Why This Matters Right Now (No Drama, Just Facts)

Money is tighter. The Fed kept rates at 5.25%–5.50% through mid-2024, and most analysts expect them to stay above 4% into 2026. That means SBA lenders aren’t just glancing at your projections—they’re digging in. They want to see a realistic Debt Service Coverage Ratio (DSCR) and consistent month-over-month growth. Not hope. Not “we’ll figure it out.”

At the same time, if you take prepayments or work on retainers, you need to understand one key split: how you report revenue to investors (GAAP/ASC 606) isn’t always how you report it to the IRS. Mess that up, and you create confusion during fundraising or, worse, an audit flag.

This isn’t a tax seminar. It’s a forecasting guide. But ignoring these basics can break your model. So we’ll keep compliance light, focused, and only where it directly impacts your numbers.

The 7-Step Framework (Built for Service Startups, Not SaaS)

Most revenue forecasting templates assume you’re selling subscriptions. You’re not. You’re selling time, expertise, or projects. Your model needs to reflect that.

Step 1: Lock Down Your Pricing Model First

Are you billing hourly, on retainer, or per project? This changes everything.

- Hourly? You need a realistic utilization rate. (Hint: 70–80% billable is strong for most service firms.)

- Retainer? Great—predictable cash. But remember: under GAAP, you recognize it over time, not when the wire hits.

- Project-based? Map delivery timelines. Revenue hits when milestones are met, not when you sign the SOW.

Pro tip: If you mix models (many agencies do), forecast each stream separately. Then roll them up.

Step 2: Get Real About Average Contract Value (ACV)

No historical data? Start with benchmarks, then adjust fast.

- IT consulting: ~$18,500/year per client (IBISWorld, 2025)

- Marketing services: ~$12,800/year (same source)

- Legal/consulting retainers: $2,500–$10,000/month depending on scope

Don’t guess. Pull your CRM. If you’re pre-revenue, talk to 3–5 potential clients. Ask what they’d pay. Then cut that number by 20% for your base case.

Step 3: Calculate MRR—But Adjust for Churn (Because Clients Leave)

Formula:

(Active Clients × Avg Monthly Fee) × (1 – Monthly Churn Rate)

Example:

15 clients × $3,000/month × (1 – 0.07 churn) = $41,850 MRR

Churn isn’t optional to model. Service startups often see 5–10% monthly churn early on. If you’re at 85% retention today, assume it drops. Update this number quarterly.

Real talk: A NYC-based marketing consultancy saw retention fall from 85% to 62% in 18 months. Their forecast didn’t account for that. They missed payroll twice.

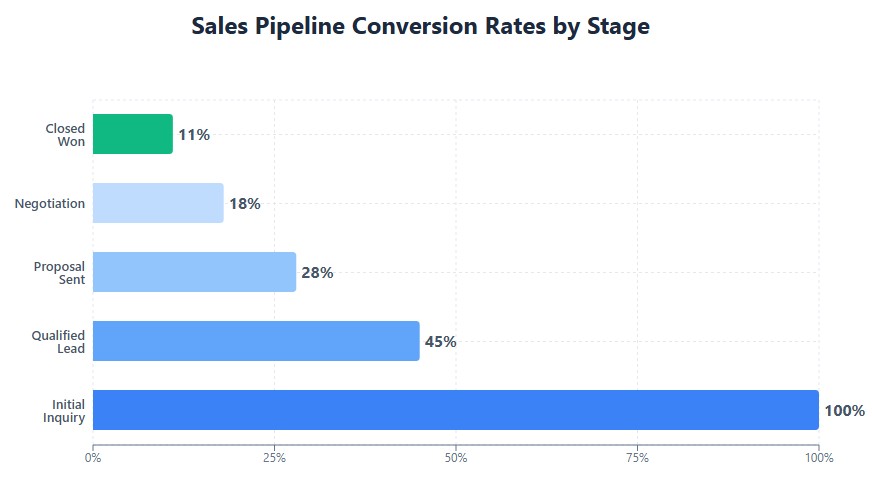

Step 4: Map Your Sales Pipeline—Not Your Hope

A lead isn’t revenue. A proposal isn’t revenue. Closed-won, signed, started—that’s revenue.

