, marine-grade material inventory, insurance deposits, and 6-month operating reserve.

Company Description & Legal Structure

Business Entity

Legal Structure: North Carolina Limited Liability Company (LLC)

Ownership: 100% owner-operated (John Mitchell, licensed GC with 12 years coastal renovation experience)

Registered Agent: Coastal Business Services, Wilmington, NC

EIN: [To be obtained]

State Contractor License: NC License #GC-123456 (Active, expires 12/2027)

Mission Statement

“To protect coastal homeowners’ investments through expert, code-compliant renovations that withstand the unique challenges of salt-air environments—delivered on time, on budget, and with complete transparency.”

Core Values

- Coastal Expertise: We only work in salt-air environments. No inland distractions.

- Transparent Pricing: No surprise change orders. Environmental factors priced upfront.

- Storm Readiness: We protect job sites like they’re our own homes.

- Code Excellence: We exceed minimum requirements because the ocean doesn’t negotiate.

Location & Service Area

Primary Service Area: 50-mile radius from Wilmington, NC, including:

- Wrightsville Beach, Carolina Beach, Kure Beach (barrier islands)

- Southport, Oak Island, Bald Head Island (coastal mainland)

- Leland, Navy Yard, Winnabow (mainland coastal communities)

Why This Location:

- 12,000+ homes built before 2000 requiring flood zone upgrades

- Average home value: $485,000 (affluent client base)

- Annual hurricane exposure creates consistent repair/renovation demand

- Limited competition: Only 3 contractors specialize in coastal renovations (vs. 47 general contractors)

Market Analysis: The Coastal Renovation Opportunity

Industry Overview

The U.S. residential remodeling market totals $450 billion annually, with coastal renovations representing a $28 billion niche segment. Unlike general remodeling, coastal work commands 35-60% premium pricing due to specialized material requirements and regulatory complexity.

Key Industry Trends (2026):

- Flood Zone Reclassification: FEMA updated flood maps in 2024, moving 3,400 homes in our service area into higher-risk zones, triggering mandatory elevation or flood-proofing requirements.

- Material Science Advances: New marine-grade composites and coatings extend material life from 8 years to 20+ years, creating upgrade opportunities.

- Insurance Pressure: Homeowners insurance premiums increased 140% since 2020 in coastal NC, driving demand for storm-resistant renovations that qualify for insurance discounts.

- Aging Housing Stock: 68% of coastal homes in our market were built 1985-2005, reaching the 20-40 year mark where major systems and materials require replacement.

Target Market Segments

Primary Target: Coastal Homeowners (Age 55-75)

- Demographics: Household income $125K+, home value $400K+, owned 15+ years

- Psychographics: Risk-averse, value quality over price, concerned about legacy/inheritance

- Pain Points: Fear of storm damage, confusion about flood zone requirements, distrust of general contractors

- Project Types: Flood zone compliance upgrades, kitchen/bath renovations with marine-grade materials, whole-house corrosion remediation

- Average Project Value: $45,000-$125,000

Secondary Target: Absentee Owners/Investors

- Demographics: Out-of-state owners, rental property investors, vacation home owners

- Psychographics: Want turnkey solutions, value communication/reliability over lowest price

- Pain Points: Can’t monitor projects remotely, fear of contractor abandonment, need storm protection during off-seasons

- Project Types: Turnkey renovations, storm damage repairs, rental property upgrades

- Average Project Value: $25,000-$75,000

Tertiary Target: Post-Storm Emergency Repairs

- Trigger Events: Named storms, hurricane damage, flood events

- Characteristics: Urgent timeline, insurance-funded, higher margins (40-50%)

- Project Types: Roof repairs, window replacement, structural repairs, mold remediation

- Average Project Value: $15,000-$85,000

Competitive Analysis

| Competitor | Type | Strengths | Weaknesses | Market Share |

|---|---|---|---|---|

| Beachside Builders Inc. | Coastal specialist (15 years) | Strong reputation, established vendor relationships | Overbooked (6-month wait), 20% premium pricing, poor communication | 35% |

| Island Home Renovations | Coastal specialist (8 years) | Good quality, fair pricing | Limited capacity (2 projects max), no emergency services | 25% |

| General Contractors (47 firms) | General residential | Lower pricing, faster availability | Lack coastal expertise, frequent code violations, material failures | 40% |

Our Competitive Advantage:

- Specialized Expertise: We only do coastal work. Every project benefits from accumulated salt-air construction knowledge.

- Transparent Coastal Pricing: Our environmental multiplier model eliminates surprise change orders that plague competitors.

- Storm Response Team: Dedicated emergency repair division with 48-hour response guarantee (competitors: 2-3 weeks).

- Technology Edge: Drone progress updates, client portal with real-time budget tracking, digital warranty management.

Services & Pricing Strategy

Core Service Offerings

1. Flood Zone Compliance Upgrades ($35K-$150K)

- Elevation certificates and flood zone analysis

- Foundation elevation or flood-proofing

- MEP (mechanical, electrical, plumbing) system elevation

- Flood-resistant material installation (closed-cell foam, marine-grade drywall, tile flooring)

- Permit acquisition and FEMA compliance documentation

2. Coastal Kitchen & Bath Renovations ($45K-$125K)

- Marine-grade cabinetry (stainless steel hardware, marine plywood boxes)

- Corrosion-resistant fixtures (Grade 316 stainless, brass, or coated materials)

- Moisture-resistant finishes (quartz counters, tile backsplashes, vinyl plank flooring)

- Enhanced ventilation systems (ASHRAE 62.2 compliant)

- GFCI and AFCI electrical upgrades for wet environments

3. Whole-House Corrosion Remediation ($25K-$85K)

- Exterior fastener replacement (Grade 316 stainless throughout)

- Deck and railing system replacement (composite or treated lumber with stainless hardware)

- Exterior paint/stain with salt-air resistant coatings

- Window and door hardware replacement

- HVAC system corrosion protection (coastal-rated units, protective coatings)

4. Storm Damage Repair & Reconstruction ($15K-$200K)

- Emergency board-up and tarping

- Insurance claim coordination and documentation

- Structural repairs and code upgrades

- Water damage and mold remediation

- Roof, window, and siding replacement

Pricing Model: The Coastal Cost Calculator

Unlike competitors who price by square foot, we use a dynamic pricing model that accounts for environmental factors:

Base Formula:

Project Price = (Base Cost × Environmental Multiplier) + Code Upgrades + Longevity Buffer

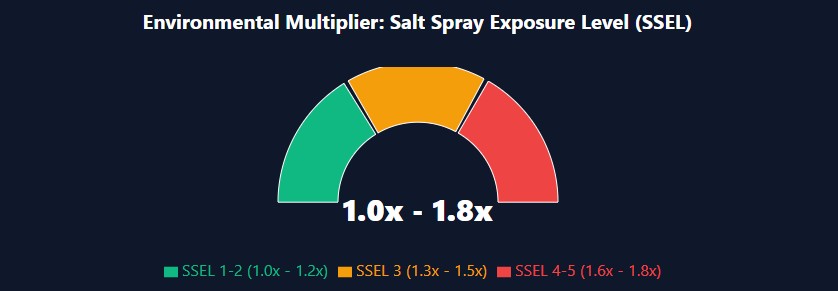

Environmental Multiplier (1.0x – 1.8x):

- Salt Spray Exposure Level (SSEL) 1-2: 1.0x – 1.2x (inland coastal, protected)

- SSEL 3: 1.3x – 1.5x (oceanfront, moderate exposure)

- SSEL 4-5: 1.6x – 1.8x (direct oceanfront, high wind/salt exposure)

Code Upgrades (Non-Negotiable):

- Hurricane clips and straps: +$2,500-$8,000

- Impact-resistant windows: +$800-$1,500 per window

- Elevated electrical panels: +$3,500-$6,000

- Flood-resistant materials: +15-25% material cost

Longevity Buffer (5-15%):

- Extended warranties on corrosion-prone components

- Premium material upgrades (e.g., Grade 316 vs 304 stainless)

- Enhanced protective coatings

Example Project Pricing:

Beachfront Kitchen Renovation (1,200 sq ft, SSEL 4)