Apply two filters to your pipeline:

- Lead-to-close rate (e.g., 25% for cold outreach, 40%+ for referrals)

- Average sales cycle (e.g., 45 days for small retainers, 90+ for enterprise)

Only count deals that will realistically close and start delivering in the forecast month. Everything else goes in a “potential” tab—not your revenue column.

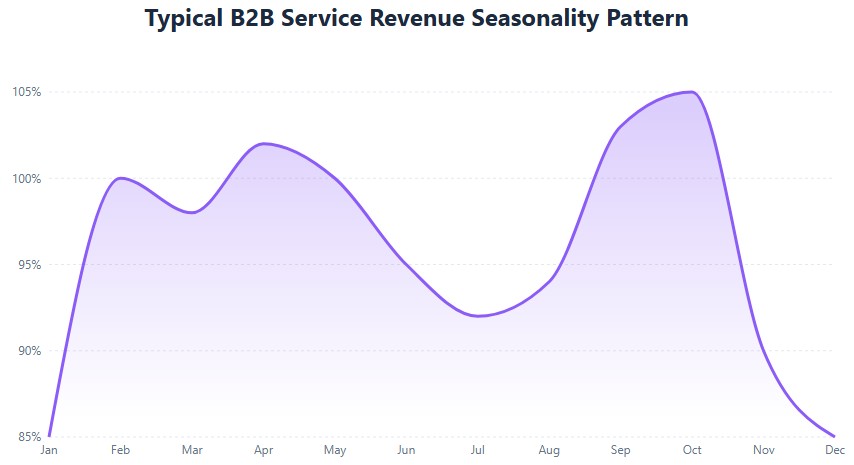

Step 5: Bake in Seasonality (Yes, Even in B2B)

Q4 slows down. January is quiet. Summer dips happen.

For B2B legal, consulting, or creative services, a 10–15% revenue dip in Q4 is normal. Use NFIB small business surveys or your own historical data to adjust.

If you don’t have history? Assume a 10% dip in November–December and a 15% rebound in February. Better to be conservative.

Source: NFIB Small Business Economic Trends

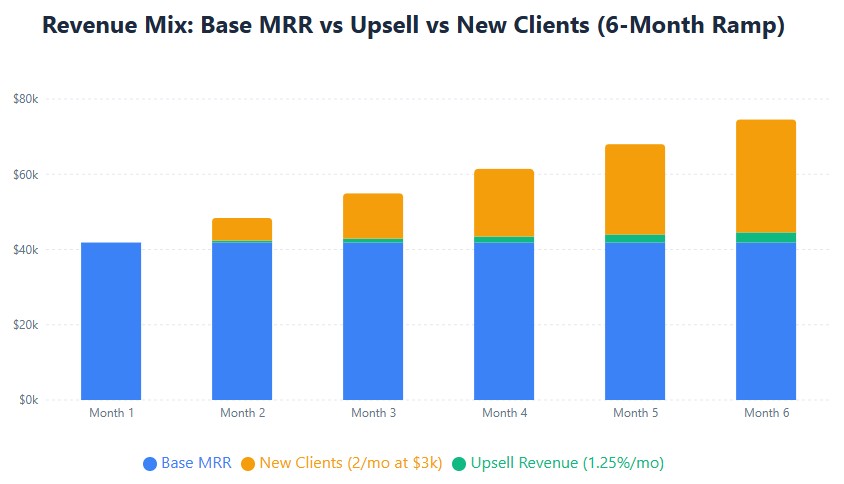

Step 6: Model Upsells—But Keep It Conservative

Happy clients buy more. But not as fast as you think.

McKinsey’s 2024 research on professional services suggests 15–20% of clients expand contracts annually. That’s ~1.25–1.5% per month. Apply that to your base MRR—not your best-case scenario.

And track it separately. Upsell revenue is fragile. If a client leaves, you lose both base and expansion.