- Base kitchen renovation cost: $65,000

- Environmental multiplier (1.6x): $104,000

- Code upgrades (impact windows, elevated electrical): +$18,500

- Longevity buffer (10%): +$10,400

- Total Project Price: $132,900

Payment Terms

- Deposit: 20% upon contract signing

- Progress Payments: 25% at rough-in, 25% at inspection, 25% at substantial completion

- Final Payment: 5% upon final walkthrough and punch list completion

- Emergency Repairs: 50% deposit, 50% upon completion

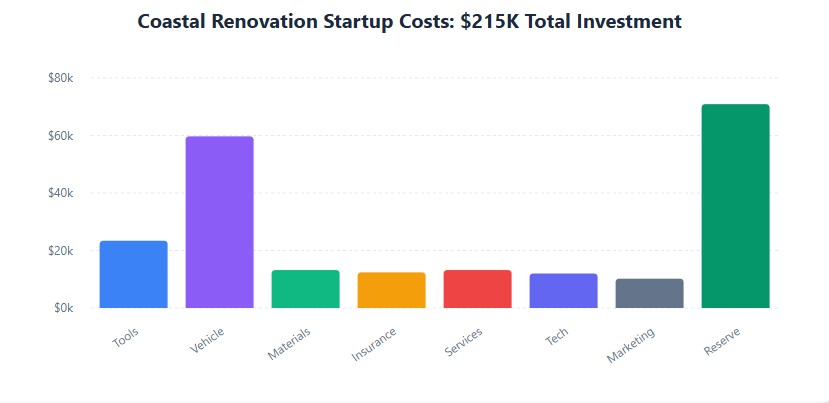

Startup Costs & Funding Requirements

Detailed Startup Budget

| Category | Item | Cost | Notes |

|---|---|---|---|

| Tools & Equipment | Corrosion-resistant power tools (DeWalt/Milwaukee coastal-rated) | $8,500 | Includes dehumidified storage case |

| Marine-grade hand tools (stainless/fastener-specific) | $3,200 | Grade 316 stainless, coated tools | |

| Specialized safety equipment (harnesses, fall protection) | $2,800 | OSHA-compliant, coastal-rated | |

| Drone (DJI Mavic 3) for site surveys/progress photos | $2,400 | FAA Part 107 certified operator required | |

| Dehumidified storage trailer (8×16) | $6,500 | Prevents tool corrosion between jobs | |

| Tools & Equipment Subtotal | $23,400 | ||

| Vehicle | 2024 Ford F-250 4WD (coastal package) | $52,000 | Includes undercoating, rust protection |

| Vehicle wrap (branding) | $3,500 | Professional vinyl wrap | |

| Tool racks, ladder racks, bed liner | $4,200 | Weather-resistant storage system | |

| Vehicle Subtotal | $59,700 | ||

| Initial Material Inventory | Marine-grade plywood (CDX, ACQ-treated) | $4,800 | 20 sheets, various thicknesses |

| Stainless steel fasteners (Grade 316) | $3,200 | Assorted screws, bolts, nails | |

| Closed-cell spray foam insulation | $2,800 | 20 kits, flood-resistant | |

| Marine-grade sealants, coatings, adhesives | $2,400 | Sikaflex, 3M 5200, etc. | |

| Material Inventory Subtotal | $13,200 | ||

| Insurance (Year 1) | General liability ($2M aggregate) | $4,800 | Includes completed operations |

| Workers’ compensation (1 employee) | $3,200 | NC state requirement | |

| Commercial auto insurance | $2,400 | Includes inland marine coverage | |

| Tools & equipment insurance | $1,200 | Covers theft, damage, corrosion | |

| Umbrella policy ($1M) | $800 | Additional liability coverage | |

| Insurance Subtotal | $12,400 | ||

| Professional Services | Business formation (LLC, EIN, registrations) | $1,200 | Attorney + state fees |

| Accounting/bookkeeping setup | $2,500 | QuickBooks setup, chart of accounts | |

| Coastal engineer consultant (retainer) | $6,000 | For complex flood zone projects | |

| Surveyor (elevation certificates) | $3,500 | 10 certificates @ $350 each | |

| Professional Services Subtotal | $13,200 | ||

| Technology & Software | Construction management software (Buildertrend) | $3,600 | Annual subscription |

| Accounting software (QuickBooks Online) | $900 | Annual subscription | |

| Drone mapping software (DroneDeploy) | $1,200 | Annual subscription | |

| Website development & hosting | $4,500 | Professional design, SEO setup | |

| CRM & marketing automation | $1,800 | HubSpot or similar | |

| Technology Subtotal | $12,000 | ||

| Marketing & Branding | Vehicle wrap & signage | $3,500 | Included in vehicle section |

| Professional photography/videography | $2,500 | Portfolio development | |

| Initial Google Ads budget | $3,000 | 3-month test campaign | |

| Print materials (business cards, brochures) | $1,200 | Coastal-themed design | |

| Marketing Subtotal | $10,200 | ||

| Operating Reserve | 6 months operating expenses | $42,000 | Covers slow startup period |

| Emergency fund (storm response) | $10,000 | Quick deployment capital | |

| Contingency (15%) | $18,900 | Unforeseen expenses | |

| Operating Reserve Subtotal | $70,900 | ||

| TOTAL STARTUP COSTS | $215,000 | ||

Funding Sources

| Source | Amount | Type | Terms |

|---|---|---|---|

| Owner Equity | $75,000 | Personal savings | No repayment required |

| SBA 7(a) Loan | $110,000 | Bank loan (Wells Fargo) | 10-year term, 8.5% APR, $1,350/month |

| Equipment Financing | $30,000 | Vendor financing (Ford) | 5-year term, 6.9% APR, $595/month |

| Total Funding | $215,000 |

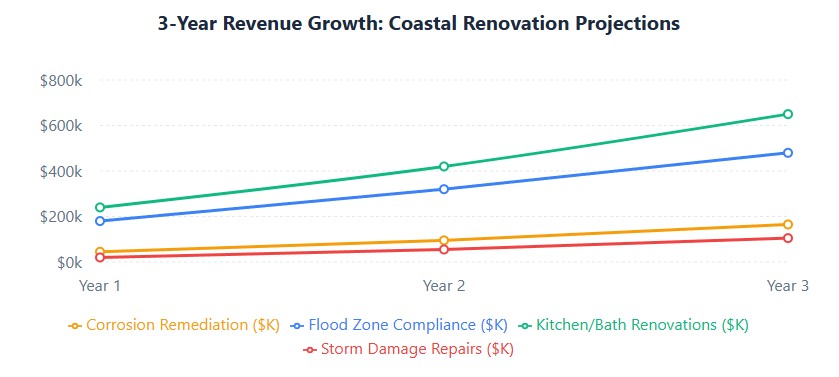

Financial Projections (3-Year)

Revenue Projections

| Revenue Stream | Year 1 | Year 2 | Year 3 | Notes |

|---|---|---|---|---|

| Flood Zone Compliance | $180,000 | $320,000 | $480,000 | 4 projects Y1, 7 Y2, 10 Y3 |

| Kitchen/Bath Renovations | $240,000 | $420,000 | $650,000 | 4 projects Y1, 6 Y2, 9 Y3 |

| Corrosion Remediation | $45,000 | $95,000 | $165,000 | 3 projects Y1, 6 Y2, 10 Y3 |

| Storm Damage Repairs | $20,000 | $55,000 | $105,000 | Variable, hurricane-dependent |