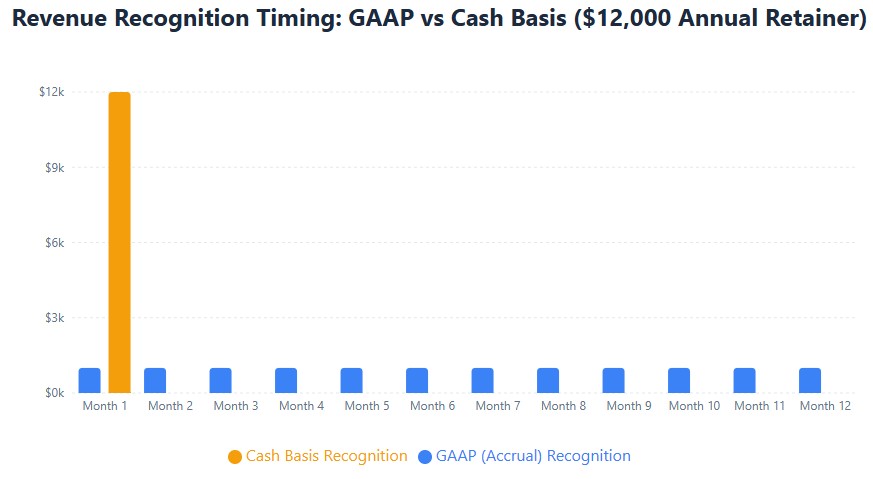

Step 7: Align Billing with Accounting Method (Cash vs. Accrual)

This is where many founders trip.

- Cash basis (common for small startups): Recognize revenue when money hits your account.

- Accrual/GAAP (required for investors, lenders): Recognize revenue as you deliver the service.

Example: A $12,000 annual retainer paid upfront.

- Cash basis: $12,000 revenue in Month 1.

- GAAP: $1,000/month for 12 months. The rest is deferred revenue (a liability).

You can use cash basis for taxes if your average annual gross receipts are under $26 million (IRS small business exception, 2026). But if you’re raising capital or applying for an SBA loan, you’ll need GAAP-aligned numbers.

Track both. Keep a simple reconciliation tab. It saves headaches later.

Source: IRS Publication 538 – Accounting Periods and Methods

GAAP vs. Tax: What You Actually Need to Know (No Jargon Dump)

You don’t need to be an accountant. But you do need to avoid two costly mistakes:

- Reporting GAAP revenue to the IRS (or vice versa)

- Ignoring deferred revenue when talking to investors

Here’s the short version:

| What You’re Tracking | GAAP (For Investors/Lenders) | Tax Basis (For IRS) | Why It Matters |

|---|---|---|---|

| When to recognize revenue | As services are delivered | When cash is received (if using cash method) | Timing differences affect cash flow planning |

| Prepaid retainers | Liability until earned | Taxable when received (cash basis) | Creates a temporary gap between book and tax income |

| Contract changes | Reallocate to remaining obligations | Treat as new income if cash received | Impacts MRR stability and tax timing |

Bottom line: Build your forecast in GAAP for credibility. Then add a simple toggle or tab to show cash-basis equivalents for tax planning. One model, two views.

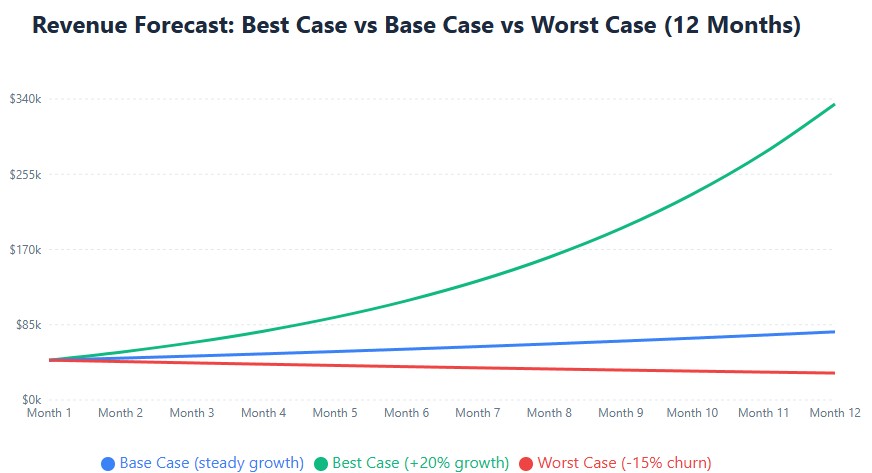

Build a Lender-Ready Forecast (Without Buying Expensive Software)

You don’t need Adaptive Insights on day one. Start simple.