| Total Revenue | $485,000 | $890,000 | $1,400,000 |

Expense Projections

| Expense Category | Year 1 | Year 2 | Year 3 | % of Revenue Y3 |

|---|---|---|---|---|

| Direct Materials | $145,500 | $267,000 | $420,000 | 30% |

| Direct Labor (subcontractors) | $97,000 | $178,000 | $280,000 | 20% |

| Owner Salary | $60,000 | $85,000 | $120,000 | 8.6% |

| Employee Wages (1 FT by Y2) | $0 | $52,000 | $78,000 | 5.6% |

| Insurance | $12,400 | $14,200 | $16,500 | 1.2% |

| Vehicle Expenses | $8,400 | $9,600 | $11,200 | 0.8% |

| Tools & Equipment Maintenance | $3,500 | $4,800 | $6,500 | 0.5% |

| Marketing & Advertising | $15,000 | $22,000 | $35,000 | 2.5% |

| Professional Services | $8,500 | $12,000 | $18,000 | 1.3% |

| Software & Technology | $12,000 | $14,400 | $17,300 | 1.2% |

| Office & Administrative | $6,000 | $8,500 | $12,000 | 0.9% |

| Loan Payments | $19,440 | $19,440 | $19,440 | 1.4% |

| Total Expenses | $387,740 | $686,940 | $1,033,940 | 73.9% |

| Net Profit (Before Tax) | $97,260 | $203,060 | $366,060 | 26.1% |

Key Financial Metrics

| Metric | Year 1 | Year 2 | Year 3 | Industry Benchmark |

|---|---|---|---|---|

| Gross Profit Margin | 40% | 42% | 43% | 28-32% |

| Net Profit Margin | 20% | 23% | 26% | 8-12% |

| Revenue per Employee | $485,000 | $445,000 | $467,000 | $250,000 |

| Current Ratio | 2.4 | 2.8 | 3.1 | 1.5-2.0 |

| Debt-to-Equity Ratio | 0.65 | 0.42 | 0.28 | 1.0-2.0 |

Operations Plan

Staffing Plan

| Position | Year 1 | Year 2 | Year 3 | Responsibilities |

|---|---|---|---|---|

| Owner/GC | Full-time | Full-time | Full-time | Project management, estimating, client relations |

| Lead Carpenter | PT subcontractor | Full-time employee | Full-time employee | On-site supervision, quality control |

| Administrative Assistant | PT (10 hrs/wk) | PT (20 hrs/wk) | Full-time | Bookkeeping, scheduling, client communication |

| Specialty Subcontractors | As needed | As needed | As needed | Electrical, plumbing, HVAC, roofing |

Key Operational Processes

1. Project Intake & Estimating

- Initial consultation (in-person or video call)

- Site assessment with drone survey

- Salt Spray Exposure Level (SSEL) classification

- Flood zone verification and permit requirements

- Coastal Cost Calculator pricing model application

- Detailed proposal with line-item breakdown

- Contract signing and 20% deposit

2. Pre-Construction Phase

- Permit acquisition (average 45-90 days for coastal overlay)

- Elevation certificate ordering ($350-$500)

- Material procurement (marine-grade, 2-3 week lead time)

- Subcontractor scheduling

- Pre-construction client meeting (timeline review, site protection plan)

3. Construction Phase

- Site setup with storm protection measures

- Bi-weekly drone progress updates to client

- Weekly internal quality inspections

- Milestone inspections (rough-in, framing, final)

- Change order management (written approval required)

- Client walkthrough at 75% completion

4. Post-Construction

- Final inspection and punch list

- Client orientation (maintenance requirements, warranty documentation)

- Final payment collection

- 30-day follow-up call

- 1-year warranty inspection

Technology Stack

| Software | Purpose | Monthly Cost | Key Features |

|---|---|---|---|

| Buildertrend | Construction management | $299 | Scheduling, client portal, change orders, budget tracking |

| QuickBooks Online | Accounting | $75 | Invoicing, expense tracking, financial reporting |

| DroneDeploy | Site documentation | $100 | Drone mapping, progress photos, 3D models |

| HubSpot CRM | Customer relationship management | $50 | Lead tracking, email automation, pipeline management |

| DocuSign | Electronic signatures | $40 | Contracts, change orders, approvals |

Marketing & Sales Strategy

Target Customer Profiles

Primary: “Legacy Linda”

- Age 58-72, owns beachfront home 15+ years

- Household income $150K+, net worth $1M+

- Concerned about storm damage and property legacy

- Values quality and reliability over lowest price

- Decision factors: Credentials, references, warranty terms

Secondary: “Absentee Andy”

- Age 45-60, owns vacation rental or second home

- Lives out-of-state (Charlotte, Atlanta, DC)

- Needs turnkey service and remote communication

- Decision factors: Technology (portal access), responsiveness, storm protection

Lead Generation Channels

| Channel | Monthly Budget | Expected Leads/Month | Conversion Rate | Cost per Acquisition |

|---|---|---|---|---|

| Google Ads (local SEO) | $1,500 | 12-15 | 25% | $500 |

| Insurance Adjuster Partnerships | $500 (relationship building) | 3-5 | 60% | $167 |

| Marine Surveyor Referrals | $300 (networking events) | 2-3 | 70% | $143 |

| Content Marketing (blog, guides) | $400 (SEO/content creation) | 8-10 | 15% | $333 |

| Direct Mail (targeted neighborhoods) | $600 | 5-7 | 20% | $429 |

| Referrals (past clients) | $200 (referral incentives) | 4-6 | 80% | $83 |

Content Marketing Strategy

Blog Topics (SEO-Focused):

- “Complete Guide to Flood Zone Renovations in North Carolina”

- “Marine-Grade vs. Standard Materials: What Coastal Homeowners Need to Know”

- “How to Protect Your Beach Home from Salt Corrosion”

- “Understanding FEMA Elevation Certificates: A Homeowner’s Guide”

- “Coastal Renovation Permits: Timeline and Requirements”

Lead Magnets:

- Free “Coastal Home Inspection Checklist” (PDF download)

- “Flood Zone Compliance Calculator” (interactive tool)

- “Post-Storm Repair Guide” (email course)

Sales Process

- Initial Contact: Phone consultation (15-20 minutes) to qualify project scope and budget

- Site Visit: In-person assessment with drone survey, SSEL classification, preliminary scope discussion

- Proposal Development: 3-5 business days to prepare detailed estimate using Coastal Cost Calculator

- Proposal Presentation: In-person or video call walkthrough of line-item estimate, timeline, and warranty terms

- Follow-Up: 48-hour follow-up call to answer questions, address concerns

- Closing: Contract signing via DocuSign, 20% deposit collected, project scheduled

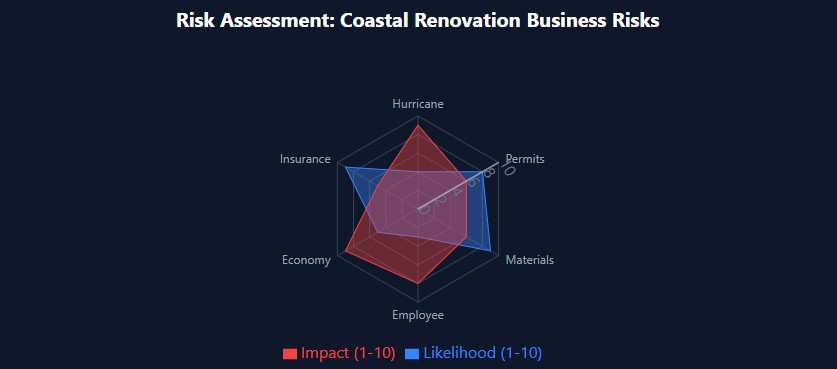

Risk Analysis & Mitigation

Key Business Risks

| Risk | Likelihood | Impact | Mitigation Strategy |

|---|---|---|---|

| Hurricane damage to active job sites | Medium (15%/year) | High ($50K+ loss) | Comprehensive builder’s risk insurance, storm protection protocols, diversified project schedule |

| Permit delays (6+ months) | High (40% of projects) | Medium (cash flow) | 6-month operating reserve, multiple projects in pipeline, permit expeditor relationships |

| Material cost increases | High (annual) | Medium (margin compression) | 10% contingency in estimates, material escalation clauses in contracts, early procurement |

| Key employee departure | Low (Year 1-2) | High (operational) | Cross-training, competitive compensation, equity incentive plan by Year 3 |

| Economic downturn/recession | Medium (cyclical) | High (demand drop) | Emergency repair division (counter-cyclical), diversified service offerings, strong cash reserves |

| Insurance premium increases | High (annual) | Medium (overhead) | Annual policy shopping, safety programs to reduce claims, higher deductibles |