Tool recommendation: Google Sheets. Free, collaborative, and flexible. Upgrade to QuickBooks Online or Xero once you’re past $50k/month in revenue.

Your forecast should include:

- Input tab: Clients, ACV, churn, sales cycle, seasonality factors

- Calculation tab: MRR, new client ramp, upsell, total revenue

- Scenario tab: Best case (+20% growth), base case (current trends), worst case (–15% churn or macro shock)

- Cash flow link: Subtract operating expenses, payroll, estimated taxes—but keep gross revenue visible

Validate against SBA benchmarks:

- DSCR >1.25x (lenders want to see you can cover debt payments)

- YoY revenue growth >15% (shows momentum)

Real example: An Austin-based IT services firm won a $360,000, 3-year city contract. They forecasted $10,000/month recognized ratably under GAAP. That boosted their MRR by 35% and helped them secure a $150k SBA Microloan. The key? They didn’t book the full amount upfront. They showed steady, defensible growth.

Avoid These 4 Forecast-Killing Mistakes

- Booking prepayments as Month 1 revenue (in GAAP)

It’s tempting. Don’t. If services are delivered over 12 months, recognize revenue over 12 months. Investors and auditors will catch this. - Ignoring sales tax variability

Texas taxes certain IT and consulting services at 6.25%. Florida doesn’t. If you forecast gross revenue without netting expected sales tax, your net revenue will be off. Factor it out early. - Overlooking client concentration

If 3 clients make up >50% of your revenue, stress-test what happens if one leaves. Lenders will. Add a “concentration risk” note to your forecast. - Misclassifying contractors

California’s AB 5 and similar laws in other states can reclassify 1099 contractors as W-2 employees. That changes your labor costs—and your scalability assumptions. Track subcontractor costs separately. Don’t net them against revenue.

Which Forecasting Model Fits Your Stage?

Not all methods work for all startups. Pick based on your data, not your ambition.

| Method | Best For | What You Need | VC Readiness |

|---|---|---|---|

| Historical Growth Rate | Year 2+ with 12+ months of data | Past revenue trends | Medium |

| Deal-Stage Pipeline | Early-stage, long sales cycles | CRM data, close rates, ACV | High |

| Recurring Revenue Model | Retainer/subscription services | MRR, churn, retention metrics | Very High |

If you’re pre-seed and selling projects, start with pipeline-based forecasting. If you have retainers, lean into MRR + churn. If you have history, use it—but adjust for market changes.

When to Hit Refresh on Your Forecast (Practical Triggers)

Static forecasts fail. Update yours when:

- Revenue crosses $100k/month: Talk to a CPA. If you’re a C-Corp or approaching $26M in average annual receipts, the IRS may require accrual accounting.

- Quarterly tax deadlines approach (April 15, June 15, Sept 15, Jan 15): Align your forecast with Form 1040-ES payments. Adjust if you’re ahead or behind.

- You hire your first W-2 employee: Payroll taxes (FUTA, SUTA, FICA) can reduce net margin by 7–10%. Update your model.

- You’re raising a priced round: Transition to GAAP-compliant forecasting. Auditors will expect ASC 606 alignment and validated pipeline assumptions.

Quick Answers to Real Founder Questions

How often should I update my forecast?

Quarterly at minimum. Monthly if you’re pre-seed or scaling past $50k/month.

Do I need GAAP for investor pitches?

Yes, if you’re talking to institutional capital. Angels might be flexible. VCs and banks expect ASC 606-aligned P&Ls.

Can I use cash basis for my forecast?

For internal planning or tax purposes, yes—if you’re under $26M in average annual gross receipts. For fundraising or SBA loans, build a GAAP version too.

One Last Thing: Keep It Living

Your forecast isn’t a document you file and forget. It’s a tool. Update it when reality shifts. Share it with your CPA before tax season. Use it to stress-test decisions.

And if you’re in a high-compliance state (California, New York, Illinois), loop in a local CPA early. Not for permission. For prevention.

Forecasting isn’t about being right every time. It’s about being prepared for what’s next. Build a model that helps you do that—and you’ll stand out from founders who are still guessing.