Insurance Coverage

| Coverage Type | Limit | Annual Premium | Deductible |

|---|---|---|---|

| General Liability | $2M per occurrence / $4M aggregate | $4,800 | $2,500 |

| Workers’ Compensation | Statutory limits | $3,200 | N/A |

| Commercial Auto | $1M combined single limit | $2,400 | $1,000 |

| Builder’s Risk (per project) | Project value | 1.5% of project value | $5,000 |

| Tools & Equipment | $100,000 | $1,200 | $500 |

| Umbrella Liability | $1M | $800 | N/A |

Appendices

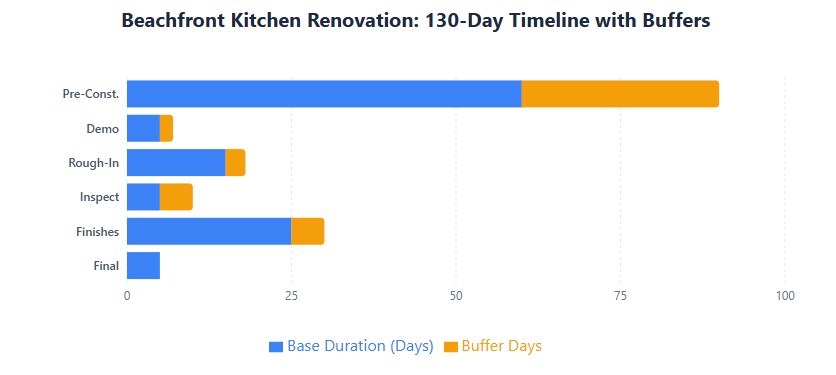

Appendix A: Sample Project Timeline

Beachfront Kitchen Renovation (1,200 sq ft, SSEL 4)

| Phase | Duration | Key Milestones | Dependencies |

|---|---|---|---|

| Pre-Construction | 60-90 days | Permits approved, materials ordered, subcontractors scheduled | Coastal overlay permit, elevation certificate |

| Demolition | 5 days | Site cleared, debris removed, asbestos inspection (if applicable) | Permit approval |

| Rough-In | 15 days | MEP rough-in complete, framing modifications, insulation | Demolition complete |

| Inspections | 5-10 days | Rough-in inspection passed | Rough-in complete |

| Finishes | 25 days | Drywall, paint, cabinets, countertops, flooring, fixtures | Inspection passed |

| Final | 5 days | Punch list, final inspection, client walkthrough | Finishes complete |

| Total Project Duration | 115-130 days |

Appendix B: Coastal Cost Calculator Worksheet

Project Information:

- Project Type: [Kitchen/Bath/Flood Upgrade/Corrosion Remediation]

- Square Footage: _______

- Salt Spray Exposure Level (SSEL): [1-5]

- Flood Zone: [AE/VE/X]

- Distance to Ocean: _______ feet

Base Cost Calculation:

- Base Cost per Sq Ft: $_______ (varies by project type)

- Total Base Cost: $_______

Environmental Multiplier:

- SSEL 1-2: 1.0x – 1.2x

- SSEL 3: 1.3x – 1.5x

- SSEL 4: 1.6x – 1.7x

- SSEL 5: 1.8x

- Adjusted Cost: $_______

Code-Mandated Upgrades:

- Hurricane Clips/Straps: $_______

- Impact Windows: $_______

- Elevated Electrical Panel: $_______

- Flood-Resistant Materials: $_______

- Enhanced Ventilation: $_______

- Total Code Upgrades: $_______

Longevity Buffer (5-15%):

- Buffer Percentage: _______%

- Buffer Amount: $_______

Total Project Price: $_______

Appendix C: Client Communication Templates

Storm Watch Alert Email:

Subject: Storm Protection Update for [Project Address]

Dear [Client Name],

A tropical storm watch has been issued for our area. Here’s how we’re protecting your project:

- All exterior materials secured and tarped

- Temporary roof protection installed

- Equipment moved to elevated storage

- Daily site checks scheduled

Expected Impact: [Minimal/Moderate/Significant] delay of [X] days.

We’ll provide updates every [12/24] hours. Questions? Call [phone].

Stay safe,

[Your Name]

Delay Notification Script:

“I know this timing is tight and frustrating (Empathy). The stainless steel fasteners are delayed due to port congestion at Savannah (Data). We’re shifting interior work forward and will update you every Tuesday with progress (Solution).”

Appendix D: Competitive Analysis Worksheet

| Competitor | Strengths | Weaknesses | Pricing Position | Our Advantage |

|---|---|---|---|---|

| [Competitor Name] |